|

China Satellite Communications Co., Ltd. (601698.SS): BCG Matrix [Apr-2026 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

China Satellite Communications Co., Ltd. (601698.SS) Bundle

China Satellite Communications sits at a pivotal inflection point: cash-rich legacy C-/Ku-band leasing and TV broadcasting underwrite aggressive investment in HTS broadband, maritime/aviation connectivity, and government secure links that are poised to drive high-growth returns, while capital-hungry LEO, IoT ventures remain uncertain "bet-the-company" projects and aging MSS/transponder footprints demand pruning; how management balances sustaining cash cows, funding stars, nurturing question marks, and shedding dogs will determine whether China Satcom converts current dominance into future-scale leadership.

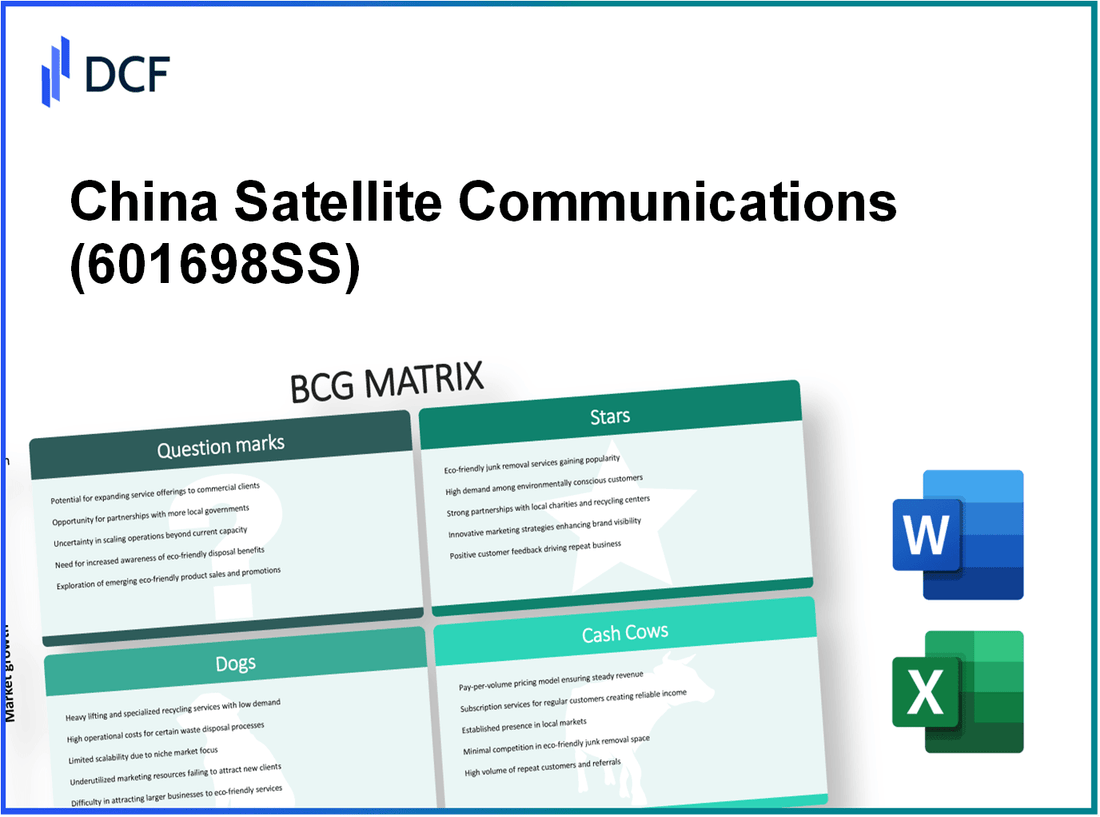

China Satellite Communications Co., Ltd. (601698.SS) - BCG Matrix Analysis: Stars

Stars

High-throughput satellite (HTS) broadband services are a core 'Star' for China Satellite Communications. The company has leveraged the 2025 operational status of ChinaSat 26 and the upcoming ChinaSat 27 (projected to deliver ~300 Gbps of capacity to Eurasia and Africa) to capture rapid expansion in China and the broader Asia‑Pacific HTS market. The Asia‑Pacific HTS revenue market is forecast to grow at a 24.2% CAGR through 2032, outpacing legacy GEO and FSS segments. China Satcom's HTS capability underpins an overall satellite communications market CAGR of 13.06% in China, positioning the company to monetize the projected ~1.8 billion mobile internet users in the region by 2030 through high‑capacity backhaul, fixed wireless access and enterprise connectivity.

| Metric | HTS Broadband Services | Maritime & Aviation Connectivity | Government & Defense Solutions |

|---|---|---|---|

| Relevant CAGR (regional / segment) | Asia‑Pacific HTS revenue CAGR 24.2% (through 2032) | Maritime satellite market CAGR 11.1% (through 2033) | Chinese satellite market CAGR 12% (2025-2030) |

| China Satcom market position | Dominant HTS provider; anchor GEO‑HTS fleet | High market share in maritime VSAT; leading regional supplier | Primary state provider for secure communications |

| Key capacity / assets | ChinaSat 26 (operational 2025); ChinaSat 27 (~300 Gbps capacity) | GEO‑HTS fleet, VSAT terminals; maritime VSAT = 65.9% of maritime type (2024) | High‑capacity transponders, secure terminals, integrated 5G‑satellite solutions |

| Demand drivers (quantified) | ~1.8 billion mobile internet users in region by 2030; HTS market growth 24.2% CAGR | 90% of global trade by shipping; Asia‑Pacific = 34.6% of global maritime sat market; VSAT 65.9% share (2024) | China government space spending ≈ $20 billion (2024); long‑term state contracts |

| Revenue / ROI dynamics | High ARPU opportunities from broadband, FWA, enterprise and backbone services; significant capex to sustain growth | Recurring VSAT service revenues; high lifetime value from maritime & aviation contracts | Stable, high‑margin contracts; strong ROI from long‑term service agreements and strategic prioritization |

Maritime and aviation connectivity are concurrent Stars: China Satcom's GEO‑HTS fleet supports VSAT services that captured a 65.9% share of the maritime type segment in 2024. The maritime market in China led the region in 2024 and is projected to grow at an 11.1% CAGR through 2033. With ~34.6% of the global maritime satellite market concentrated in the Asia‑Pacific and ~90% of global trade transported by shipping, demand for continuous high‑bandwidth connectivity at sea - plus accelerating in‑flight connectivity demand - drives robust, recurring revenue streams.

- HTS capacity expansion (ChinaSat 26/27) directly supports exponential bandwidth monetization across fixed, mobile and mobile‑platform verticals.

- Maritime & aviation VSAT deliveries generate high ARPU, long contract duration and strong installed‑base churn resistance.

- Geographic coverage (Eurasia/Africa via ChinaSat 27) enables cross‑border commercial growth and international service contracts.

Government and defense communications form another high‑share Star within China Satcom's portfolio. China's government space spending reached approximately $20 billion in 2024, sustaining large procurement and service relationships. The government/defense segment uses secure, high‑capacity transponders and tactical terminal solutions, contributing to the projected 12% CAGR for China's satellite market from 2025 to 2030. Integration of 5G and satellite infrastructure expands mission profiles (tactical backhaul, secure broadband, resilience), ensuring long‑duration contracts and predictable service revenues.

- State contracts provide durable revenue streams and high gross margins due to security requirements and scale.

- 5G‑satellite integration increases value per service and expands addressable TAM in public sector digital inclusion initiatives.

- High capital investment in payloads and ground infrastructure is matched by multi‑year contracted cash flows and favorable ROIs.

China Satellite Communications Co., Ltd. (601698.SS) - BCG Matrix Analysis: Cash Cows

Cash Cows

Traditional C-band and Ku-band transponder leasing remains China Satellite Communications' primary revenue generator, representing the core mature business with dominant domestic market share and predictable cash flow. The global satellite transponder market was valued at approximately $14.9 billion in 2024, with leasing accounting for roughly 77.7% of that revenue. Within this context, China's GEO transponder leasing operates with a low industry growth rate-estimated between 3.8% and 4.5% annually-yet China Satcom's effective domestic monopoly on GEO capacity ensures sustained utilization and contract longevity.

These traditional assets require relatively low incremental capital expenditure compared with investments in HTS (High-Throughput Satellites) or LEO (Low Earth Orbit) constellations. As a result, operating margins on transponder leasing are higher than capital-intensive segments. For fiscal reference, China Satcom reported approximately CNY 2.64 billion in annual revenue attributable to core GEO leasing and related services, supported by long-term contracts with broadcasters and enterprise VSAT customers.

| Metric | Value | Source/Notes |

|---|---|---|

| Global transponder market size (2024) | $14.9 billion | Market estimate for global transponder services |

| Leasing revenue share | 77.7% | Portion of market driven by leasing vs. other services |

| Traditional band CAGR (C-/Ku-band) | 3.8%-4.5% | Projected market growth range for mature bands |

| China Satcom annual revenue (core GEO leasing) | CNY 2.64 billion | Company reported/segment-attributable estimate |

| GEO platform global revenue share (platform market) | 68.7% | Share of platform revenues attributed to GEO systems |

| Broadcasting transponder leasing CAGR | 4.43% | Leasing growth rate specific to broadcast use |

| Typical contract length (DTH, VSAT) | 5-15 years | Range for long-term service agreements |

| Typical utilization rate (domestic GEO fleet) | 85%-95% | Estimated steady-state capacity utilization |

Satellite TV broadcasting remains a high-margin, consistent income source for China Satcom. GEO platforms account for approximately 68.7% of global satellite platform revenue, and broadcasting continues to be a core vertical for transponder leasing. Despite competition from internet-based video delivery, the push for higher-resolution content (HD, UHDTV) supports ongoing demand: transponder leasing for broadcasting is growing at an estimated CAGR of 4.43%.

China Satcom's domestic video distribution benefits from extensive coverage, established relationships with national and regional broadcasters, and low customer churn. These factors combine to produce predictable revenue streams that are strategically used to fund the company's investments in next-generation capabilities such as HTS payloads and participation in LEO projects.

- Primary cash generation: C-/Ku-band transponder leasing with long-term contracts (DTH broadcasters, enterprise VSAT).

- Revenue contribution: Core GEO services underpin CNY 2.64 billion in annually recurring revenue.

- Margin profile: Higher operating margins due to low incremental CAPEX versus HTS/LEO investments.

- Market positioning: Effective domestic monopoly in GEO services driving 85%-95% utilization.

- Use of cash: Funding R&D, HTS deployment, and strategic LEO partnerships.

China Satellite Communications Co., Ltd. (601698.SS) - BCG Matrix Analysis: Question Marks

Question Marks - Dogs: this chapter focuses on China Satellite Communications Co., Ltd. (China Satcom) exposures that sit in high-growth markets where the company currently holds a low relative market share, specifically Low Earth Orbit (LEO) satellite internet ventures and satellite-based IoT/M2M connectivity. Both are capital-intensive initiatives with uncertain short-term returns and are categorized as Question Marks in the BCG framework.

Low Earth Orbit (LEO) satellite internet ventures represent a high-growth opportunity with China Satcom's current market share remaining low versus both domestic state-backed competitors and global incumbents. The national 'Guowang' program targets a final constellation size of approximately 13,000 satellites; as of late 2025 the deployed Guowang satellites exceeded 100 units-about 0.77% of the stated target. China Satcom's share of active LEO payloads is estimated at under 5% of China's combined state and commercial LEO assets.

| Metric | Guowang Program (China) | China Satcom Role | Global Benchmark (Starlink) |

|---|---|---|---|

| Target Constellation Size | 13,000 satellites | Participation in multi-actor deployments | ~12,000+ deployed (2025) |

| Satellites Deployed (late 2025) | >100 | <5 active payloads (company estimate) | ~5,000-12,000 (varies by source) |

| China Satcom Estimated Market Share (LEO Internet) | n/a (national program) | <5% | Starlink: ~60-70% global LEO retail market |

| Addressable Market (China D2C Satellite-to-Cell by 2030) | 30 million users (forecast) | Target segment | Global LEO broadband users forecast: 50-150 million by 2030 |

| CAPEX Requirement (est.) | Program-level: tens of billions USD | China Satcom incremental capex: hundreds of millions to several billions USD | Starlink capex to date: >$10B (launch + production) |

| Immediate ROI | Low in near term | Uncertain | Delayed multi-year ROI |

Key dynamics for LEO ventures:

- High addressable domestic market: satellite direct-to-cell services forecast to reach 30 million Chinese users by 2030.

- Massive CAPEX and OPEX: program-level investment in launch, manufacturing, ground infrastructure and spectrum licensing estimated in the multiple billions USD range.

- Competitive landscape: domestic state-backed players (China SatNet, provincial consortia), commercial entrants ("Thousand Sails") and global incumbents (SpaceX/Starlink).

- Operational cadence constraints: success tied to launch cadence, mass-production yield, and regulatory approvals; current deployment (100+ Guowang satellites) is a small fraction of planned scale.

Satellite-based IoT and M2M connectivity services are another high-growth area where China Satcom currently has low revenue contribution. The global satellite IoT market is projected to transition into significant revenue generation beginning in 2025, with forecasts aligned to the broader cellular IoT landscape targeting approximately 10.6 billion cellular IoT devices by 2032. China's satellite communications market growth rate is estimated at 13.06% CAGR, but the specific satellite IoT sub-segment is in early adoption among verticals such as smart manufacturing, utilities, logistics and agriculture.

| Metric | Global Satellite IoT Forecast | China Satellite IoT Context | China Satcom Position |

|---|---|---|---|

| Key Forecast Horizon | Revenue ramp from 2025; device growth through 2032 | Early adoption 2023-2028; industrial pilots ongoing | Exploratory payloads and pilots |

| Addressable Devices | 10.6 billion cellular IoT devices by 2032 | China share: large proportion of devices given domestic manufacturing base | Targeting niche verticals - estimated <1% market share initially |

| Market Growth Rate | Satellite communications market CAGR: ~13.06% (China) | Satellite IoT sub-segment: variable; early double-digit potential | Projected company segment growth: 15-20% if successful |

| Revenue Contribution (Current) | Minimal at global level for satellite-specific IoT | Low in China; pilots generate nominal revenue | <5% of China Satcom service revenue (estimate) |

| Investment Needs | R&D for low-power terminals, LEO compatible payloads, ground segment | High upfront R&D; ecosystem partnerships required | Significant R&D and capex required; partnerships with startups and chip vendors |

Key dynamics for Satellite IoT / M2M:

- High potential scale: integration with a projected 10.6 billion cellular IoT devices by 2032 implies meaningful addressable opportunity for satellite reach in coverage-limited scenarios.

- Revenue timing risk: meaningful revenue ramp expected post-2025 as device ecosystems and standards mature.

- Competitive field: numerous specialized startups and telecom vendors targeting narrow verticals create a medium-concentration market that challenges incumbents to differentiate.

- Technical barriers: requirement for ultra-low-power terminals, near-real-time communications for critical infrastructure, and interoperability with 3GPP NB-IoT and LTE-M standards.

Risk and investment profile across the Question Marks segment:

| Dimension | LEO Internet | Satellite IoT / M2M |

|---|---|---|

| Estimated CAPEX (company incremental) | $500M-$3B (platform + payloads + ground) | $50M-$300M (R&D, pilots, terminals) |

| Time to meaningful revenue | 5-10 years | 3-7 years |

| Competitive intensity | Very high (domestic & global) | High (many niche specialists) |

| Strategic dependencies | Launch cadence, spectrum, national policy, manufacturing scale | Standards alignment (3GPP), chipsets, partnerships with integrators |

| Upside (market capture scenario) | Millions of subscribers; multi-billion USD annual revenue potential | Hundreds of millions to >$1B annual revenue in high-adoption cases |

Strategic considerations and operational constraints relevant to the Dogs/Question Marks category:

- Launch cadence remains a bottleneck: achieving thousands-scale constellations requires multiple launches per month; domestic launch capacity and cost per kg are decisive.

- Capital allocation trade-offs: prioritizing LEO internet vs. IoT initiatives requires clear hurdle rates given constrained free cash flow and competing legacy GEO services.

- Partnership and ecosystem strategies: leveraging state programs (Guowang), commercial consortia, and global suppliers can de-risk technology gaps but reduces exclusive share.

- Regulatory and spectrum risk: allocation for direct-to-cell and IoT spectrum must be secured; policy changes could materially influence addressable market timing.

- R&D intensity: developing low-power, low-cost terminals and efficient payloads is essential to capture the projected ~20% growth driver in IoT-related services.

China Satellite Communications Co., Ltd. (601698.SS) - BCG Matrix Analysis: Dogs

Dogs

Legacy narrowband mobile satellite services (MSS) represent a Dog for China Satellite Communications: declining relevance, low market growth and shrinking market share as customers migrate to broadband HTS and terrestrial 5G-integrated alternatives. Revenue from legacy MSS is now a marginal component of total company sales-internal estimates place MSS revenue contribution at approximately 3-5% of consolidated revenue in recent years-while maintenance and operating costs have risen roughly 12-18% year-on-year as the fleet ages and spare-part scarcity increases.

Key metrics for the legacy MSS segment:

| Metric | Value | Notes |

|---|---|---|

| Revenue contribution | 3-5% of total revenue | Company internal estimate (most recent fiscal year) |

| Annual operating cost increase | 12-18% YoY | Maintenance, ground segment, legacy handset support |

| Relative market share (segment) | < 10% | Global MSS players and new entrants dominate |

| Segment market growth | ~0% to negative | Users migrating to HTS and 5G; declining ARPU |

| Relevant industry CAGR | HTS market: 17.2% CAGR | Contrast highlights strategic mismatch |

| ROI outlook (5-year) | Negative to low single digits | Without major overhaul or conversion to HTS |

In oversupplied regional transponder markets, particularly in select Pacific Island and African corridors, China Satcom's older GEO capacity functions as a Dog: low growth, intense price competition and compressed margins. In these niches, transponder utilization and average revenue per MHz have declined, with market growth often falling below global averages and utilization rates drifting under breakeven thresholds for older satellites.

Transponder segment snapshot:

| Metric | Value | Notes |

|---|---|---|

| Regional transponder growth | < 4.7% (often 0-2%) | Below global average of 4.7% |

| Capacity utilization (selected markets) | 40-60% | Oversupply due to GEO-HTS entrants |

| Average price per MHz-month | Decline of 20-35% over 3 years | "Capacity dumping" pressure |

| China Satcom regional market share | 5-15% by transponder-km | Loss to local and global HTS operators |

| CAPEX priority | Low | Funds reallocated to domestic HTS and strategic missions |

Drivers that lock these assets into the Dog quadrant include:

- Technological obsolescence: legacy MSS and older GEO transponders cannot match HTS throughput (HTS CAGR 17.2%).

- Price competition: capacity dumping in select regions reduces ARPU by 20-35% over three years.

- Low market growth: certain regional niches show 0-2% growth vs. global transponder average 4.7%.

- Rising operating costs: maintenance and fleet-support costs up 12-18% YoY for aging satellites.

- CAPEX reallocation: preference for domestic/high-value HTS and strategic payloads lowers reinvestment in Dogs.

Financial and strategic consequences for China Satcom:

| Area | Impact | Quantified effect |

|---|---|---|

| Short-term EBITDA | Downward pressure | Legacy MSS/transponder margin contraction of 5-12 percentage points |

| CAPEX allocation | Reduced reinvestment | Reprioritized ~30-50% of incremental CAPEX toward HTS/domestic projects |

| Strategic focus | Shift to HTS & national projects | Lower strategic value for Dogs; potential asset decommissioning |

| Cashflow | Weakening from segment | MSS/transponder cashflow contribution trending toward breakeven or negative within 3-5 years |

Management options for these Dogs (operational levers and potential outcomes):

- Divest or lease older transponder capacity to third parties - potential one‑time proceeds offset by reduced recurring revenue.

- Repurpose airtime/ground infrastructure for value-added services (IoT overlay, government backup) - limited upside but can stabilize utilization.

- Selective retrofit to HTS-capable payloads where technically feasible - high CAPEX, long payback; generally not viable for most legacy MSS assets.

- Decommission aging satellites to cut opex and reallocate funds - immediate opex relief, near-term service disruption risks.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.