|

WidePoint Corporation (WYY): BCG Matrix [Dec-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

WidePoint Corporation (WYY) Bundle

You're looking for a clear-eyed view of WidePoint Corporation's business lines, and the BCG Matrix is defintely the right tool to map where capital should flow. We need to see which segments are funding growth and which ones need more investment to compete in high-growth markets, using the latest 2025 figures. The core carrier business remains a solid Cash Cow, bringing in $65.0 million revenue over nine months and generating $479,000 in free cash flow, but the real action is in the Stars-like the FedRAMP-authorized ITMS platform that just landed a $40M to $45M deal. Meanwhile, we've got Question Marks like the DaaS offering that drove a $1.9 million net loss while chasing big commercial wins, and Dogs like legacy fees barely hitting $1.3 million in Q3. Let's map out exactly where WidePoint Corporation needs to place its bets for 2026.

Background of WidePoint Corporation (WYY)

You're looking at WidePoint Corporation (WYY) as of late 2025, and the story is one of consistent operational milestones mixed with revenue timing challenges. WidePoint Corporation (WYY) is a technology Managed Solution Provider (MSP) focused on securing the mobile workforce and the broader enterprise environment. They are a federally certified provider of what they call Trusted Mobility Management (TM2) solutions. Their core technology offerings are quite broad, covering Identity & Access Management (IAM), Mobility Managed Services (MMS), Telecom Management, Information Technology as a Service, Cloud Security, and Analytics & Billing as a Service (ABaaS). That's a lot of ground to cover, honestly.

Let's look at the numbers coming out of the third quarter ended September 30, 2025. For that quarter, WidePoint Corporation reported revenues of $36.1 million, which was a modest 4% increase compared to the same quarter last year. Looking at the bigger picture, the revenues for the first nine months of 2025 totaled $108.2 million, also showing an increase year-over-year. The gross margin for the nine-month period stood at 14%, but if you exclude carrier services revenue, that margin improved to 35%.

Profitability metrics showed a positive trend sequentially, even with a net loss reported for the period. The third quarter saw a net loss of $559,000, or a loss of $(0.06) per share. However, the company achieved its 33rd consecutive quarter of positive Adjusted EBITDA, which came in at $344,000 for Q3 2025-that's an 88% sequential jump from Q2 2025. Furthermore, they marked their 8th consecutive quarter of positive free cash flow, hitting $324,000 in Q3 2025, a 260% increase from the prior quarter. As of September 30, 2025, WidePoint Corporation maintained $12.1 million in unrestricted cash and reported a contract backlog of approximately $269 million.

Operationally, WidePoint Corporation has been busy securing significant federal and commercial contracts. They recently secured an estimated $40 million to $45 million SaaS contract to deliver their FedRAMP-authorized ITMS platform to a major telecom carrier. Also, they landed a task order under the Navy Spiral 4 Contract Vehicle for the U.S. Army valued at more than $1.25 million, and a new CWMS 2.0 task order from U.S. Customs & Border Protection valued up to $27.5 million. The company is also positioning itself for the upcoming DHS CWMS 3.0 recompete, which is a $3.0 billion opportunity, with proposals due in mid-December 2025.

Management noted that while the first half of 2025 saw some opportunities shift, these actions have positioned WidePoint Corporation for a strong finish to the second half of 2025, enabling them to capitalize on delayed pipeline opportunities throughout 2026. Still, they revised their full-year 2025 revenue guidance to be slightly below their initial expectations due to those timing issues. Finance: draft 13-week cash view by Friday.

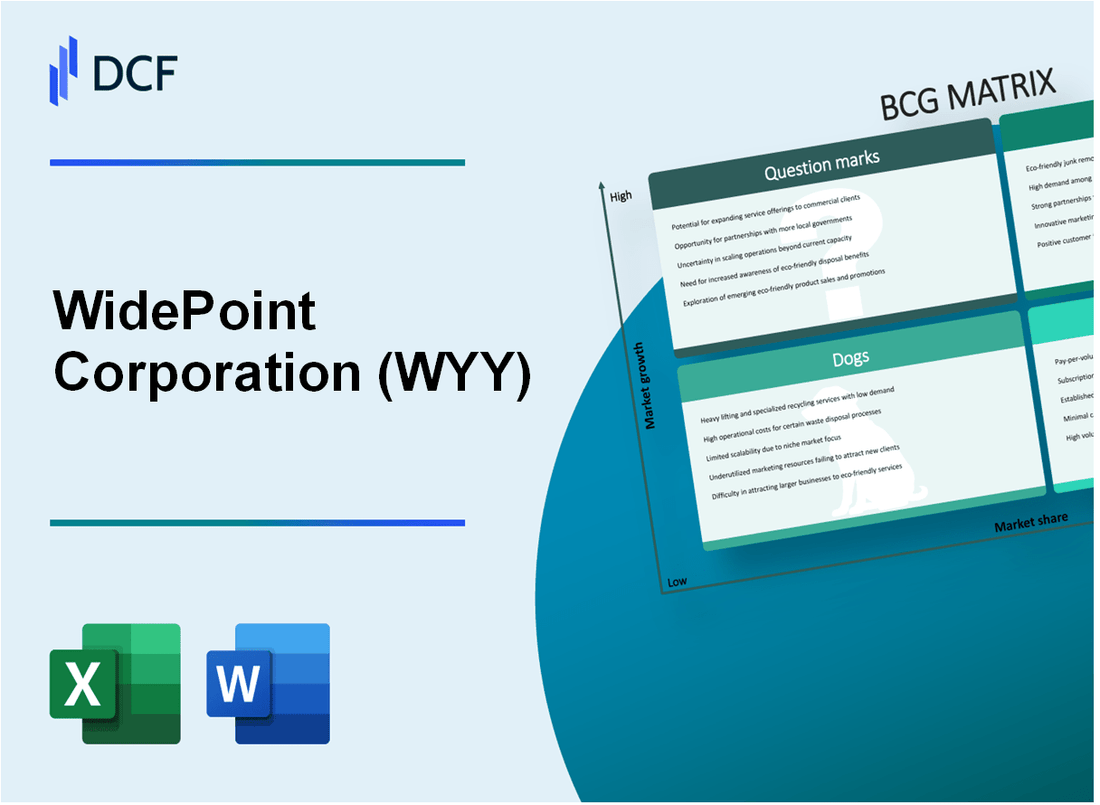

WidePoint Corporation (WYY) - BCG Matrix: Stars

You're looking at the business units that are leading the charge for WidePoint Corporation (WYY) right now, the ones dominating a fast-growing space. These are the Stars in the Boston Consulting Group Matrix, characterized by high market share in markets that are still expanding rapidly.

The Secure Identity & Access Management (IAM) and MobileAnchor Digital Credential Solution are central to this quadrant. WidePoint Corporation is positioned as a subject-matter expert in identity management, credential issuing, and Public Key Infrastructure (PKI), being one of only two companies worldwide certified by the Department of Defense (DoD) for these specific cybersecurity offerings. This suggests a dominant, or near-monopolistic, share within a highly regulated, high-security niche.

The scale of the market these Stars operate in is substantial. The global cybersecurity market size was valued at USD 193.73 billion in 2024 and is projected to grow to USD 218.98 billion in 2025. Specifically for IAM, the segment is projected to grow from $17.7 billion in 2024 to $25.4 billion by 2028. In the US, the government cyber security market is set to grow by USD 4.18 billion from 2025 to 2029, exhibiting a Compound Annual Growth Rate (CAGR) of 6.1%.

A concrete example of this high-growth, high-share success is the recent major contract win. WidePoint Corporation secured an estimated $40 Million to $45 Million SaaS contract to deliver its FedRAMP-Authorized ITMS™ Command Center Platform for a leading global telecom carrier, with revenue recognition expected to start in the second half of 2026. This single contract represents a significant portion of the company's full-year guidance.

Here's a quick look at how these key products relate to WidePoint Corporation's overall financial picture as of late 2025:

| Metric | Value/Range | Date/Period |

| FY 2025 Revenue Guidance | $154 million to $163 million | Full Year 2025 |

| Q3 2025 Revenue | $36.1 million | Period Ended September 30, 2025 |

| Contract Backlog | Approximately $269 million | As of September 30, 2025 |

| ITMS™ Carrier SaaS Contract Value | Estimated $40 Million to $45 Million | Awarded November 2025 |

| Gross Margin (Excluding Carrier Services) | 34% | Q3 2025 |

These Stars consume cash to maintain their leading position in a fast-moving market. The need for continued investment is clear to scale and defend this competitive advantage, especially given the high growth rates in the underlying security segments. The company's strategy involves continued investment to ensure these units can transition into Cash Cows when the market growth inevitably slows.

The operational highlights supporting the Star status include:

- Achieved FedRAMP Authorized Status for its Intelligent Technology Management Systems (ITMS).

- Awarded new Identity & Access Management contract supporting the U.S. Department of Education.

- Awarded new MobileAnchor contract by an agency under the U.S. Department of Energy.

- Secured a $2.5 million Task Order under the Spiral 4 Contract Vehicle with a U.S. Department of Defense combat support agency in Q1 2025.

WidePoint Corporation (WYY) - BCG Matrix: Cash Cows

You're looking at the foundation of WidePoint Corporation's financial stability, the segment that reliably funds the rest of the portfolio. These are the high-share, mature businesses that generate more cash than they need to maintain their position.

The Core Carrier Services Revenue stream is a prime example of this category for WidePoint Corporation. For the first nine months of 2025, this segment brought in $65.0 million. This revenue base is deeply embedded within the federal ecosystem, suggesting a high market share in a necessary, albeit slower-growing, area of telecom management.

This stability is what drives the consistent positive cash flow you see on the bottom line. The company reported a free cash flow of $479,000 for the nine months ended September 30, 2025. Honestly, that positive flow, marking the eighth consecutive quarter of positive free cash flow, is the direct result of milking these established, high-share assets.

The long-standing nature of the Telecom Lifecycle Management (TLM) contracts with large Federal agencies reinforces this Cash Cow status. Think about the DHS Cellular Wireless Managed Services 2.0 (CWMS 2.0) contract; these are multi-year engagements that require minimal new promotional investment but demand consistent service delivery, which is exactly how you manage a Cash Cow.

The overall strength in this area is further evidenced by the substantial contract backlog, which stood at approximately $269 million as of September 30, 2025. The majority of this backlog represents recurring work with long-standing government customers, which translates directly into predictable future revenue.

Here's a quick look at how this core revenue compares to the total picture for the nine-month period:

| Metric | Value (9 Months Ended 9/30/2025) | Strategic Implication |

| Core Carrier Services Revenue | $65.0 million | High market share in a mature segment. |

| Total Revenue | $108.2 million | The base upon which other growth is funded. |

| Free Cash Flow | $479,000 | Consistent cash generation for corporate needs. |

| Contract Backlog | $269 million | Strong revenue visibility for the near term. |

| Gross Margin (Excluding Carrier Services) | 35% | Indicates higher margin potential in the Managed Services component. |

To maintain these Cash Cows, WidePoint Corporation focuses on efficiency rather than aggressive market capture spending. Investments here are targeted at supporting infrastructure to improve cash flow further, not on costly new customer acquisition.

- Maintain productivity on existing large Federal contracts.

- Service the corporate debt with reliable cash inflows.

- Fund the development of Question Marks.

- Support the infrastructure for the DHS CWMS 2.0 base.

- Generate passive gains by 'milking' the established base.

The stability provided by these long-term government relationships is defintely what allows the company to pursue higher-risk, higher-reward opportunities elsewhere in the portfolio. Finance: draft 13-week cash view by Friday.

WidePoint Corporation (WYY) - BCG Matrix: Dogs

The components categorized as Dogs within the WidePoint Corporation portfolio are characterized by their position in markets with low growth prospects or by their inherently low-margin profile, demanding careful management of tied-up resources.

Legacy Billable Services Fees represent a segment seeing contraction, which aligns with the profile of a Dog. For the third quarter of 2025, these fees registered at $1.3 million, a decrease from the $1.7 million recorded in the same period of 2024. This quarterly dip was attributed to a slightly lower count of billable positions during Q3. However, looking at the nine-month period ending September 30, 2025, billable services fees totaled $4.4 million, showing a modest increase of $249,000 over the prior year, reflecting higher billable positions in the first half of 2025.

Commodity reselling and other services fall into the category of lower-margin activities that are not the primary strategic growth drivers for WidePoint Corporation, which is increasingly focused on margin-accretive SaaS contracts.

| Service Category | Q3 2025 Amount | Q3 2024 Amount | 9-Month 2025 Amount | 9-Month 2024 Amount |

| Legacy Billable Services Fees | $1.3 million | $1.7 million | $4.4 million | $4.151 million (Calculated: $4.4M - $0.249M) |

| Reselling and Other Services | $4.3 million | $2.0 million (Calculated: $4.3M - $2.3M) | $10.3 million | $12.2 million |

The financial data for the reselling segment shows that for the nine-month period of 2025, revenue was $10.3 million, down from $12.2 million in the comparable period last year. This year-over-year comparison appears lower because of a change in revenue recognition for SaaS-type reselling agreements, where revenue is now recognized ratably over the contract period instead of at delivery, which front-loaded last year's revenue. The overall gross margin, excluding carrier services revenue, for Q3 2025 was 34%, while the total company gross margin was 15% for the quarter.

These older, less-differentiated offerings, particularly in the commercial market, are contrasted by the company's success in securing large, margin-accretive SaaS contracts, such as the estimated $40 million to $45 million SaaS contract for the FedRAMP-authorized ITMS platform.

The continued existence of these segments necessitates ongoing management oversight and resource allocation, even if they contribute minimally to the desired growth trajectory. The requirements for management are evidenced by the operational focus areas that still require attention:

- Legacy Billable Services Fees saw a slight decrease in Q3 2025 to $1.3 million.

- Reselling and other services revenue for the nine-month period was $10.3 million, compared to $12.2 million the prior year.

- Gross profit percentage from managed services revenue decreased to 34% in Q3 2025 from 38% the previous year, partially due to a shift towards lower-margin reselling.

- Sales and marketing expenses for the nine-month period were $2 million, or 2% of revenues.

General administrative expenses in the third quarter were $4.8 million.

WidePoint Corporation (WYY) - BCG Matrix: Question Marks

You're looking at the areas of WidePoint Corporation (WYY) that are in fast-growing markets but haven't yet captured significant market share. The Device-as-a-Service (DaaS) offering is definitely one of these. This is a key focus for long-term sustainable growth, especially as the DaaS market itself is seeing an estimated 22% CAGR market growth. Right now, the pipeline for DaaS is growing, with more than 90% of the opportunities targeting large commercial, managed services clients, which is a shift toward the broader commercial sector where initial share is low. This is where the high growth potential lies, but it requires heavy investment to secure that share.

These Question Marks consume cash while they scale up to prove their market viability. This investment in infrastructure and sales to capture that commercial market share is a major factor in the company's current financial standing. For the nine months ending September 30, 2025, WidePoint Corporation reported a net loss of $1.9 million. This loss reflects the cash burn required to position these growth areas, like DaaS, for future success. Still, the third quarter showed sequential improvement, with the Q3 2025 net loss narrowing to $559,000.

Here are some key figures related to these high-growth, high-investment areas as of the third quarter of 2025:

| Metric | Value / Period | Context |

| Nine Months 2025 Net Loss | $1.9 million | Overall cash consumption for growth initiatives. |

| Q3 2025 Revenue | $36.1 million | Quarterly top-line performance. |

| DaaS Pipeline Commercial Focus | 90% | Percentage of DaaS opportunities targeting commercial clients. |

| Estimated DaaS Gross Margin Target | 60-70% | Potential profitability once scale is achieved. |

| Contract Backlog (As of 9/30/2025) | $269 million | Total contracted work remaining. |

The IT as a Service (ITaaS) component, particularly through the recently secured Software-as-a-Service (SaaS) contract with a major telecommunications carrier, demonstrates the potential payoff. This contract is estimated to generate $40 million to $45 million in margin-accretive SaaS revenue over its initial 3-year term. This platform will serve an estimated 2 million to 2.5 million devices, validating the strategy to invest in FedRAMP-authorized ITMS for large commercial entities. Securing these large deals is the necessary step to convert these Question Marks into Stars.

Handling these Question Marks requires clear action based on their potential. You need to decide where to commit the capital to gain share quickly or decide to divest if the path to market leadership is too costly or slow. The immediate requirements for these units include:

- Invest heavily to rapidly increase market share.

- Secure large commercial contracts, like the one targeting 2 million to 2.5 million devices.

- Manage the current cash drain, which contributed to the $1.9 million nine-month net loss.

- Focus on achieving the targeted 60-70% gross margins on DaaS to flip the cash flow profile.

Finance: draft the Q4 2025 capital allocation plan prioritizing DaaS pipeline conversion by next Tuesday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.