|

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ): BCG Matrix [Apr-2026 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ) Bundle

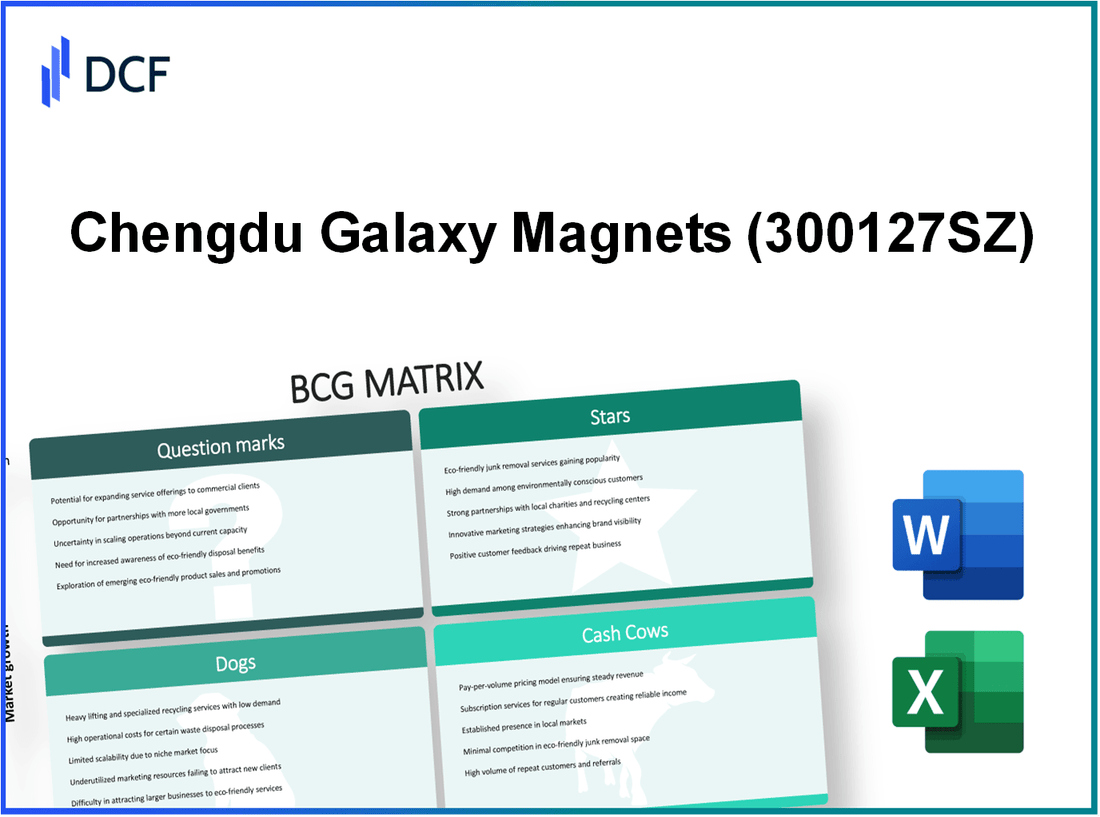

Chengdu Galaxy Magnets sits at a pivotal inflection-high-growth Stars in automotive, robotics and advanced NdFeB technologies are driving rapid revenue and margin expansion and receiving heavy CAPEX and R&D backing, while mature Cash Cows like HDD and appliance magnets continue to fund that push; however, capital-hungry Question Marks (EV traction motors, SmCo, renewables, medical) demand decisive investment or partnerships to scale, and a clutch of Dogs tied to legacy consumer and office products are being harvested or wound down-how management allocates cash between defending market leadership and selectively funding new high‑potential plays will determine whether the company converts its innovation pipeline into sustained market dominance.

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ) - BCG Matrix Analysis: Stars

Stars

EXPANDING AUTOMOTIVE BONDED MAGNET SOLUTIONS - The automotive bonded magnet solutions business is the principal Star, accounting for ~45% of Chengdu Galaxy's total annual revenue as of late 2025. The unit operates in a market growing at ~18% CAGR driven by electrification of vehicle subsystems (electronic power steering, braking systems, EPS modules). Chengdu Galaxy holds a 25% global market share in this niche, with gross margins of ~32% and a segment ROI >22%. The company allocated 85 million RMB in CAPEX this fiscal year to install automated production lines, increasing capacity and reducing per-unit labor costs. Order backlog from international Tier 1 suppliers remains strong, supporting projected revenue CAGR for the segment of 16-20% over the next 3 years.

HIGH PERFORMANCE HOT PRESSED MAGNET TECHNOLOGY - Hot pressed NdFeB magnets are a high-growth Star contributing ~12% to consolidated revenue and expanding at ~24% annually. These magnets target high-speed motors in robotics and aerospace; Chengdu Galaxy commands ~15% of the global high-end specialty market. Current production capacity is ~350 tonnes/year; gross margins are ~36% due to technical barriers and limited competition. The company reinvests ~15% of segment earnings into process optimization (sintering control, density improvements) to sustain magnet density and magnetic performance leadership.

INTELLIGENT ROBOT ACTUATOR MAGNET COMPONENTS - The robotics actuator segment recorded ~20% YoY order volume growth through December 2025, representing ~8% of corporate revenue. The underlying market grows at ~22% annually. Chengdu Galaxy has secured a ~12% share among leading humanoid robot manufacturers by delivering customized bonded magnet solutions for joints and sensors. Segment margins run at ~30%; capital investments this year include ~30 million RMB in specialized testing and precision metrology equipment to ensure near-zero defect rates for high-profile clients.

NEW ENERGY PUMP MAGNET SYSTEMS - High-efficiency magnets for EV thermal management pumps contribute ~10% of revenue and operate in a market expanding at ~25% annually as EV architectures grow more complex. The company captured ~20% of the domestic Chinese market for these pump components. Operating margins are ~28% with ROI for new production molds of ~19%. Management has doubled dedicated assembly headcount to process the projected 2026 order backlog, improving throughput and lead-time performance.

ADVANCED ELECTRONIC POWER STEERING MAGNETS - The EPS magnet division contributes ~15% to revenue, within a global market growing at ~12% annually as autonomous features proliferate in mid-range vehicles. Chengdu Galaxy holds ~30% share in the global bonded NdFeB EPS segment; gross margins are ~31% despite raw material price volatility. The firm invested 45 million RMB in magnetic field orientation technology this year to improve torque consistency and reduce warranty claims related to steering feel variability.

| Star Segment | Revenue Contribution (%) | Market Growth Rate (%) | Company Market Share (%) | Gross Margin (%) | Recent CAPEX / Investment (RMB) | Segment ROI (%) | Capacity / Notes |

|---|---|---|---|---|---|---|---|

| Automotive Bonded Magnet Solutions | 45 | 18 | 25 | 32 | 85,000,000 | >22 | Automated lines; high Tier 1 demand |

| Hot Pressed NdFeB Magnets | 12 | 24 | 15 | 36 | Reinvestment = 15% of segment earnings | - | 350 t/yr capacity; high-end motors |

| Robotics Actuator Components | 8 | 22 | 12 | 30 | 30,000,000 | - | Customized bonded solutions; precision testing |

| New Energy Pump Magnet Systems | 10 | 25 | 20 (domestic) | 28 | Molds CAPEX (undisclosed) + hiring | 19 | Thermal management pump components |

| EPS (Electronic Power Steering) Magnets | 15 | 12 | 30 | 31 | 45,000,000 | - | Bonded NdFeB; magnetic orientation tech |

Key performance metrics and strategic actions for Stars

- Capacity expansion and automation: 85M RMB CAPEX for automotive automated lines; production throughput expected to increase 25-35% post-commissioning.

- R&D and process reinvestment: ~15% of hot-pressed segment earnings channelled to process optimization; focus on magnetic density, sintering uniformity and yield improvement.

- Quality assurance and precision testing: 30M RMB invested in metrology and zero-defect testing for robotics actuators to meet OEM tolerances sub-0.1 mm.

- Workforce scaling: Assembly headcount doubled for new energy pump systems to process 2026 backlog; leads to projected lead-time reduction of ~40%.

- Advanced manufacturing tech: 45M RMB for magnetic field orientation tech in EPS segment to improve torque variance by estimated 10-15% and reduce warranty costs.

Financial and operational projections (next 12-36 months)

- Expected consolidated revenue share from Stars: maintain >70% of company revenue if mid-cycle demand holds (automotive + EPS + hot-pressed + pumps + robotics).

- Projected incremental revenue from CAPEX projects: automotive automation and EPS orientation tech expected to add ~10-14% incremental segment revenue by FY2026.

- Margin outlook: blended gross margin for Star segments expected to remain between 30-34% given current product mix and reinvestment levels.

- Return profile: targeted segment ROIs remain in the high-teens to low-twenties for core automotive and pump systems; hot-pressed magnets expected to sustain higher margins due to scarcity and technical barriers.

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ) - BCG Matrix Analysis: Cash Cows

Cash Cows

The following Cash Cow segments generate stable, high-margin cash flow for Chengdu Galaxy Magnets Co.,Ltd., funding R&D and investment into higher-growth Star segments while operating in low or negative market growth environments.

DOMINANT HARD DISK DRIVE MARKET POSITION

The Hard Disk Drive (HDD) magnet segment contributes 35% of consolidated revenue as of December 2025. Market growth is negative at -4% year-on-year due to SSD substitution, yet the company sustains a 50% global market share in bonded magnets for HDD spindle motors.

Key financial and operational metrics for the HDD segment include a gross margin of 26%, segment ROI of 28%, and annual maintenance CAPEX of 10 million RMB. High production-line efficiency yields cash conversion cycles under 45 days, and operating profit from the segment funds approximately 60-70% of strategic investments into new technologies.

STABLE HOUSEHOLD APPLIANCE MOTOR REVENUE

Magnets for household appliance motors account for 15% of total revenue. The segment experiences modest market growth of 3% annually, aligned with global consumer spending. Chengdu Galaxy holds a 20% share in the high-end appliance motor magnet market across Asia and Europe.

Financial metrics: gross margin 24%, segment ROI 18%, minimal R&D spend (<1% of segment sales). Annual CAPEX allocated to this unit averages 8 million RMB for minor tooling and efficiency upgrades. Cash flows are predictable with EBITDA margin near 20% and operating cash inflow stability of ±3% year-on-year.

OPTICAL DISK DRIVE SPINDLE MAGNETS

The Optical Disk Drive (ODD) spindle magnet segment contributes 5% of revenue. Global market contraction is approximately -8% annually but Chengdu Galaxy retains a 40% global market share in this niche due to legacy customer relationships and specialized manufacturing.

Gross margins remain at 22% primarily because production assets are fully depreciated. CAPEX requirements are near-zero (<1 million RMB annually). The minimal reinvestment need allows almost all operating profit (~90% of segment EBITDA) to be reallocated to Star businesses. Cash conversion rate for this unit exceeds 95% of operating profit to free cash flow.

LEGACY POWER TOOL COMPONENT MAGNETS

Power tool component magnets represent 7% of annual revenue. The global market grows slowly at 2% annually; Chengdu Galaxy holds a 15% share in the professional-grade power tool magnet segment backed by long-term supply agreements.

Gross margin is 25% with annual reinvestment rates below 2% of segment sales (approx. 3-4 million RMB). Contractual price stability and extended payment terms produce steady operating cash flow which supports dividend policy and scheduled debt servicing. Segment ROI measures near 20% on an operating basis.

TRADITIONAL SENSOR MAGNET COMPONENTS

Basic sensor magnets for industrial applications contribute 6% of revenue. Market growth is stable at 4% annually; company global market share stands at 10% within industrial sensor components.

Gross margin averages 23% with an ROI of 16%. Production uses older but highly reliable machinery with annual maintenance CAPEX of approximately 5 million RMB. Low marketing and technical support costs yield consistent returns and predictable cash generation used for working capital and contingency reserves.

| Segment | % of Total Revenue (2025) | Market Growth Rate | Company Market Share (Global) | Gross Margin | Segment ROI | Annual CAPEX (RMB) |

|---|---|---|---|---|---|---|

| HDD Magnets | 35% | -4% YoY | 50% | 26% | 28% | 10,000,000 |

| Household Appliance Motors | 15% | +3% YoY | 20% | 24% | 18% | 8,000,000 |

| ODD Spindle Magnets | 5% | -8% YoY | 40% | 22% | - (operating ROI basis) | 1,000,000 |

| Power Tool Components | 7% | +2% YoY | 15% | 25% | 20% | 3,500,000 |

| Sensor Magnet Components | 6% | +4% YoY | 10% | 23% | 16% | 5,000,000 |

Consolidated Cash Cow Financial Snapshot (2025): total revenue contribution 68% from listed Cash Cow segments; weighted average gross margin ~24.3%; weighted average ROI ~20.4%; total annual CAPEX across Cash Cow units ≈ 27.5 million RMB; cash conversion cycle weighted average ~50 days.

- Primary cash generation: HDD magnets (35% revenue, largest absolute EBITDA contributor).

- Low capital intensity across Cash Cows enables redirection of free cash flow to Star segments and shareholder returns.

- Exposure risk: secular decline in HDD and ODD markets requires monitoring and potential portfolio rebalancing over medium term.

- Stability drivers: long-term contracts, fully depreciated assets, and high utilization rates preserve margins and cash yields.

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ) - BCG Matrix Analysis: Question Marks

Question Marks - Emerging Electric Vehicle Traction Motor Segment: The traction motor magnet market currently accounts for 4% of Chengdu Galaxy's total revenue. Segment CAGR >40%. Company market share <2%. Required R&D investment: RMB 60,000,000 to develop high-temperature resistant magnet materials and coatings capable of sustained operation above 200°C. Current gross margin: 18% (suppressed by low volumes and initial capital-intensive tooling). Target: achieve economies of scale and lift margin to 30% within 36 months if long-term supply contracts are secured. Critical milestone: secure binding multi-year contracts with at least two top-10 global EV OEMs within 24 months to justify incremental capacity build-out (estimated incremental capex: RMB 120,000,000 for sintering and thermal-treatment lines). Current production volume: pilot output ~120,000 units-equivalent/year.

Question Marks - Specialized Samarium Cobalt (SmCo) Magnet Applications: SmCo represents 3% of 2025 revenue. Market growth: 15% CAGR driven by defense, aerospace, and deep-sea applications. Chengdu Galaxy global SmCo market share: ~1%. Operating margin: 20% today but exposed to volatile rare-earth and cobalt pricing. Raw material cost risk: samarium and cobalt price variance can swing input costs ±18-25% year-over-year. Committed capital: RMB 25,000,000 for a vacuum induction melting furnace to improve yield and reduce scrap by projected 6-8 percentage points. Target: increase share to 4-6% in 3-5 years through quality upgrades and qualification contracts. Current annual SmCo throughput: ~350 tonnes-equivalent.

Question Marks - High Speed Railway Sensor Magnets: Contribution <2% of revenue. Market growth: 12% CAGR supported by global rail infrastructure projects. Company status: qualification phase with most major rail operators; market share negligible (<0.5%). Current margin: break-even to 10% depending on certification amortization. Required investments: international certifications and type-approval testing (estimated compliance spend: RMB 18,000,000) and dedicated clean-room assembly lines (capex estimate: RMB 40,000,000). Key dependency: successful field trials scheduled H1 2026; positive results could enable contracts with rail integrators and lift margins to industry norms of 18-22% over 3 years.

Question Marks - Renewable Energy Generator Magnet Components: Revenue share: 2%. Market growth: 18% CAGR due to decentralized wind and small hydro demand. Company market share: <3%. Current gross margin: 15% due to market-entry price strategies and small-batch inefficiencies. Capital allocation: RMB 20,000,000 for development of large-format bonded magnet production and tooling to serve small turbine and micro-hydro generators. Strategic objective: reach 8-10% market share in 4 years and margin improvement to 25% after scale and process optimization. Competitor dynamic: price pressure from large sintered magnet producers; lead time to scale: 18-30 months.

Question Marks - Medical Imaging Equipment Magnet Components: Revenue share: 1%. Market growth: 10% CAGR for medical imaging components requiring high precision and traceability. Company market share: <1%. Status: prototype stage with two major medical device OEMs; margins currently low at 12% due to extensive testing and compliance costs (expected additional spend: RMB 8,500,000 for ISO 13485 and device-specific validations). Time to commercialization: multi-stage regulatory and clinical validations with expected approval/qualification window of 24-48 months. Strategic goal: leverage high precision magnetic alignment capability to convert this into a Star - target margin post-qualification: 28-32%.

| Segment | 2025 Revenue % | Market CAGR | Company Market Share | Current Margin | Committed/Required Capex (RMB) | Key Timeline | Primary Risk |

|---|---|---|---|---|---|---|---|

| EV Traction Motors | 4% | >40% | <2% | 18% | RMB 60,000,000 (R&D) + RMB 120,000,000 potential capacity) | 24 months to secure OEM contracts | Failure to win long-term OEM contracts |

| SmCo Applications | 3% | 15% | ~1% | 20% | RMB 25,000,000 (VIM furnace) | 3-5 years to meaningful share gain | Raw material price volatility |

| High Speed Railway Sensors | <2% | 12% | <0.5% | ~10% (break-even) | RMB 58,000,000 (certification + clean-room) | Field trials H1 2026 | Qualification and certification delays |

| Renewable Energy Generators | 2% | 18% | <3% | 15% | RMB 20,000,000 (large-format bonded magnet dev) | 18-30 months to scale | Competition from larger sintered producers |

| Medical Imaging | 1% | 10% | <1% | 12% | RMB 8,500,000 (compliance/testing) | 24-48 months to regulatory qualification | Long approval lead times and high compliance cost |

Strategic imperatives for these Question Marks:

- Prioritize segments with highest upside-to-investment ratio (EV traction and SmCo) while staging capex to milestones.

- Negotiate conditional offtake or development agreements with anchor customers to derisk R&D spend and shorten payback periods.

- Hedge raw material exposure for SmCo and EV rare-earth inputs via long-term supply contracts or financial hedges to limit input-cost volatility of ±20%.

- Allocate technical and regulatory resources to accelerate railway and medical qualifications; target grant/subsidy programs to offset certification capex.

- implement production scale strategies (capacity sharing, contract manufacturing) to improve gross margins from current 12-18% range toward 25-30% where feasible.

Chengdu Galaxy Magnets Co.,Ltd. (300127.SZ) - BCG Matrix Analysis: Dogs

LEGACY CONSUMER ELECTRONICS VIBRATION MOTORS: Magnets for legacy vibration motors in basic mobile phones now contribute only 2 percent to total revenue. This segment is facing a market decline of 12 percent annually as haptic technology shifts toward more advanced linear actuators. Company market share has eroded to 5 percent as resources pivot to automotive applications. Gross margin is compressed to 14 percent, making this one of the least profitable units. Reported ROI is negative 2 percent and there is no planned CAPEX for the upcoming fiscal year.

STANDARD OPTICAL PICK UP UNIT MAGNETS: The market for standard optical pick up unit magnets has shrunk to represent 1 percent of company sales. Market growth is currently -20 percent as streaming services replace physical media. The company holds a 10 percent share of this shrinking market but struggles with profitability; gross margins are 11 percent. Production lines are being repurposed for automotive sensor magnets where feasible. No new marketing or sales budget is allocated to this product line.

LOW END POWER TOOL MAGNETS: Basic magnets for entry-level DIY power tools contribute 3 percent to revenue and face intense price competition. Market growth is stagnant at 1 percent and company share stands at 4 percent. Gross margins have declined to 12 percent due to undercutting by low-cost competitors from emerging markets. Segment ROI is 5 percent, below the company weighted average cost of capital (WACC). Management is evaluating divestiture to concentrate on professional and industrial-grade tool components.

DISCONTINUED OFFICE AUTOMATION COMPONENTS: Magnets for older-generation photocopiers and printers now account for less than 1 percent of total revenue. This segment experiences market contraction of 15 percent as offices adopt paperless workflows. The company retains a 3 percent share, mainly for replacement parts. Gross margins are weak at 10 percent and the segment consumes disproportionate warehouse space. Capital allocation is zero and the unit is scheduled for full retirement by end-2026.

BASIC COMPUTER PERIPHERAL MAGNETS: Magnets for traditional computer mice and keyboards are classified as a Dog with a 1 percent contribution to 2025 revenue. Market growth is flat (0 percent) and commoditization is extreme. Company share is 2 percent with operating margins at 9 percent, barely covering logistics and administrative costs. The unit is being managed for harvest with no further investment in R&D or capacity expansion.

| Segment | Revenue % (2025) | Market Growth (%) | Company Market Share (%) | Gross Margin (%) | ROI (%) | CAPEX Plan | Strategic Action |

|---|---|---|---|---|---|---|---|

| Legacy Consumer Electronics Vibration Motors | 2 | -12 | 5 | 14 | -2 | 0 | Halt investment; reallocate resources to automotive |

| Standard Optical Pick Up Unit Magnets | 1 | -20 | 10 | 11 | Not reported (low) | 0 | Phase out; repurpose lines to automotive sensors |

| Low End Power Tool Magnets | 3 | 1 | 4 | 12 | 5 | Minimal / conditional | Consider divestiture; focus on premium tools |

| Discontinued Office Automation Components | <1 | -15 | 3 | 10 | Negative/Not meaningful | 0 | Retire by end-2026; reduce warehouse footprint |

| Basic Computer Peripheral Magnets | 1 | 0 | 2 | 9 | Low (near breakeven) | 0 | Harvest strategy; no R&D or capacity expansion |

Key near-term operational implications:

- Inventory and warehouse optimization required to eliminate low-turn Dogs (target reduction of warehouse space by 8-12% tied to office automation and legacy motors).

- Reallocation of human and capital resources toward automotive and industrial segments where margin expansion potential exceeds 200-300 basis points compared with Dogs.

- Planned CAPEX for Dogs: zero for three segments, conditional/minimal for low-end tools; forecasted FY2026 cost savings from decommissioning: estimated RMB 4-6 million.

- Divestiture targets: low-end power tool magnets and remaining legacy motor contracts-expected one-time disposal or sale proceeds estimated at RMB 2-4 million, contingent on buyer interest.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.