|

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS): BCG Matrix [Dec-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS) Bundle

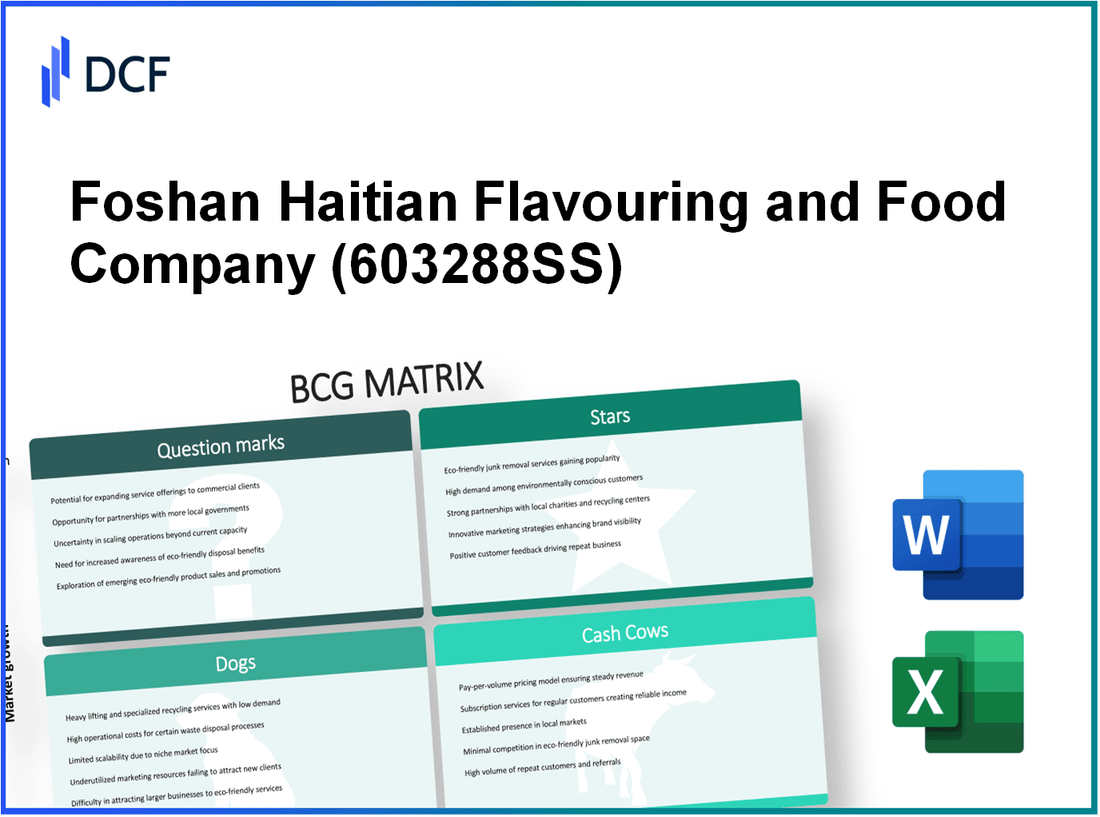

Foshan Haitian's portfolio is sharply bifurcated: high-margin Stars-oyster sauce and premium zero‑additive soy-are driving growth and commanding targeted CAPEX and R&D, while entrenched Cash Cows-core soy sauce and seasoning pastes-generate the steady cash flow financing that expansion; Question Marks like vinegar, cooking wine and hot‑pot bases show rapid market upside but demand heavy marketing and investment to scale, and Dogs such as bulk catering soy and grain & oil are being deprioritized with frozen CAPEX-a capital-allocation stance that prioritizes premiumization and selective market entry, making this a pivotal moment for the company's next growth phase.

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS) - BCG Matrix Analysis: Stars

Stars

DOMINANT OYSTER SAUCE MARKET EXPANSION

Haitian's oyster sauce segment qualifies as a Star: it contributes approximately 18.5% of total corporate revenue (late 2025), holds a 42.0% domestic market share in the oyster sauce category, and is growing at an annual rate of 11.2%, well above the condiment industry average. Gross margin for the segment is 35.4%, underpinned by scale manufacturing and process optimization. Management allocated 8.5% of total 2025 CAPEX to expand oyster sauce production capacity, and the segment-level return on investment (ROI) stands at 14.2%.

| Metric | Value |

|---|---|

| Revenue contribution to company | 18.5% |

| Domestic market share (oyster sauce) | 42.0% |

| Annual segment growth | 11.2% |

| Gross margin | 35.4% |

| 2025 CAPEX allocation (share of total) | 8.5% |

| Segment ROI | 14.2% |

| Estimated 2025 segment revenue (RMB) | Assuming company revenue of 45.0 billion RMB: ~8.33 billion RMB |

| Unit cost improvement (3-year trend) | ~6.0% reduction vs. 2022 baseline |

Strategic levers and operational priorities for the oyster sauce Star include capacity scaling, SKU rationalization toward premium and value tiers, logistics optimization for shorter lead times, targeted trade promotions in high-growth provinces, and cross-selling into institutional foodservice channels to protect share as the category matures.

- Production: Add two high-efficiency filling lines by H2 2026 to support projected volume increase of 15% YoY.

- Pricing: Maintain margin via tiered pricing and cost-plus contracts for key distributors.

- Distribution: Expand cold-chain and FMCG retail penetration in lower-tier cities to sustain growth momentum.

- Marketing: Allocate incremental marketing budget equivalent to 0.4% of segment revenue to support brand loyalty programs.

PREMIUM ZERO ADDITIVE PRODUCT GROWTH

The premium Zero Additive soy sauce sub-segment is a high-growth Star within the soy sauce portfolio. It accounts for 15.2% of total soy sauce revenue, is growing at 22.5% year-over-year driven by rising health-conscious consumption, and commands a 30.1% share of the high-end soy sauce market. Gross margins are elevated at 45.6% due to premium pricing and lower promotional intensity. Haitian invested 500 million RMB in 2025 in R&D and marketing specifically for the Zero Additive series; post-investment brand equity in urban tier-one markets increased by 12.8% (brand awareness and preference index). ROI on the Zero Additive initiative is currently trending toward double-digit returns as distribution and ASPs scale.

| Metric | Value |

|---|---|

| Share of soy sauce revenue (Zero Additive) | 15.2% |

| YoY growth | 22.5% |

| Market share (high-end soy sauce) | 30.1% |

| Gross margin | 45.6% |

| 2025 investment (R&D & marketing) | 500 million RMB |

| Brand equity increase (tier-one urban) | +12.8% |

| Estimated average selling price (ASP) premium vs. standard | ~+38% |

| Estimated contribution to company gross profit (RMB) | Assuming soy sauce segment gross profit of 6.5 billion RMB: Zero Additive ~0.99 billion RMB |

- R&D focus: Continued product formulation, shelf-life testing, and label certifications to support premium positioning.

- Channel strategy: Accelerate premium placement in modern trade, e-commerce flagship stores, and gourmet food outlets.

- Pricing and margin management: Preserve 45%+ gross margin by limiting discounting and using value-added bundling.

- Brand building: Leverage the 500 million RMB investment to increase penetration in top-tier city households and premium foodservice accounts.

Collectively, these Stars (oyster sauce expansion and Zero Additive premium soy sauce) exhibit high relative market share and strong market growth, justify continued CAPEX and marketing investment, and are positioned to transition into cash-generating Heavyweights as category growth moderates while retaining high profitability.

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS) - BCG Matrix Analysis: Cash Cows

Cash Cows

CORE SOY SAUCE REVENUE ANCHOR

The traditional soy sauce category remains the company's primary cash generator, contributing 51.4% of total turnover and holding an 18.2% share of the national soy sauce market. Market growth is mature at 4.5% annually. Net profit margins for this business unit are steady at 24.3%, while maintenance CAPEX is low at 3.2% of segment revenue. Management uses the sizable free cash flow from this unit to fund R&D, geographic expansion in adjacent condiment categories, and marketing tests for premium SKUs.

| Metric | Value (percent of total turnover) | Unit-level metric |

|---|---|---|

| Share of company revenue | 51.4% | per 100 RMB total revenue = 51.40 RMB |

| National market share (soy sauce) | 18.2% | relative position in fragmented market |

| Segment growth rate | 4.5% | annual |

| Net profit margin | 24.3% | of segment revenue |

| Maintenance CAPEX | 3.2% | of segment revenue |

| Estimated operating cash flow margin | 21.0% | of segment revenue (derived from net margin minus non-cash items and reinvestment) |

| Cash generated per 100 RMB company revenue | 51.4 21.0% = 10.79 RMB |

- Primary uses of soy sauce cash flows: funding diversification into new seasoning categories, selective acquisitions, working capital for high-turnover SKUs.

- Cost advantages sustained by scale purchasing of soybeans and optimized bottling lines reduce variable cost volatility.

- Risks: margin pressure if raw-material commodity spikes occur or if premiumization cannibalizes base portfolio.

SEASONING PASTE STABLE MARKET POSITION

The seasoning paste and compound sauce segment contributes 11.8% of 2025 total revenue and holds a 15.4% share in its domestic category. This mature segment grows roughly 3.8% annually. Strong supply-chain management and procurement produce gross margins of 38.2% and an operating cash flow margin of 21.5%. Marketing investment is deliberately low at 2.1% of the segment's revenue to preserve cash generation while maintaining shelf presence.

| Metric | Value (percent of total turnover) | Unit-level metric |

|---|---|---|

| Share of company revenue | 11.8% | per 100 RMB total revenue = 11.80 RMB |

| Domestic market share (seasoning paste) | 15.4% | stable competitive position |

| Segment growth rate | 3.8% | annual |

| Gross margin | 38.2% | of segment revenue |

| Operating cash flow margin | 21.5% | of segment revenue |

| Marketing spend | 2.1% | of segment revenue |

| Cash generated per 100 RMB company revenue | 11.8 21.5% = 2.54 RMB |

- Cash profile: predictable, low volatility cash surplus supporting central functions and pilot programs for premium/healthier formulations.

- Efficiency levers: procurement contracts, consolidated manufacturing runs, and minimized category-level marketing to sustain high cash conversion.

- Operational constraints: slower organic growth requires reinvestment elsewhere for long-term portfolio rejuvenation.

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS) - BCG Matrix Analysis: Question Marks

Question Marks - VINEGAR CATEGORY STRATEGIC MARKET PENETRATION

The vinegar segment represents 4.2% of total corporate revenue (2025). Domestic vinegar market growth rate: 9.6% CAGR. Haitian vinegar market share: 3.5% national. 2025 CAPEX for vinegar production increased by 20.4% year‑over‑year. Current gross margin: 18.5%, impacted by promotional pricing and initial entry costs. Management target: 15% revenue growth in vinegar for the next fiscal year. Distribution leverage: existing retail footprint of 500,000 terminals intended for rollout. Short‑term unit economics show negative contribution at promotional volumes; break‑even volume projected at ~36 million liters annually under current cost structure.

Key quantitative metrics for vinegar:

| Metric | Value |

|---|---|

| 2025 Revenue Contribution | 4.2% |

| Domestic Market Growth | 9.6% CAGR |

| Haitian Market Share (Vinegar) | 3.5% |

| 2025 Vinegar CAPEX Change (YoY) | +20.4% |

| Gross Margin (Vinegar) | 18.5% |

| Revenue Growth Target (next FY) | 15% |

| Break‑even Volume (Est.) | ~36 million liters/year |

Question Marks - COOKING WINE EXPANSION IN CATERING

Cooking wine products account for 5.1% of total revenue (Dec 2025). Specialized cooking wine industry growth: 14.2% annual, driven by professional catering demand. Haitian market share in specialized cooking wines: ~4.1% national. R&D spend on new formulations increased by 25% in the current fiscal period. Gross margins: 22.3% under pressure from competitive pricing. Marketing and promotional intensity high: advertising expenses represent 8.5% of cooking wine segment sales. Channel strategy emphasizes institutional sales to catering chains; target gross margin improvement to 26% within 18 months via premium SKUs and cost efficiencies.

Key quantitative metrics for cooking wine:

| Metric | Value |

|---|---|

| 2025 Revenue Contribution | 5.1% |

| Industry Growth Rate (Specialized) | 14.2% CAGR |

| Haitian Market Share (Cooking Wine) | 4.1% |

| R&D Spend Increase (YoY) | +25% |

| Gross Margin (Cooking Wine) | 22.3% |

| Advertising as % of Segment Sales | 8.5% |

| Target Gross Margin (18 months) | 26% |

Question Marks - COMPOUND SEASONING AND HOT POT BASES

Compound seasoning and hot pot bases represent 1.6% of total 2025 revenue. Category growth: 16.5% annual across China. Haitian market share in this emerging segment: <2.0%. Marketing expenditures for hot pot bases increased by 30% to raise brand visibility. Current gross margin: 28.4% with anticipated scale economies to improve margin to mid‑30s at higher volumes. Company leverages 500,000 retail terminals and institutional channels to accelerate penetration. Short‑term sales targets: increase segment revenue by 40% year‑over‑year; investment focus on co‑branding with regional hot pot chains and SKU localization.

Key quantitative metrics for compound seasoning & hot pot bases:

| Metric | Value |

|---|---|

| 2025 Revenue Contribution | 1.6% |

| Category Growth Rate | 16.5% CAGR |

| Haitian Market Share | <2.0% |

| Marketing Spend Increase (Hot Pot) | +30% |

| Gross Margin (Current) | 28.4% |

| Target Margin at Scale | Mid‑30s % |

| Retail Terminals Leveraged | 500,000 |

| Short‑term Revenue Growth Target | +40% YoY |

Consolidated view and tactical priorities for these Question Marks

- Resource allocation: prioritize CAPEX and targeted marketing to vinegar (20.4% CAPEX increase) and compound seasoning (30% marketing increase) while monitoring ROI quarterly.

- Margin recovery: implement price architecture, reduce promotional depth, and improve scale efficiencies to raise margins from 18.5% (vinegar) and 22.3% (cooking wine) toward target thresholds (mid‑20s to mid‑30s).

- Distribution leverage: activate 500,000 retail terminals and institutional catering channels to convert market growth into share gains (targets: vinegar +15% revenue; hot pot +40% revenue).

- R&D and product differentiation: sustain R&D boost (cooking wine +25%) to develop higher‑margin premium SKUs and regionally tailored formulations.

- Performance KPIs: segment revenue growth, gross margin improvement, customer acquisition cost, promotional depth, and break‑even volume for vinegar to be tracked monthly.

Foshan Haitian Flavouring and Food Company Ltd. (603288.SS) - BCG Matrix Analysis: Dogs

Dogs - BULK CATERING SOY SAUCE SEGMENT

The low-end bulk soy sauce for the catering industry accounts for 5.2% of Haitian's consolidated revenue but shows characteristics of a 'Dog' within the BCG framework: low market growth, weak relative market share, thin margins and minimal ROI. Annual segment revenue is estimated at RMB 2.34 billion (5.2% of total), with a year-on-year growth rate of only 2.1%. Gross margin for the segment is 8.4%, significantly below the corporate average. Haitian's market share in the low-tier bulk catering soy sauce market has declined to 12.5% from 16.8% three years prior. Reported ROI for this business unit is approximately 4.2%, the lowest in the portfolio, and below the company weighted average cost of capital (WACC ~7.5%). Management has frozen CAPEX for new bulk production capacity and reallocated investment toward premiumization initiatives.

| Metric | Value |

|---|---|

| Contribution to Total Revenue | 5.2% (RMB 2.34bn) |

| Segment Growth Rate (YoY) | 2.1% |

| Gross Margin | 8.4% |

| Haitian Market Share (low-tier bulk) | 12.5% |

| ROI | 4.2% |

| CAPEX Status | All new bulk production CAPEX frozen |

| Competitive Dynamics | Intense price competition from local unbranded producers |

Key operational and financial pressures for the bulk catering soy sauce segment include margin compression from spot-price driven raw material procurement, channel concentration risk with major foodservice distributors, and limited product differentiation versus local commoditized alternatives.

- Operational risks: high reliance on cost-leadership, vulnerability to soy/fermentation input price swings.

- Financial constraints: sub-WACC ROI limits ability to fund modernization or automation for this line.

- Strategic posture: maintain supply to key catering customers while minimizing further investment; evaluate potential divestiture or contract-manufacturing partnerships.

Dogs - NON CORE GRAIN AND OIL PRODUCTS

The grain and oil division (rice and cooking oil) is a marginal revenue contributor at 1.8% of consolidated sales, estimated at RMB 0.81 billion. Market growth is effectively flat at 1.5% annually in a highly commoditized national market. Haitian's national market share in this category stands at 0.5%, indicating negligible competitive positioning. Gross margin is extremely low at 6.2%, primarily eroded by commodity price parity and elevated logistics and storage costs. ROI for this segment is estimated at 2.8%, below the firm's cost of capital and operationally loss-averse. Management classifies the division as non-core with no expansion planned for fiscal 2026 and limited marketing or capital allocation.

| Metric | Value |

|---|---|

| Contribution to Total Revenue | 1.8% (RMB 0.81bn) |

| Segment Growth Rate (YoY) | 1.5% |

| Gross Margin | 6.2% |

| Haitian Market Share (grain & oil) | 0.5% |

| ROI | 2.8% |

| Strategic Status | Non-core, no expansion planned for 2026 |

| Cost Structure Pressure | High logistics and storage costs relative to margins |

Principal issues for the grain and oil line include scale disadvantages, exposure to thin commodity spreads, and distribution inefficiencies relative to established national players. The segment's economics do not justify incremental marketing spend or capacity investment under current corporate strategy.

- Possible near-term actions: maintain minimal operational footprint, pursue asset-light supply agreements, or seek divestment to local commodity specialist.

- Cost levers: reduce warehousing footprint, optimize logistics routes, renegotiate supplier terms to protect cash flows.

- Exit criteria: inability to achieve ROI above WACC within a 24-36 month horizon or failure to secure strategic partner interest.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.