|

TrueCar, Inc. (TRUE): Análisis de 5 Fuerzas [Actualizado en Ene-2025] |

Completamente Editable: Adáptelo A Sus Necesidades En Excel O Sheets

Diseño Profesional: Plantillas Confiables Y Estándares De La Industria

Predeterminadas Para Un Uso Rápido Y Eficiente

Compatible con MAC / PC, completamente desbloqueado

No Se Necesita Experiencia; Fáciles De Seguir

TrueCar, Inc. (TRUE) Bundle

En el mercado automotriz digital en rápida evolución, TrueCar, Inc. se encuentra en la encrucijada de la innovación tecnológica y la interrupción de la industria. Al diseccionar el marco de las cinco fuerzas de Michael Porter, presentamos el complejo panorama competitivo que da forma al posicionamiento estratégico de Truecar en 2024. Desde la navegación de la dinámica del proveedor hasta la comprensión del poder del cliente, este análisis proporciona una visión afilada de los desafíos y las oportunidades que enfrenta esta plataforma automotriz digital, revelando cómo TrueCar maniobra a través de un ecosistema de la industria cada vez más competitivo y transformador.

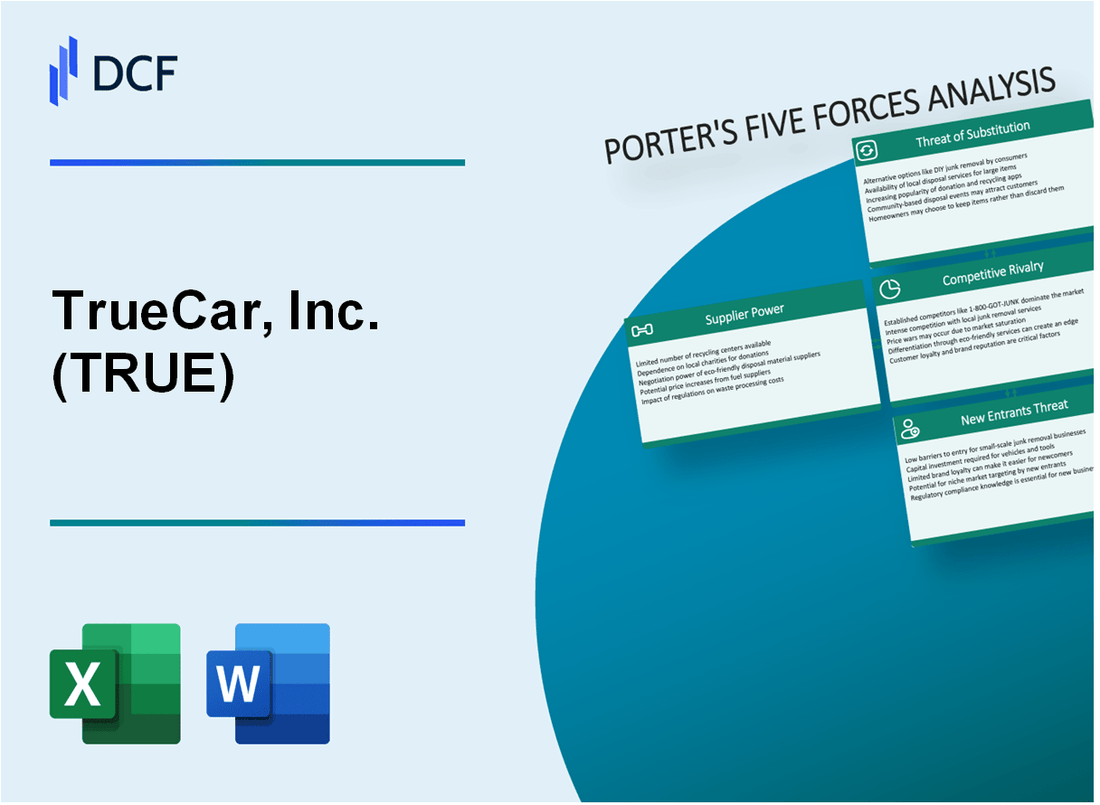

Truecar, Inc. (verdadero) - Las cinco fuerzas de Porter: poder de negociación de los proveedores

Número limitado de fabricantes de automóviles y redes de concesionarios

A partir de 2024, el mercado automotriz de EE. UU. Está dominado por un pequeño número de principales fabricantes:

| Fabricante | Cuota de mercado | Producción anual |

|---|---|---|

| General Motors | 16.8% | 2.3 millones de vehículos |

| Vado | 13.5% | 1.9 millones de vehículos |

| Stellantis | 12.7% | 1.7 millones de vehículos |

| Toyota | 14.2% | 2.0 millones de vehículos |

Proveedores de datos y proveedores de tecnología

TrueCar se basa en múltiples tecnología y socios de infraestructura de datos:

- Socios de intercambio de datos automotrices: 7 proveedores principales

- Proveedores de infraestructura en la nube: 3 proveedores principales

- Valor de contrato de proveedor de tecnología anual promedio: $ 2.4 millones

Dependencia de las fuentes de datos de la industria automotriz

Desglose de abastecimiento de datos de TrueCar:

| Fuente de datos | Porcentaje de datos | Costo anual |

|---|---|---|

| Redes de concesionario | 45% | $ 3.6 millones |

| Feeds Direct Feeds del fabricante | 35% | $ 2.9 millones |

| Agregadores de terceros | 20% | $ 1.7 millones |

Costos de cambio potenciales para la infraestructura tecnológica

Estimaciones de costos de cambio de infraestructura tecnológica:

- Costo de migración promedio: $ 1.2 millones

- Riesgo estimado de tiempo de inactividad: 3-4 semanas

- Pérdida de ingresos potencial durante la migración: $ 500,000- $ 750,000

Truecar, Inc. (verdadero) - Las cinco fuerzas de Porter: poder de negociación de los clientes

Bajos costos de cambio para compradores de automóviles utilizando plataformas en línea

La plataforma digital de TrueCar permite a los clientes comparar fácilmente los precios y cambiar entre mercados automotrices con una fricción mínima. A partir del cuarto trimestre de 2023, la plataforma de TrueCar facilitó 844,000 transacciones de compra de vehículos, lo que representa un aumento del 12.3% respecto al año anterior.

| Métrico | Valor |

|---|---|

| Transacciones de plataforma totales (2023) | 844,000 |

| Crecimiento de la transacción año tras año | 12.3% |

| Costo promedio de adquisición de clientes | $47.50 |

Capacidades de transparencia y comparación de alta transparencia

TrueCar proporciona herramientas integrales de comparación de precios en múltiples concesionarios. En 2023, la plataforma mostró datos de precios para:

- Más de 16,500 ubicaciones de concesionario

- Aproximadamente 3.5 millones de listados de vehículos

- Comparaciones de precios en tiempo real en 50 estados

Los consumidores tienen múltiples mercados automotrices digitales

El análisis competitivo del panorama revela una fragmentación significativa del mercado:

| Mercado automotriz en línea | Usuarios activos mensuales |

|---|---|

| Truecar | 6.7 millones |

| Carvana | 5.2 millones |

| Carguero | 7.1 millones |

| Cars.com | 4.9 millones |

Fuerte demanda del consumidor de experiencias simplificadas de compra de automóviles

Las preferencias del consumidor demuestran una tendencia clara hacia la compra de automóvil digital:

- El 68% de los compradores de automóviles prefieren la investigación en línea antes de las visitas al concesionario

- 42% Completa porciones significativas de compra de vehículos en línea

- Tiempo promedio dedicado a la plataforma TrueCar por usuario: 12.4 minutos

Truecar, Inc. (verdadero) - Las cinco fuerzas de Porter: rivalidad competitiva

Competencia intensa en el mercado automotriz digital

A partir de 2024, Truecar enfrenta una presión competitiva significativa de múltiples plataformas automotrices digitales:

| Competidor | Cuota de mercado | Ingresos anuales |

|---|---|---|

| Carguero | 23.4% | $ 687.2 millones |

| Edmunds | 15.7% | $ 412.5 millones |

| Cars.com | 19.6% | $ 545.3 millones |

| Truecar | 12.9% | $ 326.8 millones |

Plataformas de mercado automotriz digital

Características del panorama competitivo:

- Número total de plataformas automotrices digitales activas: 17

- Tamaño estimado del mercado: $ 2.3 mil millones

- Base de usuarios promedio de la plataforma: 3.6 millones de visitantes mensuales

- Costo promedio de adquisición de clientes: $ 42 por usuario

Requisitos de innovación tecnológica

Métricas de inversión tecnológica:

| Categoría de innovación | Inversión anual | Ciclo de desarrollo |

|---|---|---|

| AI/Aprendizaje automático | $ 15.7 millones | 6-8 meses |

| Diseño de experiencia de usuario | $ 8.3 millones | 4-6 meses |

| Desarrollo de plataforma móvil | $ 11.2 millones | 5-7 meses |

Presiones de proposición de valor únicas

Métricas de diferenciación competitiva:

- Tasa promedio de retención de usuarios: 42.6%

- Rango de puntaje de satisfacción del cliente: 3.7-4.2/5

- Costo único de desarrollo de características: $ 2.1- $ 3.5 millones por función

Truecar, Inc. (verdadero) - Las cinco fuerzas de Porter: amenaza de sustitutos

Métodos tradicionales de compra de automóviles

A partir de 2024, los concesionarios de automóviles tradicionales representan el 89.3% de los canales de venta de vehículos. La cuenta de ventas privadas para aproximadamente el 10.7% de las transacciones de vehículos usados.

| Canal de ventas | Cuota de mercado (%) | Volumen de transacción promedio |

|---|---|---|

| Ventas de concesionario | 89.3 | 15,2 millones de vehículos/año |

| Ventas privadas | 10.7 | 1.8 millones de vehículos/año |

Plataformas emergentes de venta de automóviles de pares

Las plataformas de venta de automóviles entre pares generaron $ 3.4 mil millones en ingresos en 2023, con una tasa de crecimiento esperada del 12.7% anual.

- Carvana: $ 12.8 mil millones Ingresos totales en 2023

- Vroom: ingresos totales de $ 1.2 mil millones en 2023

- Carmax: $ 27.5 mil millones ingresos totales en 2023

Servicios de arrendamiento y suscripción de automóviles

El mercado de suscripción de automóviles alcanzó los $ 6.2 mil millones en 2023, con un crecimiento proyectado a $ 15.7 mil millones para 2027.

| Proveedor de servicios | Costo de suscripción mensual | Opciones de vehículos |

|---|---|---|

| Justo | $150 - $400 | Más de 150 modelos de vehículos |

| Flexible | $200 - $500 | Más de 100 modelos de vehículos |

Mercados de vehículos eléctricos

Los ingresos del mercado de vehículos eléctricos alcanzaron los $ 42.3 mil millones en 2023, con un crecimiento de 18.2% año tras año.

- Ventas directas de Tesla: $ 23.4 mil millones en 2023

- Rivian Marketplace: $ 4.7 mil millones en 2023

- Ventas de Lucid Motors: $ 1.2 mil millones en 2023

Truecar, Inc. (verdadero) - Las cinco fuerzas de Porter: amenaza de nuevos participantes

Costos iniciales de desarrollo de tecnología

Los costos de desarrollo tecnológico de Truecar en 2023 fueron de $ 37.8 millones, lo que representa el 21.4% de los gastos operativos totales. El desarrollo de una plataforma de mercado automotriz comparable requiere una inversión inicial significativa.

| Categoría de inversión tecnológica | Costo anual |

|---|---|

| Desarrollo de software | $ 22.5 millones |

| Infraestructura de datos | $ 9.3 millones |

| Integración de aprendizaje automático/AI | $ 6 millones |

Relaciones de red de distribuidores

Truecar mantiene relaciones con 10,287 concesionarios en los Estados Unidos a partir del cuarto trimestre de 2023.

- Costo de adquisición del concesionario: $ 3,750 por socio de red

- Tasa de retención promedio de los distribuidores: 78.6%

- Cobertura de red de distribuidores: 85% de los mercados automotrices estadounidenses

Requisitos de integración de datos automotrices

TrueCar procesa aproximadamente 6.2 millones de precios de vehículos y puntos de datos de transacción mensualmente.

| Componente de integración de datos | Inversión anual |

|---|---|

| Infraestructura de recopilación de datos | $ 5.6 millones |

| Sistemas de validación de datos | $ 3.2 millones |

| Tecnología de integración en tiempo real | $ 4.1 millones |

Inversiones de marketing para participación de mercado

Truecar gastó $ 48.3 millones en marketing en 2023, dirigido a la adquisición de clientes y la conciencia de la marca.

- Costo de adquisición de clientes: $ 127 por usuario

- Canales de comercialización: publicidad digital, asociaciones, marketing directo

- Gastos de marketing como porcentaje de ingresos: 16.7%

TrueCar, Inc. (TRUE) - Porter's Five Forces: Competitive rivalry

The competitive rivalry within the digital automotive marketplace is defintely intense, driven by the presence of well-capitalized public competitors. You see this scale difference clearly when you compare TrueCar, Inc.'s top-line performance against rivals like CarGurus. For instance, TrueCar, Inc.'s total revenue for the third quarter of 2025 was reported at only $43.2 million.

To put that in perspective against a key rival, CarGurus posted revenue of $238.70 million for its third quarter, and maintained a market capitalization of approximately $3.49 Billion USD as of November 2025. This disparity in scale means TrueCar, Inc. must fight aggressively for every dealer budget and consumer click.

This fight manifests in high operating expenditures. Consider the first quarter of 2025: TrueCar, Inc.'s sales and marketing costs reached $24.5 million. That spend represented 54.6% of the $44.8 million Q1 2025 revenue, showing how much capital is required just to maintain, let alone grow, market share in this environment.

Competition centers on core operational strengths. You are competing on the quality and quantity of your audience, the breadth of your dealer network, and the stickiness of your product innovations, such as the TrueCar+ platform. The market itself feels mature, which translates to a zero-sum game for the finite advertising dollars allocated by dealer groups.

Here is a quick look at the scale difference in key metrics as of late 2025:

| Metric | TrueCar, Inc. (Q3 2025) | CarGurus (Q3 2025) |

| Revenue | $43.2 million | $238.70 million |

| Market Capitalization | (Implied significantly lower than competitor) | $3.49 Billion USD (as of Nov 2025) |

| Average Monthly Unique Visitors | 5.6 million | (Data not directly comparable/available) |

| Franchise Dealer Count | 8,225 (as of Sept 30, 2025) | (Data not directly comparable/available) |

The pressure on dealer relationships is evident in the network dynamics. If onboarding takes 14+ days, churn risk rises, especially when alternatives are readily available. The competitive battleground includes:

- Traffic volume and quality.

- The size and quality of the dealer network.

- Consumer experience features like TrueCar+.

- Dealer monetization per unit.

The dealer network itself is showing signs of contraction under this pressure. TrueCar, Inc.'s franchise dealer count fell to 8,225 as of September 30, 2025, down from 8,292 in the prior quarter. Similarly, the independent dealer count dropped to 2,794 from 2,885 sequentially. This shrinking footprint highlights the difficulty in retaining dealer partners when budgets are tight across the industry.

TrueCar, Inc. (TRUE) - Porter's Five Forces: Threat of substitutes

You're looking at the competitive landscape for TrueCar, Inc. (TRUE) as of late 2025, and the threat from substitutes is definitely a major factor. The most visible substitutes are those direct-to-consumer online retailers that have matured significantly since their early days.

Take Carvana, for example. As a major substitute, Carvana reported third quarter 2025 revenue of $5.647 billion and sold 155,941 retail units in that same period. Compare that to TrueCar, Inc.'s third quarter 2025 total revenue of just $43.2 million and 87.5 thousand total units sold. It's clear these direct players command a much larger transaction volume, even though Carvana still held only about 1% of the highly fragmented U.S. automotive retail market as of early 2025. Analysts estimate Carvana's full-year 2025 Adjusted EBITDA could range between $1.8 billion and $2.2 billion.

Consumers still have ways to bypass marketplaces entirely, which pressures TrueCar, Inc.'s model. You see this pressure reflected in the shrinking network TrueCar, Inc. relies on. As of September 30, 2025, the franchise dealer count stood at 8,225, down from 8,303 a year earlier. Similarly, the independent dealer count dropped to 2,794 from 3,106 in the third quarter of 2024. If a consumer can go straight to a dealer's own website, they cut out the middleman, including TrueCar, Inc.

New technology, especially AI, is rapidly emerging as a substitute for traditional search and discovery methods. A Cars.com survey from November 2025 found that 44% of consumers opted to use AI-powered car search tools when shopping. What's more telling is that 97% of those AI users say the technology will impact their purchase decisions. Even among all car buyers in 2025, 25% report using or planning to use AI tools like ChatGPT for research or negotiation. This shift means that AI-driven search results, which can aggregate data from many sources, substitute for the curated experience a marketplace like TrueCar, Inc. offers. Dealers are responding, with 81% anticipating an increase in their AI budget for 2025.

Still, the old ways haven't vanished. Traditional auto classifieds and local newspaper listings continue to serve a segment of the market, particularly for private party sales or older inventory where digital marketplace fees might seem excessive to the seller. While we don't have precise 2025 market penetration figures for these legacy channels, their existence means consumers always have a low-tech alternative to structured online platforms.

| Metric | TrueCar, Inc. (Q3 2025) | Direct Substitute (Carvana Q3 2025) |

|---|---|---|

| Revenue | $43.2 million | $5.647 billion |

| Retail Units Sold | 87.5 thousand | 155,941 |

| Net Income | $5.0 million | $263 million |

| Adjusted EBITDA | $(0.4) million | $637 million |

| Dealer Network (Franchise/Total) | 8,225 (Franchise as of 9/30/2025) | N/A (Direct-to-Consumer Model) |

The threat here is multifaceted: established online giants offer scale, direct dealer engagement cuts out the platform fee, and new AI tools are becoming the default research starting point for nearly everyone.

TrueCar, Inc. (TRUE) - Porter's Five Forces: Threat of new entrants

You're assessing the competitive landscape for TrueCar, Inc. as it moves into a private structure. The threat of new entrants, or how easily a competitor could start up and steal market share, is definitely a key factor here. Honestly, the barriers to entry aren't zero, but they aren't insurmountable for a well-funded player.

The primary hurdle is the dealer network. Building a national footprint that rivals TrueCar's established network of over 8,500 franchised and independent dealers across all 50 states requires substantial time and capital investment. To give you a snapshot of that network as of early 2025, TrueCar reported 2,936 franchise dealers and 8,336 independent dealers in Q1 2025, though the independent count later settled to 2,794 by September 30, 2025, reflecting a strategic focus on franchise activations. Starting from scratch to secure that level of dealer commitment and integration is a massive undertaking.

Next up is the cost of building brand trust and acquiring customers. Consumers need to trust the platform before they enter a negotiation-free transaction. TrueCar historically poured significant resources into this; for instance, sales and marketing expenses totaled $95.6 million in 2024. While the company has shown operational improvements, like achieving positive Adjusted EBITDA of $0.4 million in Q4 2024, Q1 2025 saw a negative Adjusted EBITDA of $(3.8) million, showing that customer acquisition remains an expensive proposition. Any new entrant faces this same steep marketing cliff.

However, the recent transaction details suggest the market might not value the incumbent's assets as highly as a true market leader's might be valued. The agreed-upon all-cash, go-private transaction valued TrueCar's equity at approximately $227 million. This valuation, while delivering a premium to shareholders, indicates that the cost to acquire or build a comparable, established platform might be lower than one might initially assume for a dominant player, potentially lowering the perceived barrier for a well-capitalized disruptor.

A significant, though not impenetrable, barrier is TrueCar's established channel access through affinity partners. The company powers auto-buying programs for over 250 leading brands, including major credit unions and membership organizations. These relationships create a powerful 'transfer of trust' that new entrants would need to replicate, which involves securing agreements with large, trusted entities that have millions of members ready to shop.

Here's a quick look at the key figures influencing this threat assessment:

| Metric | Value/Amount | Context/Date |

|---|---|---|

| National Dealer Network Size | Over 8,500+ | Established footprint |

| Q1 2025 Franchise Dealers | 2,936 | Q1 2025 Snapshot |

| 2024 Sales & Marketing Expense | $95.6 million | Historical investment in brand/acquisition |

| Acquisition Equity Valuation | Approx. $227 million | October 2025 transaction value |

| Affinity Partner Count | Over 250 | Existing relationships |

The combination of a large, integrated dealer network and deep-seated affinity partnerships means a new entrant must secure both physical infrastructure and consumer trust simultaneously. Still, the $227 million price tag suggests that the market sees a path for a new owner to streamline operations and potentially lower the cost structure, which could embolden a competitor looking to enter with significant private equity backing.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.