|

Sypris Solutions, Inc. (SYPR): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Sypris Solutions, Inc. (SYPR) Bundle

You're looking for the real story behind Sypris Solutions' market position as we head into late 2025, and honestly, the picture is a classic split personality. We see suppliers squeezing that $50.4 million market cap through material costs, while the commercial vehicle segment shows customer power clearly-just look at that Q3 revenue dip to $11.5 million-but then you have the defense side, where a 14% backlog increase suggests strong, sticky demand. So, before you make your next move, you need to see how these five forces-from intense rivalry with giants to low threat from new entrants-are truly shaping the playing field for Sypris Solutions right now.

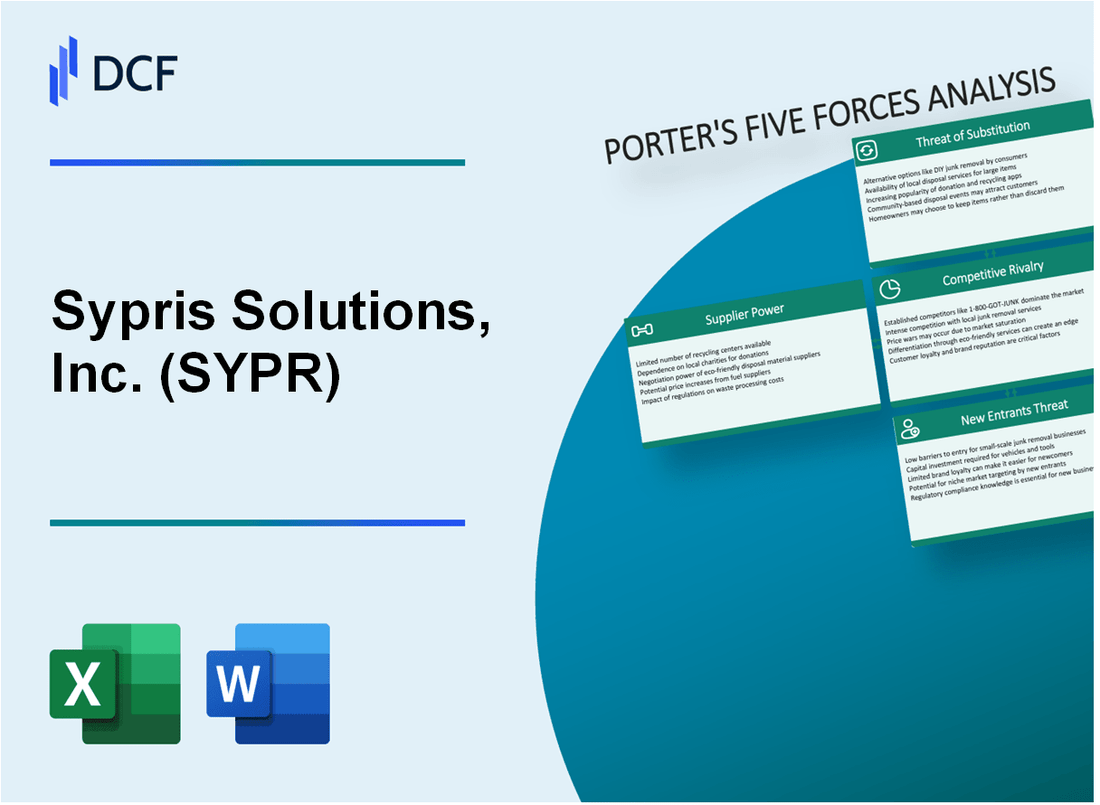

Sypris Solutions, Inc. (SYPR) - Porter's Five Forces: Bargaining power of suppliers

You're looking at the supplier landscape for Sypris Solutions, Inc. (SYPR) as of late 2025, and honestly, the power dynamic leans toward the suppliers, especially for critical inputs. The company's operational hiccups in 2025 clearly show where the leverage lies in the supply chain.

High power due to reliance on a few key suppliers for steel and electronic components.

While Sypris Solutions operates across Technologies (steel components) and Electronics, the impact of material constraints suggests a concentrated supplier base for key raw materials and specialized components. The company's reliance on these specific inputs means that if a few key vendors face their own issues, Sypris Solutions feels the pinch immediately. This is a classic setup for supplier power, especially when the company is not overwhelmingly large in the eyes of a major global supplier.

Material availability issues caused delivery delays and manufacturing inefficiencies in 2025.

We saw direct evidence of this strain throughout 2025. For instance, in the second quarter of 2025, Sypris Electronics faced production inefficiencies directly resulting from material availability issues, which subsequently delayed customer deliveries. This pattern continued into the third quarter of 2025, where material-driven inefficiencies were cited as a factor impacting the Electronics segment's gross margin. When you have out-of-sequence manufacturing, costs jump up, and efficiency drops-that's the direct cost of supplier constraint.

Inflation and tariffs increase raw material costs, pressuring Sypris Solutions' gross margin.

The macro environment certainly didn't help. While tariffs directly impacted transportation-related demand, reducing revenue for Sypris Technologies, the underlying cost pressure from inflation on raw materials, coupled with the general supply chain uncertainty, squeezed profitability. The company had to withdraw its full-year 2025 guidance for Gross Margin Expansion of +150-175 bps, signaling that cost control against external factors was much harder than anticipated. Here's a quick look at how severely margins were compressed in Q3 2025:

| Segment | Q3 2025 Gross Margin (%) | Year-Over-Year Change (Q3 2024 vs Q3 2025) |

|---|---|---|

| Company Total | 7.1% | Down from 16.8% |

| Sypris Electronics | 6.9% | Down from 14.3% |

| Sypris Technologies | 7.5% | Down from 18.8% |

These figures show the direct financial consequence of input cost pressures and operational friction.

Suppliers face limited counter-leverage given Sypris Solutions' $49.054 million market cap.

To be fair, the relationship isn't entirely one-sided. Sypris Solutions, Inc.'s market capitalization as of late November 2025 was approximately $49.054 million, with other readings around $48.06 million or $48.36 million. This relatively small size means that Sypris Solutions, Inc. is likely not a large enough customer for the biggest, most diversified raw material producers to prioritize its needs over those of much larger industrial buyers. Still, for highly specialized components, a small customer base can sometimes give a supplier a temporary edge, but the overall scale limits the supplier's ability to exert massive, sustained price increases without risking the loss of the entire Sypris Solutions, Inc. account.

You should definitely monitor the Electronics backlog, which was over $80 million in Q1 2025, representing more than a full year of sales for that segment. That backlog provides some forward visibility, which helps in negotiating, but it doesn't eliminate the near-term power held by the component providers.

Finance: draft 13-week cash view by Friday.

Sypris Solutions, Inc. (SYPR) - Porter's Five Forces: Bargaining power of customers

You're looking at how Sypris Solutions, Inc.'s customers exert pressure, and honestly, it's a tale of two segments right now. The bargaining power of customers isn't uniform across the business; it really depends on which division you're looking at as of late 2025.

For Sypris Technologies, which serves the commercial vehicle market, customer power looks high. We saw this play out clearly in the third quarter. When large commercial vehicle OEMs (Original Equipment Manufacturers) pull back, Sypris Technologies feels it immediately. This segment's revenue for Q3 2025 was just $11.5 million, a sharp drop from the $19.5 million seen in the prior-year period. That kind of volume impact shows you the leverage those big customers have when they adjust their inventory or when the market cycle turns against them.

The cyclical downturn in the commercial vehicle market definitely gives those customers leverage. They can push for volume adjustments and, naturally, price cuts when demand softens. This dynamic is what we see reflected in the margin compression for Sypris Technologies, whose gross profit margin fell to just 7.5% in Q3 2025 from 18.8% a year earlier. Here's the quick math: the revenue drop in this segment was about 41% year-over-year for the quarter.

The contrast with Sypris Electronics is stark. Here, customer power is significantly lower, which is a huge benefit to Sypris Solutions, Inc. This is because Sypris Electronics operates under multi-year, sole-source contracts, often with defense prime contractors. These long-term commitments lock in demand, insulating the segment from the immediate whims of the commercial cycle.

Check out the revenue comparison for Q3 2025:

| Segment | Q3 2025 Revenue (Millions USD) | Q3 2024 Revenue (Millions USD) |

|---|---|---|

| Sypris Technologies | $11.5 | $19.5 |

| Sypris Electronics | $17.1 | $16.2 |

Sypris Electronics revenue actually grew to $17.1 million in Q3 2025, up from $16.2 million the year before. That growth is directly tied to the stability of their defense customer base. You can see the strength in their order book, too.

The defense-related customer relationships provide a much more stable revenue base:

- Year-to-date orders for Sypris Electronics rose 65% compared to the prior year.

- This robust ordering lifted the Electronics backlog by 14% since the end of 2024.

- Follow-on awards secure production through 2026 for subsea communication modules.

- They received a follow-on award for a classified missile weapons system, with production starting in 2026.

So, while the commercial vehicle customers hold the cards when that market is weak, Sypris Solutions, Inc. has successfully built a counterweight in Sypris Electronics where customers are bound by mission-critical, long-term defense requirements. Finance: draft 13-week cash view by Friday.

Sypris Solutions, Inc. (SYPR) - Porter's Five Forces: Competitive rivalry

When you look at the competitive rivalry facing Sypris Solutions, Inc. (SYPR), you see a company operating at two very different scales, which really defines the pressure in each segment. The sheer size difference in the defense electronics space is stark.

In defense electronics, Sypris Solutions is definitely competing against behemoths. Think about a company like GE Aerospace, which, as of late 2025, commands a market capitalization of approximately $313.22 billion. Sypris Solutions, on the other hand, is a nano-cap at about $48.36 million as of November 21, 2025. That difference in scale-billions versus millions-means that rivals like Lockheed Martin and Northrop Grumman have vastly superior resources for R&D, bidding on large programs, and weathering downturns. Sypris Solutions is defintely a niche player here, relying on specific contract wins, such as the follow-on award from a U.S. Department of Defense prime contractor for electronic warfare and communications systems, which helps build out its backlog, which was reported at over $80 million for Sypris Electronics in Q3 2025.

The competitive intensity is also highlighted when you compare profitability metrics. Sypris Solutions is currently unprofitable, reporting a net loss of $2.05 million in Q2 2025 and a negative return on equity of -12.98%. Its price-to-earnings ratio is reported at -20.15. Contrast that with a major competitor like GE Aerospace, which reported a net margin of 18.34% in its latest results. That gap in margin performance creates significant pricing and investment pressure on Sypris Solutions.

Here's a quick look at the scale difference:

| Metric | Sypris Solutions (SYPR) | GE Aerospace (GE) |

| Market Capitalization (Nov 2025) | $48.36 million | $313.22 billion |

| Employees | 713 | Data Not Found |

| Reported Net Margin (Latest) | Negative (Net Loss of $2.05 million in Q2 2025) | 18.34% |

Now, shift over to Sypris Technologies, which deals in forged and machined components. While direct competitor margin data isn't readily available, the nature of this market is generally characterized by high capital intensity. This means that starting up a local rival requires substantial investment in heavy machinery and specialized facilities, which acts as a barrier to entry, limiting the number of new, local competitors that can easily jump in.

Still, the existing rivalry is felt through market cycles. For instance, in Q3 2025, Sypris Technologies revenue was $11.5 million, down from $19.5 million in Q3 2024, reflecting a cyclical decline in the commercial vehicle market and the impact of converting Mexico shipments to a sub-maquiladora model, which reduced recognized revenue by approximately $1.6 million year-over-year in Q2 2025.

The overall competitive environment for Sypris Solutions can be summarized by its position:

- Defense Electronics: Intense rivalry against firms with market caps in the hundreds of billions.

- Forged Components: High capital intensity limits the number of local entrants.

- Profitability Gap: Competing against peers with net margins over 18% while reporting net losses.

- Company Size: Market Cap of $48.36 million places it firmly in the micro-cap/niche category.

The company's net debt to equity ratio stands at 39.4%, which you have to manage carefully when facing rivals with deep pockets.

Finance: review Q4 2025 capital expenditure plan against the current backlog conversion rate.

Sypris Solutions, Inc. (SYPR) - Porter's Five Forces: Threat of substitutes

You're looking at the threat of substitutes for Sypris Solutions, Inc. (SYPR), and the picture is quite segmented across its business lines. Honestly, the risk profile isn't uniform; it shifts depending on whether you're looking at defense hardware or commercial truck parts.

For the defense sector, the threat of substitution is definitely low. Sypris Electronics operates as a Trusted Source, backed by over 50+ years of experience in high-reliability electronic solutions. They have a 60 years history servicing the military market, working as subcontractors to prime contractors like Lockheed Martin and Northrop Grumman. These long qualification cycles and strict adherence to regulated requirements create significant barriers that keep substitutes out.

The strength in the high-reliability electronics business is clear from the order book. The backlog for Sypris Electronics grew by 14% since the end of 2024. Furthermore, year-to-date orders for Sypris Electronics were up a strong 65% as of the third quarter of 2025.

In the specialty energy products area, specifically pipeline closures, the threat of substitutes is also low because these components are highly engineered and mission-critical. Sypris Solutions, Inc. notes its products are found in challenging projects like the Trans-Alaska Pipeline and the Strategic Petroleum Reserve. This reliance on proven, specialized engineering translates to high switching costs for customers. The market's confidence in this area is reflected in the numbers: the backlog for energy products rose by 59% year-to-date in Q3 2025.

Now, let's look at the commercial vehicle market where the threat feels more moderate. Here, you see the impact of alternative materials or original equipment manufacturers (OEMs) potentially bringing component production in-house. Sypris Technologies, which handles these components, saw its revenue drop sharply by 41% year-over-year in the third quarter of 2025, landing at $11.5 million. That segment's gross profit margin also compressed significantly, falling to 7.5% from 18.8% a year prior.

Here's a quick look at the segment performance that illustrates the substitution pressure in the commercial vehicle space versus the strength in electronics:

| Segment | Q3 2025 Revenue (Millions USD) | Year-over-Year Revenue Change | Q3 2025 Gross Margin (%) |

| Sypris Technologies (Commercial Vehicle/Energy) | $11.5 | -41% | 7.5% |

| Sypris Electronics (Defense/High-Reliability) | $17.1 | +6% | 6.9% |

Even though Sypris Electronics had modest top-line growth, its margin pressure to 6.9% suggests execution challenges, though the underlying order book remains strong.

The overall mitigation strategy for Sypris Solutions, Inc. against substitution risk is clearly tied to its backlog strength in the less substitutable segments. The 14% backlog increase in electronics and the 59% increase in energy product backlog since year-end 2024 provide a solid foundation against competitive threats in those specialized areas.

- Defense sector: Low threat due to 60+ years of trust.

- Energy products: Low threat due to highly engineered nature.

- Commercial vehicle: Moderate threat, evidenced by 41% revenue drop.

- Electronics backlog: Up 14% since year-end 2024.

Finance: draft Q4 2025 cash flow projection incorporating the Q3 revenue of $28.7 million by Friday.

Sypris Solutions, Inc. (SYPR) - Porter's Five Forces: Threat of new entrants

The threat of new entrants for Sypris Solutions, Inc. is generally low to moderate, heavily dependent on the specific market segment. The barriers to entry are substantial, stemming from regulatory complexity, high capital needs for specialized equipment, and established operational footprints.

Low threat in defense/aerospace due to high regulatory hurdles and the need for significant capital investment.

Entering the defense and aerospace electronics space requires navigating a complex web of regulations. For instance, upcoming updates to DFARS (Defense Federal Acquisition Regulation Supplement) could subject companies with contracts exceeding $5 million to Defense Counterintelligence and Security Agency (DCSA) review for foreign influence risks, even without classified information handling. New entrants must also align with geopolitical priorities, as governments scrutinize supply chains for national security reasons. Sypris Solutions, Inc.'s established reputation as a 'Trusted Source' for programs like the Joint Strike Fighter provides a significant intangible barrier.

Low to moderate threat in industrial components due to high capital requirements for precision manufacturing.

The precision manufacturing sector, which includes Sypris Technologies' industrial components, demands heavy upfront capital. Advanced equipment like CNCs requires huge initial purchase, maintenance, and upgrade costs, which prohibits many smaller enterprises from adopting the necessary technology. The Precision Turned Product Manufacturing market size was valued at $121.05 billion in 2025, indicating a large, established market where incumbents benefit from scale and technological integration. Manufacturers in this space are prioritizing cost containment over expansion unless directly tied to high-growth areas like aerospace or data centers.

New entrants are deterred by the cyclical nature and tariff-related demand weakness in the transportation market.

The Vehicle Components segment faces volatility that deters new entrants unwilling to absorb potential downturns. Sypris Solutions, Inc. experienced a revenue decline in Sypris Technologies, its vehicle components arm, reflecting the anticipated cyclical downturn in the commercial vehicle market. Furthermore, tariff uncertainty has driven demand weakness and inventory adjustments among transportation customers. New entrants would face the immediate risk of navigating these macroeconomic headwinds, which caused Sypris Technologies' Q3 2025 revenue to fall to $11.5 million from $19.5 million year-over-year.

Sypris Solutions' specialized manufacturing facilities in the U.S. and Mexico create a cost/scale barrier.

Sypris Solutions, Inc. operates a footprint across 4 locations in 2 countries, employing approximately 600 people. The presence of facilities in both the U.S. (Louisville, KY) and Toluca, Mexico, allows for strategic cost management, though recent operational shifts have occurred. The conversion of certain Mexico shipments to a value-add only sub-maquiladora model in 2025 shows an established, complex operational structure that new entrants would need time and capital to replicate for cost efficiency. The scale of Sypris Solutions, with a Q3 2025 revenue of $28.67 million, provides a base for absorbing fixed costs that smaller startups cannot easily match.

Here is a breakdown of the segment revenue performance as of the third quarter of fiscal year 2025:

| Segment | Q3 2025 Revenue (USD) | Q3 2024 Revenue (USD) | Gross Profit Margin Q3 2025 (%) |

|---|---|---|---|

| Sypris Electronics | $17.1 million | $16.2 million | 6.9% |

| Sypris Technologies | $11.5 million | $19.5 million | 7.5% |

The Electronics segment showed modest growth, while Technologies saw a significant year-over-year decline.

The barriers to entry are further evidenced by the financial scale of Sypris Solutions, Inc., which had a market capitalization of $50.4M as of November 5, 2025.

You should focus your next analysis on how Sypris Solutions, Inc. is managing its working capital given the nine-month operating cash flow used of $(4.613) million for the period ended September 28, 2025.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.