|

Colgate-Palmolive Company (CL): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Colgate-Palmolive Company (CL) Bundle

You're looking at a giant, a company pulling in nearly $20.0 billion in revenue, and you need to know if that engine is running smoothly against market headwinds as of late 2025. Honestly, even a dominant player with a 41.2% global toothpaste share isn't immune; we see supplier costs squeezing margins toward 60.1% and massive retailers dictating terms. So, I've mapped out the full competitive landscape-from the threat of cheaper substitutes to the sheer cost of fighting rivals like Procter & Gamble-to give you a clear, precise picture of the risks and where the real power lies in this essential consumer goods business.

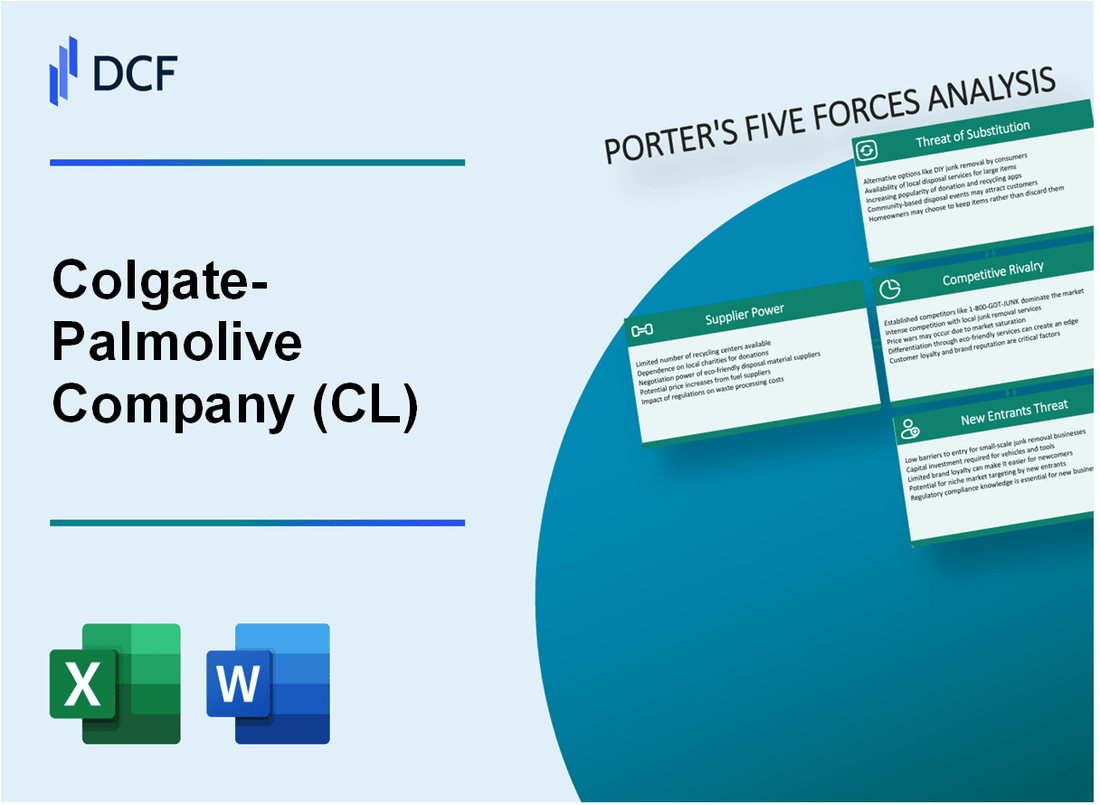

Colgate-Palmolive Company (CL) - Porter's Five Forces: Bargaining power of suppliers

You're analyzing the supplier landscape for Colgate-Palmolive Company as of late 2025, and honestly, the pressure from input costs is a major theme right now. Raw material costs, especially for packaging and resins, are definitely squeezing margins.

Rising raw material costs, like packaging and resins, pressured gross margin to 60.1% in 2025 YTD. To be fair, in the third quarter alone, raw and packaging materials had a 600 basis point negative impact on gross profit margin, driven by higher costs for fats and oils, among other things.

Trade policy adds another layer of complexity. Tariffs, like the 25% levy on Mexican imports, increase input costs for US-bound products. This is particularly relevant because approximately 40% of US-bound toothpaste is manufactured in Mexico. While the company expects an approximate $75 million impact from tariffs finalized as of October 29, 2025, this highlights the direct financial exposure to supplier-adjacent government actions.

Still, Colgate-Palmolive Company's sheer size offers some defense against supplier leverage, particularly for high-volume commodity ingredients. The company's global scale allows for global sourcing flexibility, defintely mitigating single-supplier risk. The company has also invested $2 billion in its US supply chain since 2020, which includes increasing US manufacturing facilities by more than 40% in the last five years, creating alternative sourcing options.

Here's a quick look at how these supplier-related factors stack up against the company's market scale:

| Factor | Metric | Value | Context/Timing |

|---|---|---|---|

| Gross Margin (GAAP) | Margin Percentage (YTD 2025) | 60.1% | Year to Date 2025 |

| Input Cost Pressure | Raw & Packaging Materials Negative Impact (Q3 2025) | 600 basis points | Q3 2025 |

| Tariff Exposure | Expected Cost from Finalized Tariffs (2025) | $75 million | Based on tariffs finalized as of Oct 29, 2025 |

| Mexican Sourcing Vulnerability | Tariff Levy on Mexican Imports | 25% | Specific Tariff Rate |

| Mexican Sourcing Vulnerability | Percentage of US-Bound Toothpaste from Mexico | 40% | Volume Percentage |

| Market Scale (Oral Care) | Global Toothpaste Value Share (YTD 2025) | 41.2% | Year to Date 2025 |

| Market Scale (Oral Care) | US Toothpaste Value Share (YTD 2025) | 33.4% | Year to Date 2025 |

The ability to command favorable terms is supported by the company's significant market presence, which translates to high volume purchasing power:

- High volume purchasing power offsets supplier leverage for commodity ingredients.

- Company's scale allows for global sourcing flexibility, defintely mitigating single-supplier risk.

- Global leadership in toothpaste at 41.2% value share YTD 2025 provides negotiation leverage.

- The company's funding-the-growth initiatives delivered a 290 basis point benefit to gross profit margin in Q3 2025.

Finance: draft 13-week cash view by Friday.

Colgate-Palmolive Company (CL) - Porter's Five Forces: Bargaining power of customers

You're looking at the power customers hold over Colgate-Palmolive Company (CL), and frankly, it's substantial, especially in the highly competitive North American market. The sheer scale of major retailers means they dictate terms, and Colgate-Palmolive has to play ball.

- - Large retailers (Walmart, Kroger) wield immense power over shelf space and pricing terms.

The dependency on a few massive players is clear when you see that Walmart Inc. (WMT) alone accounts for roughly 11% of Colgate-Palmolive's total sales. This concentration gives these buyers significant leverage in distribution agreements and slotting fees. In the third quarter of 2025, the company noted persistent pricing pressures specifically in North America.

- - Low switching costs for end-consumers drive price sensitivity, especially in non-premium segments.

For everyday items like toothpaste or soap, switching brands is easy, so consumers are definitely price-sensitive. This is evident in the performance metrics. For instance, in the first quarter of 2025, North America saw net sales decline by 3.6% due to inflation and tightened consumer spending. While the company is pushing premiumization, the core segments feel the pinch of low switching costs immediately.

- - Economic uncertainty pushes consumers to cheaper alternatives, impacting volume growth.

When the economy feels shaky, people trade down, which directly hits volume. In Q3 2025, category volume growth remained under pressure because consumers were exhibiting behavior consistent with purchasing around paycheck cycles. This cautious environment meant that while the company achieved an organic sales increase of 1.4% in Q1 2025, the underlying volume dynamics were challenging.

- - Retailer consolidation increases their negotiation leverage in distribution agreements.

The threat of massive consolidation among buyers remains a structural risk. You only need to look at the failed $25 billion Kroger-Albertsons merger to see the scale of potential power shifts in the retail landscape. Even as some deals stall, large-cap and retail players have strengthened their balance sheets in the first half of 2025, potentially positioning them for more active Mergers and Acquisitions (M&A) consideration later in the year, which only tightens the negotiation vise on CPG companies like Colgate-Palmolive.

Here is a quick look at some relevant figures from the recent reporting periods that illustrate the environment Colgate-Palmolive is navigating with its customer base:

| Metric | Value/Period | Source Context |

|---|---|---|

| Walmart Share of CL Sales | Roughly 11% | Q3 2025 Sales Dependency |

| North America Volume Change | Declined -0.5% | Q3 2025 |

| Global Toothpaste Market Share (YTD) | 41.1% | Q2 2025 |

| Q1 2025 Pricing Improvement | +1.5% Year-over-Year | Driven by segmental divisions |

| Q1 2025 Organic Sales Growth | 1.4% | Despite FX headwinds |

To counter this, Colgate-Palmolive is leaning heavily on premium innovation, reporting a 1.5% pricing improvement in Q1 2025, which helped offset some of the volume softness. Still, managing the shelf space and pricing terms with giants like Walmart remains a primary focus for the management team.

Colgate-Palmolive Company (CL) - Porter's Five Forces: Competitive rivalry

You're looking at the oral care landscape, and honestly, the competitive rivalry here is a heavyweight bout that never ends. This isn't a sleepy market; it's a constant battle for shelf space and consumer mindshare between established giants. It's definitely a high-stakes game where brand loyalty is hard-won and easily lost.

Colgate-Palmolive maintains a dominant position, which is key to understanding the dynamic. As of the latest available data for 2025 year-to-date, Colgate-Palmolive holds a global toothpaste share of 41.2%. That's a commanding lead, but the competition is right there, pressing hard. For instance, Procter & Gamble's Crest brand holds a strong counter-position, often cited around the 20% global toothpaste share mark, making them the primary challenger in many key regions.

This rivalry forces continuous, expensive investment. Aggressive marketing and R&D spending are constant, which is just the cost of entry at this level. For example, in Q1 2025, Colgate-Palmolive's advertising investment was 13.6% of net sales, and their guidance for the full year suggested keeping that investment roughly flat as a percentage of sales to defend share. That kind of spending fuels the cycle of continuous innovation you see across the category.

The competition isn't uniform, though; it's category-specific, which creates interesting pockets of focus. While Colgate-Palmolive is the overall leader, P&G is exceptionally strong in specific areas, particularly in North America with Crest and Oral-B. Unilever, with brands like Close-Up and Pepsodent, often focuses its competitive thrust on emerging markets with value and freshness propositions. Here's a quick look at how the major players stack up in the toothpaste segment based on recent estimates:

| Company/Brand | Estimated Global Toothpaste Share (Late 2025 Context) | Primary Competitive Focus |

|---|---|---|

| Colgate-Palmolive (Colgate) | 41.2% | Overall Market Leadership, Therapeutic/Total Care |

| Procter & Gamble (Crest) | Approx. 20% | Premium Science, Whitening, North America |

| Unilever (Close-Up/Pepsodent) | Range of 8% to 12% | Affordability, Freshness, Emerging Markets |

The intensity of this rivalry manifests in several ways you need to watch:

- - Very high rivalry among giants like Procter & Gamble and Unilever.

- - Colgate-Palmolive maintains a dominant 41.2% global toothpaste share YTD.

- - P&G's Crest holds a strong counter-position near 20% share.

- - Aggressive marketing spend, like CL's 13.6% of sales in Q1 2025, is constant.

- - Competition is category-specific; P&G strong in oral care, Unilever in personal care value.

This market structure means any strategic move by one player-a major product relaunch or a shift in pricing-demands an immediate, costly response from the others. Finance: draft 13-week cash view by Friday.

Colgate-Palmolive Company (CL) - Porter's Five Forces: Threat of substitutes

Private-label brands present a direct, lower-cost alternative that pressures the pricing power of Colgate-Palmolive Company's established portfolio. This threat was evident in the first quarter of 2025, where organic sales growth of 1.4% was tempered by a 0.4% negative impact stemming from lower private label pet volume. In response to this dynamic, Colgate-Palmolive Company announced plans to exit the private-label pet nutrition business 'over the course' of 2025.

The appeal of natural and specialty brands is growing, aligning with consumer focus on clean labels and wellness. The broader natural cosmetics market, which includes oral care, is estimated to reach US$23.42 billion by 2028. In the oral care space, which was valued at USD 55,390.1 million in 2025, brands focusing on natural ingredients, such as alcohol-free mouthwash, have seen 'tremendous growth'. Colgate-Palmolive Company is countering this by introducing products like biodegradable toothbrushes and toothpaste made from plant ingredients.

Within the premium Pet Nutrition segment, Hill's Pet Nutrition contends with strong, science-focused substitutes. The competitive landscape in the prescription pet food space for 2025 shows significant revenue figures for its main rivals and itself:

| Prescription Pet Food Brand (2025 Revenue) | Parent Company | 2025 Reported Revenue |

| Royal Canin | Mars, Incorporated | $3.5 billion |

| Hill's Pet Nutrition | Colgate-Palmolive Company | $2.8 billion |

| Purina Pro Plan Veterinary Diets | Nestle Purina PetCare Company | $2.3 billion |

The North America prescription pet food market holds a 46% market share, with veterinary clinics' sales surging 24%. Hill's Pet Nutrition leads the veterinary diet segment, leveraging its Science Diet and Prescription Diet ranges.

Colgate-Palmolive Company's primary defense against generic and trend-driven substitutes is product differentiation, heavily supported by marketing and innovation. The company maintained its global leadership in toothpaste with a market share of 40.9% year to date in Q1 2025, and its manual toothbrush share stood at 31.9%. To reinforce its premium credentials and brand health, advertising investment was robust in 2024, remaining over 13% of net sales. This investment supports premium launches like Colgate Total and elmex, which are leading growth in markets like Latin America and Europe. The company's gross profit margin reached 60.8% in Q1 2025, reflecting success in premium mix management.

Key investments supporting differentiation include:

- Advertising investment at over 13% of net sales in 2024.

- Focus on premium brands like Colgate Total and elmex for higher-margin sales.

- Hill's Pet Nutrition targeting double-digit volume growth potential in key SKUs.

- Science-led innovations in Hill's, such as ActivBiome+ Multi-Benefit.

Colgate-Palmolive Company (CL) - Porter's Five Forces: Threat of new entrants

You're looking at the barriers protecting Colgate-Palmolive Company's dominant position, and honestly, the hurdles for a new player are substantial. The sheer scale of operations required immediately filters out most potential entrants.

High capital expenditure is required for global manufacturing and distribution networks.

To even attempt to match Colgate-Palmolive Company's reach, a new entrant needs deep pockets for physical assets. Consider the last twelve months ending September 30, 2025, where Colgate-Palmolive Company reported capital expenditures (CAPEX) of $571 million. This investment supports a global footprint that spans over 200 countries. To illustrate the scale of investment in this sector, a direct competitor, Procter & Gamble Company, reported CAPEX of $3.98 billion in a comparable period. Setting up the necessary manufacturing capacity and securing shelf space through established distribution channels demands capital far exceeding what a typical start-up can raise.

The required investment level is clearly visible when you map out the necessary financial commitments:

| Metric | Colgate-Palmolive Company (CL) | Procter & Gamble Company (PG) |

| Latest Twelve Months CAPEX (as of 9/30/2025) | $571 million | $3.98 billion |

| 2024 Revenue | $20.10 billion | N/A |

| Global Market Share (Manual Toothbrushes, YTD 2025) | 32.4% | N/A |

Established brand loyalty and trust create a significant barrier to entry.

Consumers show remarkable inertia when it comes to daily use items like toothpaste and soap. Colgate-Palmolive Company's core brands command deep consumer trust, built over decades. This translates directly into market share dominance; for instance, the company holds a global market share of 32.4% in manual toothbrushes year-to-date in 2025. This level of ingrained preference means a new brand must offer a demonstrably superior product or price point to justify switching, which is a tough sell when the incumbent has a market capitalization of approximately $64.52B as of October 2025.

Massive advertising spend is necessary to compete with established brands.

To even gain visibility against the established giants, new entrants must commit to advertising budgets that dwarf those of most other industries. You see this spending pressure even in regional subsidiaries. For example, Colgate-Palmolive (India) Ltd. increased its advertising and promotional (A&P) spending by 8.2% year-on-year to Rs 822.46 crore in Fiscal Year 2024-25 to support innovation and brand health. This continuous, high-volume marketing is essential to maintain top-of-mind awareness, a cost new entrants must immediately absorb.

The necessity for heavy marketing investment is a constant drain on initial capital:

- For the quarter ended June 30, 2024, Colgate-Palmolive India spent approximately Rs 199 crore on advertising expenditure.

- For the quarter ended September 30, 2024, the spend rose to Rs 242.72 crore.

- The company's 2024 revenue was over $20 billion.

Regulatory hurdles for health and personal care products are complex and costly.

Launching health and personal care products means navigating a patchwork of regulations that vary significantly by country and region. New formulations for toothpaste or specialized personal care items face complex testing and approval processes. Varying standards across different regions pose a challenge for companies aiming for global scale, adding significant time and expense before a product can even reach the shelf. This regulatory complexity acts as a non-financial, but very real, barrier to rapid market entry.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.