|

Xylem Inc. (XYL): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Xylem Inc. (XYL) Bundle

You're assessing Xylem Inc. (XYL) to see if its moat is truly deep enough for the long haul, and honestly, the picture is complex. While the company is leaning hard into digital, projecting it to be 50% of 2025 revenue, and it's sitting on a healthy $5 billion backlog, we can't ignore the supply side; the top three suppliers control nearly 59.7% of the market for critical components. To really understand where Xylem Inc. (XYL) stands against rivals like Pentair and Veolia, you need to see how these five competitive forces-from customer loyalty baked into long-term municipal contracts averaging 5.2 years to the threat of emerging substitutes-are shaping its near-term strategy.

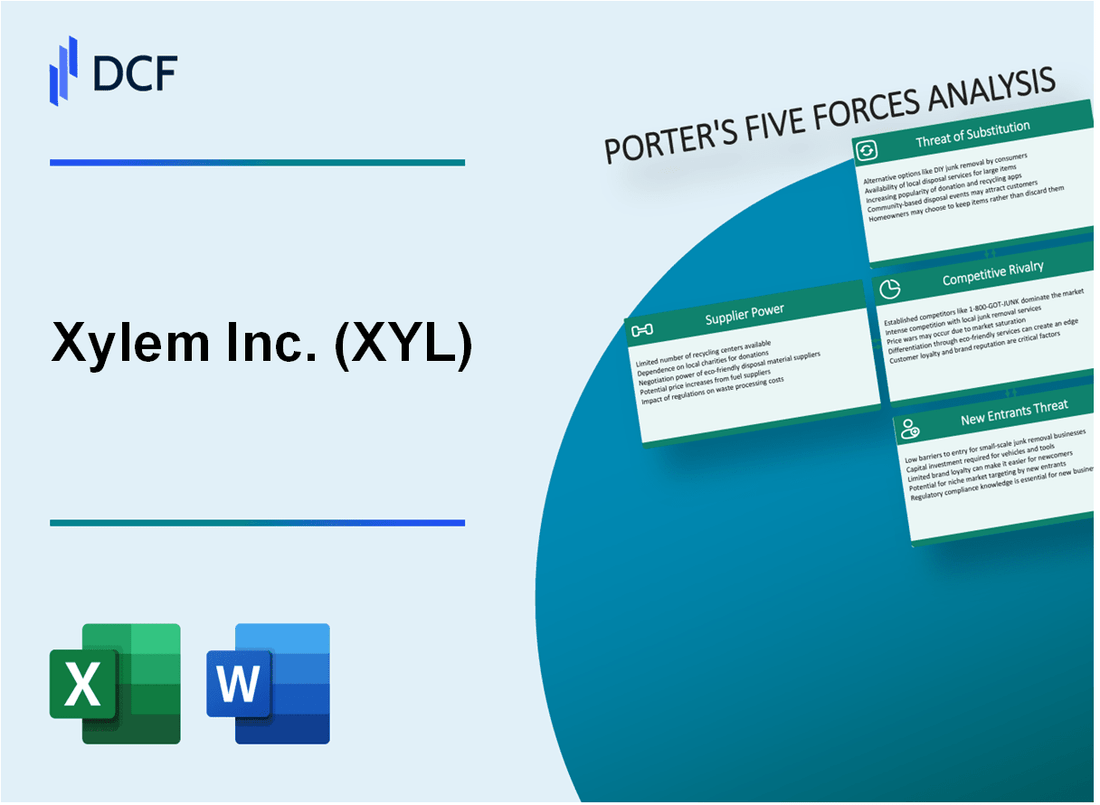

Xylem Inc. (XYL) - Porter's Five Forces: Bargaining power of suppliers

You're analyzing Xylem Inc.'s supplier landscape as of late 2025. The power held by the upstream providers of components and raw materials is a significant factor in Xylem's ability to maintain its projected full-year 2025 revenue guidance of approximately $8.9 to $9.0 billion. This power stems from concentration, high investment in integration, and proprietary technology dependencies.

The structure of the critical component market suggests suppliers hold considerable leverage. We assess the concentration as high, with the top 3 suppliers controlling an estimated 59.7% of the market for certain critical components necessary for Xylem's specialized equipment. This concentration means Xylem Inc. has limited recourse if one of these key partners faces operational issues or seeks to renegotiate terms. Furthermore, the specialized nature of Xylem's business-focusing on complex, specialized water infrastructure-means that many of the necessary inputs are not easily substituted.

The financial commitment required to change suppliers reinforces this dynamic. Critical component switching costs are estimated to be high, reaching up to $2.3 million per transition for certain integrated systems. This figure reflects the deep integration of supplier parts into Xylem's proprietary designs and the associated costs of re-qualifying, re-tooling, and re-certifying new components, which is a major deterrent to switching.

Technology lock-in is another key lever for suppliers. Many suppliers hold proprietary patents for advanced pump and sensor technology that Xylem relies upon for its high-growth segments, like Measurement and Control Solutions, which saw double-digit gains in Q3 2025. While Xylem Inc. itself holds over 8,300 patents and trademarks globally, its dependence on external, patented core technologies limits its negotiating flexibility on pricing and supply terms for those specific items.

We must also factor in external cost pressures. Raw material price volatility can increase supplier cost pass-through. For the broader manufacturing sector in early 2025, manufacturers anticipated raw material prices would rise by 5.5% over the following year. Xylem Inc. has actively managed this, noting that tariff costs (with a net exposure reduced to $160 million) were mitigated through pricing and supplier management, but this ongoing cost pressure is often transferred downstream.

Here is a summary of the key factors influencing supplier bargaining power:

| Supplier Power Factor | Quantifiable Metric/Data Point | Impact on Xylem Inc. |

| Market Concentration | Top 3 suppliers control 59.7% of critical components market. | Reduces Xylem's ability to play suppliers against each other. |

| Switching Costs | Up to $2.3 million per transition for critical components. | Creates high inertia against changing established supply relationships. |

| Proprietary Technology | Suppliers hold patents for advanced pump/sensor technology. | Forces reliance on specific, often higher-priced, specialized inputs. |

| Raw Material Volatility | General manufacturing input cost rise expected at 5.5% (early 2025 estimate). | Increases supplier cost basis, leading to potential cost pass-through to Xylem. |

| Xylem's Business Complexity | Focus on complex, specialized water infrastructure. | Limits the pool of qualified suppliers capable of meeting stringent specifications. |

The supplier power is further illustrated by the high-value transactions in the sector. For instance, IDEX Corporation recently acquired Mott Corporation for a cash consideration of $1 billion, indicating that precision component and proprietary technology businesses command high multiples, which translates to strong pricing power for those suppliers.

To manage this, Xylem Inc. is focusing on operational discipline, which helped drive its Q2 2025 adjusted EBITDA margin to 21.8%. This internal efficiency is crucial for absorbing any unavoidable cost increases from suppliers. You should definitely monitor Xylem's stated goal of attracting more U.S.-based small businesses into its supplier base, as diversification is the primary counter-strategy to supplier concentration.

- Xylem engages with more than 12,000 suppliers globally.

- The company requires suppliers to disclose sustainability information via EcoVadis or equivalent.

- Productivity savings and strong price realization helped offset inflation in Q2 2025.

- The Measurement and Control Solutions segment orders were up 12% in Q2 2025.

Finance: draft 13-week cash view by Friday.

Xylem Inc. (XYL) - Porter's Five Forces: Bargaining power of customers

When we look at Xylem Inc. (XYL) through the lens of customer bargaining power, the picture is one of structural limitations on the buyer side, though not absolute weakness. The power is generally considered moderate, tempered significantly by the nature of the water and wastewater infrastructure business. For instance, power is tempered by long-term municipal contracts averaging 5.2 years. These multi-year commitments lock in revenue streams and reduce the immediate threat of customers shopping around for alternatives on a quarterly basis.

The customer base itself is segmented, which generally keeps any single buyer from exerting overwhelming pressure. Customers are fragmented across utilities, industrial, and commercial segments. To be fair, the utility sector is the bedrock of Xylem Inc.'s business, with large utility customers representing approximately 55% of end markets. However, even within this large segment, the high cost to switch installed systems-think large-scale pumps, controls, and treatment equipment-acts as a major switching cost barrier for these large utility customers. This installed base creates a powerful moat.

The stickiness of Xylem Inc.'s customer relationships is quite remarkable, suggesting that while price negotiation happens, the relationship itself is highly valued. The repeat customer rate is very high at 87%, indicating strong customer loyalty, likely driven by the mission-critical nature of the solutions and the high cost/risk associated with system failure or replacement. Also, the essential nature of water and wastewater treatment solutions means that price sensitivity is low for these critical solutions; customers prioritize uptime and compliance over minor cost savings, especially when dealing with regulatory mandates like the PFAS upgrades requiring systems to be updated by 2029 in many U.S. systems.

We can summarize the customer landscape characteristics here:

- Power is moderated by long-term contract duration.

- Switching costs for installed base are substantial.

- Solutions are deemed essential, lowering price elasticity.

- High customer retention signals deep integration.

Here's a quick look at how the end markets are structured, based on recent reporting:

| End Market | Approximate Revenue Share/Focus | Key Characteristic |

|---|---|---|

| Utility | Approximately 55% of end markets | Focus on water, wastewater, and storm water networks. |

| Industrial | The other primary segment | Requires water/wastewater infrastructure for operations. |

| Building Solutions | Part of the broader exposure | Can see more cyclical demand swings. |

Furthermore, the structure of some agreements suggests long-term commitment potential. For example, certain master agreements can facilitate performance periods extending up to seven (7) years through mutually agreed-upon extensions, which further constrains customer power over the medium term. The focus on recurring revenue, such as maintenance contracts, also helps Xylem Inc. maintain a stable revenue base, which is a direct countermeasure to customer bargaining leverage. Finance: draft the cash flow impact of a 7-year contract vs. a 4-year contract by next Tuesday.

Xylem Inc. (XYL) - Porter\'s Five Forces: Competitive rivalry

You're looking at Xylem Inc. (XYL) in late 2025, and the competitive rivalry force is definitely showing moderate pressure, though Xylem's scale and differentiation are helping manage it. The landscape includes global leaders like Pentair, Veolia, and SUEZ, all vying for market share in essential water infrastructure and treatment. It's not a price war across the board, but you see sharper elbows in specific areas.

Competition ramps up noticeably within the Applied Water segment. This area, which you know is critical for aftermarket and specific equipment sales, represents about 30% of Xylem Inc.'s total business. In contrast, the broader industry growth outlook is healthy, projected at an annual rate of 6.2%, which helps ease the overall price pressure because there's more pie to slice. Still, you can't ignore the established players.

Xylem Inc.'s sheer size provides a competitive moat. The company's 2025 revenue is forecasted at approximately $9.0 billion, which is a significant scale advantage when negotiating with suppliers or bidding on large, multi-year municipal contracts. This scale allows for more robust R&D spending, especially in areas where competitors struggle to match the investment.

Here's a quick look at how the scale stacks up against recent performance data, showing where Xylem Inc. is focusing its strength:

| Metric | Value (FY 2025 Forecast/Latest Data) |

| Full-Year 2025 Revenue Forecast | $9.0 billion |

| Q3 2025 Revenue | $2.27 billion |

| Applied Water Segment Revenue (Q3 2025) | $456 million |

| Water Infrastructure Segment Revenue (Q3 2025) | $656 million |

The key differentiator for Xylem Inc. right now is technology adoption. Differentiation is strong, with digital solutions expected to account for 50% of 2025 revenue. This shift toward smart water management-think real-time analytics and predictive maintenance software-moves the conversation away from pure equipment cost and toward total cost of ownership and operational efficiency, which is where Xylem Inc. excels against rivals focused only on hardware.

The competitive dynamics can be summarized by looking at where the growth and pressure points lie:

- Rivalry intensity is moderate globally.

- Applied Water competition is higher, about 30% of the business.

- Industry growth projection of 6.2% annually eases price pressure.

- Digital revenue target is 50% of 2025 sales.

- Xylem Inc.'s 2025 revenue scale is near $9.0 billion.

- Q3 2025 Adjusted EBITDA margin reached 23.2% (prior year quarter was 21.2%).

To be fair, the competitive intensity in the Applied Water segment, making up roughly 30% of the whole, requires constant vigilance on pricing and service delivery, as customers there are often more sensitive to upfront capital expenditure. Still, the overall market momentum, supported by that 6.2% projected growth, means that Xylem Inc.'s focus on high-margin digital offerings-aiming for 50% of revenue-is the right strategic play to maintain pricing power over competitors who haven't made that same pivot. Finance: draft 13-week cash view by Friday.

Xylem Inc. (XYL) - Porter's Five Forces: Threat of substitutes

You're looking at the competitive landscape for Xylem Inc. (XYL) and need to assess how easily customers can switch to alternatives for their water technology needs. Honestly, the threat of substitutes is real, driven by digital innovation, but Xylem's entrenched installed base provides a significant moat.

Digital water management platforms represent a significant, growing substitute threat. While the prompt suggests a 22.5% growth in 2024 for these platforms, Xylem's own segment data shows the momentum. For instance, Xylem's Measurement & Control Solutions, which heavily includes digital metering, recorded 11% organic growth in the third quarter of 2025. This digital shift means customers can increasingly use real-time data and AI to optimize operations, potentially reducing the need for certain traditional hardware upgrades or services. The broader digital transformation in agriculture alone aims for water use optimization between 20% and 50%.

Here's a quick look at how the growth of these substitute/adjacent technologies compares to the overall market size Xylem operates in:

| Technology Category | Market Value (2025 Est.) | Projected CAGR (Next Period) |

|---|---|---|

| Global Water Management Systems Market | USD 17.74 Billion (2024) to USD 67.34 Billion (2035) | 12.89% (2025-2035) |

| Water Treatment Systems Market (Overall) | USD 45.15 Billion (2025) | 8.15% (2025-2034) |

| Biological Wastewater Treatment Market | N/A | 5.6% (2025-2032) |

| Nanofiltration Membrane Market | USD 1.39 Billion (2024) | 10.2% (2024-2032) |

Emerging alternatives like biological treatment and nanotechnology-based purification are gaining traction, though they target specific treatment niches. The biological wastewater treatment market is expected to reach USD 16.1 billion by 2032. Nanofiltration membranes, a key component in advanced purification, are projected to grow from USD 1.39 billion in 2024 to USD 3.01 billion by 2032.

Still, the high capital investment required for Xylem Inc.'s installed base creates a strong barrier to substitution. Municipalities face massive replacement costs. The federal government estimates a capital improvement need of $472 billion by 2035 just for U.S. drinking water systems, with current spending covering only one-third of that need. This sheer scale of sunk cost and necessary future expenditure locks in many customers to maintaining or incrementally upgrading existing infrastructure.

For customers considering a full switch to unproven substitute technologies, the risks are tangible:

- Regulatory frameworks can be complex and slow deployment.

- Technical validation for novel systems takes time and resources.

- High initial capital outlay is a major constraint for many operators.

- Operational expenses for unproven tertiary treatment systems can be burdensome.

The essential nature of water services fundamentally limits non-technical substitution. Water and Wastewater Treatment Technologies Market size is estimated at USD 65.15 billion in 2025, underscoring that water security is non-negotiable. You can't simply decide not to treat or move water; you must use a solution, which keeps the focus on the incumbent providers like Xylem Inc. unless a substitute offers overwhelming cost or performance advantages.

Xylem Inc. (XYL) - Porter's Five Forces: Threat of new entrants

You're looking at the barriers to entry in the water technology space, and honestly, they are substantial for any newcomer trying to challenge Xylem Inc. The threat of new entrants is decidedly weak, primarily because the industry demands massive upfront investment before you even ship your first high-tech pump or treatment module.

Threat is weak due to extensive capital requirements for infrastructure and R&D. To compete at the level of Xylem Inc., you need serious financial backing. Consider Xylem's commitment to innovation; their Research and Development Expenses for the twelve months ending September 30, 2025, totaled $224M. That's a significant, ongoing spend just to keep pace. Furthermore, Xylem is projecting full-year 2025 revenues around $9.0 billion, which shows the scale incumbents operate at. A new entrant faces the challenge of matching this scale or finding a niche that doesn't require immediate, multi-billion-dollar operational capacity.

High fixed costs are associated with managing high-tech pumps and treatment facilities. This isn't a software startup where you can scale cheaply. We're talking about physical assets, manufacturing plants, and complex service networks. To give you a sense of the underlying capital intensity in the customer base, U.S. municipal capital expenditure (CAPEX) for water and wastewater treatment infrastructure is projected to hit $515.4 billion through 2035. Navigating that environment requires deep pockets and established supply chains, which new firms simply don't possess.

Established brands like Xylem Inc., with a nearly $5 billion backlog, have strong reputational barriers. As of the third quarter of 2025, Xylem Inc. reported maintaining a robust backlog of approximately $5 billion. That figure, which was $5,070 million at the end of 2024, represents secured, long-term work. Customers in this mission-critical sector-where failure means public health risks-prioritize proven reliability over unproven technology. Trust is earned over decades, not quarters.

Regulatory hurdles and long certification cycles for water systems are defintely a factor. The regulatory landscape itself acts as a moat. For instance, evolving regulations around contaminants like PFAS have created massive capital needs for existing utilities; McKinsey analysis suggested new PFAS requirements could lead to a threefold increase in related annual capital spending between 2021 and 2025. A new entrant must not only develop compliant technology but also navigate the lengthy, often multi-year process of getting that technology certified and approved by various municipal and state bodies. Regulatory uncertainty, as noted in 2025 reports, can also cause project delays, which favors incumbents who can absorb those timeline shifts.

Incumbents frequently use M&A to acquire smaller, innovative entrants. Xylem Inc. actively uses its financial strength to neutralize potential threats by acquisition. This strategy buys innovation and eliminates a future competitor. We saw this with the acquisition of a majority stake in Idrica in December 2024, bolstering intelligent solutions, and the purchase of Heusser, a water management solutions provider, also in December 2024. It's a clear signal: if you innovate successfully, Xylem Inc. might just buy your company rather than compete against you.

Here's a quick look at the scale differences that create these barriers:

| Metric | Xylem Inc. (Late 2025 Estimate/Data) | Industry Context/Proxy |

|---|---|---|

| FY 2024 Revenue | $8.6 billion | New entrant must fund operations against this scale. |

| TTM R&D Spend (to Sep 2025) | $224M | Required investment to maintain technological parity. |

| Order Backlog (Q3 2025) | Approx. $5 billion | Represents secured, near-term revenue stability. |

| U.S. Municipal CAPEX Projection (through 2035) | N/A (Customer Spend) | Totaling $515.4 billion-shows the massive, long-term capital base. |

The barriers to entry are high-touch, high-cost, and heavily regulated. It's a tough neighborhood to break into without significant resources or a truly disruptive, non-regulated technology.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.