|

Woodside Energy Group Ltd (WDS): BCG Matrix |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Woodside Energy Group Ltd (WDS) Bundle

Woodside Energy Group Ltd stands at a pivotal juncture, navigating a dynamic energy landscape shaped by shifting demands and innovative technologies. Within the context of the Boston Consulting Group (BCG) Matrix, we can categorize its diverse portfolio into Stars, Cash Cows, Dogs, and Question Marks. Each segment reveals critical insights into its performance and strategic positioning. Dive deeper to discover how these classifications impact Woodside's growth trajectory and market potential.

Background of Woodside Energy Group Ltd

Woodside Energy Group Ltd, headquartered in Perth, Australia, is a prominent independent oil and gas company. Founded in 1954, it has grown to become one of the largest producers of hydrocarbons in the Asia-Pacific region. Woodside primarily engages in the exploration, development, production, and marketing of oil and gas, with a focus on liquefied natural gas (LNG).

As of 2023, Woodside's operations span across various assets, including the North West Shelf, Pluto LNG, and Scarborough projects. The company has established itself as a leader in LNG production, which is a critical component of its strategy to respond to the increasing global demand for cleaner energy sources.

In 2022, Woodside reported a significant increase in revenue, reaching approximately $7.4 billion, driven by higher oil and gas prices in the wake of global energy supply disruptions. This financial performance highlights the company's resilience and its ability to capitalize on favorable market conditions.

Woodside is also focused on sustainability and reducing its carbon footprint. It aims to achieve net zero emissions by 2050 and has invested in initiatives to enhance its environmental responsibility, including carbon capture and storage technologies.

The company is publicly traded on the Australian Securities Exchange (ASX) under the ticker symbol WPL. As of late 2023, Woodside's market capitalization was approximately $25 billion, reflecting its strong position in the energy sector.

In terms of strategic partnerships, Woodside has entered various agreements to enhance its portfolio and ensure a stable supply chain. Collaborations with international firms also help Woodside expand its reach into emerging markets and diversify its operational footprint.

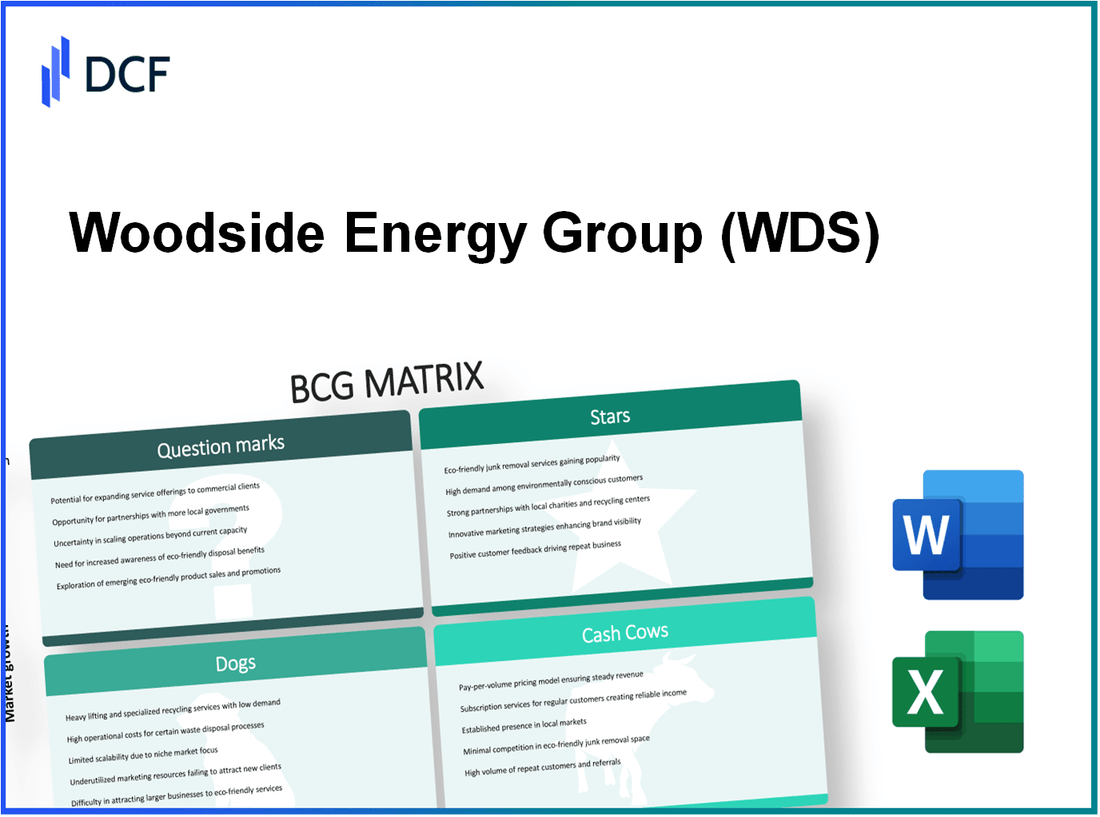

Woodside Energy Group Ltd - BCG Matrix: Stars

Woodside Energy Group Ltd has positioned itself strategically in the energy sector, boasting several business units that qualify as Stars within the BCG Matrix. These units demonstrate both high market share and significant growth potential, particularly in the realms of Liquefied Natural Gas (LNG) and renewable energy.

LNG Projects in High-Demand Regions

Woodside is heavily invested in LNG projects, particularly in Asia-Pacific markets where demand is surging. In 2022, Woodside reported that the company had secured long-term sales agreements totaling approximately $15 billion. In 2023, Woodside's Pluto LNG facility achieved a production capacity of 4.3 million tonnes per annum (MTPA), contributing significantly to its revenue stream.

The demand for LNG is projected to grow at a compound annual growth rate (CAGR) of around 6% through 2027, with Asia leading the charge. Woodside is poised to benefit from this trend due to its strategic positioning in the market.

Renewable Energy Initiatives Aligned with Market Growth

Woodside's commitment to renewable energy is also noteworthy, particularly its investments in hydrogen and solar projects. In 2023, Woodside allocated $800 million towards renewable initiatives, aiming to achieve a production target of 1.5 million tonnes of hydrogen per year by 2030.

The company's hydrogen project at the H2TAS facility is expected to generate significant revenue as global hydrogen demand is forecasted to reach 60 million tonnes by 2030. Woodside’s strategic initiatives align with the global shift towards cleaner energy, positioning the company for sustained growth.

Technology-Driven Exploration and Production

Woodside employs cutting-edge technologies to enhance its exploration and production capabilities. The company's investment in digital technologies has led to a reduction in exploration costs by 20%. In 2023, Woodside’s successful application of machine learning cut the time needed for seismic data analysis by 30%.

Moreover, Woodside's implementation of automated drilling techniques has improved operational efficiency, with drilling costs dropping by 15%. This technological leverage not only strengthens Woodside’s market position but also contributes to its revenue growth, with the production forecast for 2024 set at 100 million barrels of oil equivalent (MMboe).

| Initiative | Investment ($) | Production Capacity | Projected Growth Rate (%) |

|---|---|---|---|

| LNG Projects | 15 billion | 4.3 MTPA | 6 |

| Renewable Energy | 800 million | 1.5 million tonnes of hydrogen/year | N/A |

| Technology Investment | N/A | 100 MMboe (2024 forecast) | 20 |

These elements collectively highlight Woodside's standing as a Star within the BCG Matrix, showcasing its robust market share and strategic investments that drive growth. The company's alignment with industry trends ensures it remains a leader in the energy sector, balancing cash generation with significant reinvestment into its high-potential projects.

Woodside Energy Group Ltd - BCG Matrix: Cash Cows

Woodside Energy Group Ltd's cash cows primarily consist of established oil and gas fields that have demonstrated steady output over the years. These fields are critical to the company's overall financial stability, allowing for consistent revenue generation in a mature market.

Established Oil and Gas Fields with Steady Output

As of 2022, Woodside reported production of approximately 95.8 million barrels of oil equivalent (MMboe). The majority of this output came from long-standing assets such as the North West Shelf and the Pluto gas project. These fields contribute significantly to the company’s cash flow, maintaining a relatively stable production profile.

Long-term LNG Contracts with Key Customers

Woodside has secured long-term contracts for liquefied natural gas (LNG) sales, which ensure predictable revenue streams. As of 2023, the company reported that over 70% of its LNG sales were locked in through long-term agreements, providing a buffer against market volatility. The average selling price for LNG contracts was around $12 per MMBtu in early 2023, reflecting steady demand in the Asia-Pacific region.

| Year | Production (MMboe) | LNG Contracts (%) | Average Selling Price ($/MMBtu) |

|---|---|---|---|

| 2020 | 90.5 | 65 | 8.50 |

| 2021 | 93.2 | 68 | 10.00 |

| 2022 | 95.8 | 72 | 11.00 |

| 2023 | Est. 97.0 | 70 | 12.00 |

Mature Downstream Operations

Woodside's mature downstream operations encompass refining and marketing activities that further enhance its cash cow portfolio. In 2022, the downstream segment generated revenues of approximately $2.5 billion, primarily driven by refining margins and enhanced operational efficiencies. The company reported a gross profit margin of 30% from this segment, indicating strong profitability despite a larger industry trend towards lower growth.

The combination of established fields, long-term contracts, and mature operations positions Woodside effectively within the BCG Matrix's cash cow quadrant. This status enables the company to generate substantial cash flows, which are crucial for sustaining long-term strategic initiatives and shareholder returns.

Woodside Energy Group Ltd - BCG Matrix: Dogs

Within Woodside Energy Group Ltd, certain assets can be categorized as 'Dogs' in the BCG Matrix, indicating their positioning in low growth markets with low market share. This often results in these units neither generating significant profit nor requiring substantial investment, making them prime candidates for divestiture.

Declining Oil Fields with High Operational Costs

Woodside's portfolio includes several mature oil fields that have seen a gradual decrease in production levels. Specifically, the Enfield oil field, which has been operational since 2007, reported a production decline to approximately 5,000 barrels of oil per day as of 2023, down from a peak of 40,000 barrels per day in its early years. The operational costs associated with these aging fields are rising, with estimated production costs around $30 per barrel, impacting overall profitability.

Outdated Petrochemical Assets

The company’s involvement in certain petrochemical ventures, particularly in downstream operations that have not been modernized, has contributed to their status as Dogs. The Karratha Gas Plant, for example, has faced challenges due to aging infrastructure and limited capacity for scalability. Its operating margins have narrowed to around 5%, compared to the industry average of approximately 10% to 15%. This inefficiency has resulted in reduced competitiveness in the market.

Underperforming Energy Services

Woodside’s energy services sector, particularly in the provision of drilling and maintenance services, has also underperformed. Recent quarterly reports indicate that this division has experienced a revenue drop of 25% year-on-year, correlating with a decrease in global demand for offshore drilling services. Operating expenses in this segment have not significantly decreased, leading to an EBITDA margin of only 3%, far below the industry standard of around 8%.

| Asset Type | Current Status | Production/Performance Metrics | Operational Costs |

|---|---|---|---|

| Enfield Oil Field | Declining | 5,000 barrels/day; Peak: 40,000 barrels/day | $30 per barrel |

| Karratha Gas Plant | Outdated | Operating margin: 5%; Industry average: 10-15% | High fixed costs; Limited scalability |

| Energy Services | Underperforming | Revenue drop: 25% YoY; EBITDA margin: 3% | Rising operational expenses |

In summary, Woodside Energy Group Ltd's Dogs are characterized by stagnant assets in a low growth environment, burdened by high operational costs and outdated infrastructure. These factors hinder performance and investment returns, necessitating a reevaluation or divestment strategy to allocate resources more effectively across the portfolio.

Woodside Energy Group Ltd - BCG Matrix: Question Marks

Within the context of Woodside Energy Group Ltd, several segments can be identified as Question Marks due to their high growth potential yet low market share. These focus primarily on emerging renewable technologies and markets that require significant investment but currently show unproven returns.

Emerging Renewable Segments with High Investment Needs

Woodside has been actively investing in the renewable energy sector, particularly in hydrogen production and solar energy. The company announced a potential investment of A$1.1 billion in renewable hydrogen projects through 2025. However, as of 2023, these segments represent less than 5% of Woodside’s total revenue of A$7.5 billion.

For instance, the collaboration with GenZero on the H2Perth project focuses on producing green hydrogen, which is projected to have an output of up to 15,000 tons per annum. Despite this high growth potential, the current market share in the hydrogen space remains negligible.

Unproven Technologies in Carbon Capture and Storage

Woodside has also entered the carbon capture and storage (CCS) sector, with investments exceeding A$500 million aimed at developing technologies that are still in the experimental phase. The company’s CCS initiative aims to capture up to 1.5 million tons of CO2 per year by 2025.

However, the market share for CCS technologies globally is dominated by established energy companies, leaving Woodside as a newcomer with a low market share despite the rapid development of CCS projects. The expected costs of CCS technology implementation can range from A$50 to A$100 per ton of CO2 captured, making it financially challenging without a solid market position.

New Geographical Markets with Uncertain Regulatory Environments

Woodside is exploring opportunities in new geographical markets such as Africa and South America, where regulatory frameworks are still developing. The company plans to allocate A$300 million for exploration and development in these regions in the upcoming fiscal year.

In Africa, specifically, Woodside is looking at opportunities in Mozambique and Senegal, with potential reserves estimated at 30 trillion cubic feet of gas. However, the company faces challenges due to uncertain regulatory environments, which impact its ability to establish a foothold in these emerging markets.

| Segment | Investment (A$ million) | Market Share (%) | Projected Output | Key Challenges |

|---|---|---|---|---|

| Renewable Hydrogen | 1,100 | 5 | 15,000 tons/year | Low market awareness |

| Carbon Capture & Storage | 500 | 2 | 1.5 million tons/year | High implementation costs |

| Africa/South America Market | 300 | 1 | 30 trillion cubic feet (potential) | Uncertain regulations |

While these segments hold promise, they require focused investment and strategic planning to potentially transition into Stars within the BCG Matrix. Consequently, Woodside must navigate the complexities of these markets effectively to convert Question Marks into profitable ventures.

Woodside Energy Group Ltd operates within a dynamic landscape characterized by its strategic positioning across the BCG Matrix. With significant investments in high-demand LNG projects and promising renewable energy initiatives, the company is well-positioned as a Star. Its reliable Cash Cows stem from established oil and gas fields and long-term contracts, providing financial stability. However, the challenges posed by declining assets labeled as Dogs and the uncertainties of emerging market ventures as Question Marks necessitate astute management and innovation to maintain growth and competitive edge in the evolving energy sector.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.