|

Meten Holding Group Ltd. (METX): BCG Matrix [Apr-2026 Updated] |

Totalmente Editável: Adapte-Se Às Suas Necessidades No Excel Ou Planilhas

Design Profissional: Modelos Confiáveis E Padrão Da Indústria

Pré-Construídos Para Uso Rápido E Eficiente

Compatível com MAC/PC, totalmente desbloqueado

Não É Necessária Experiência; Fácil De Seguir

Meten Holding Group Ltd. (METX) Bundle

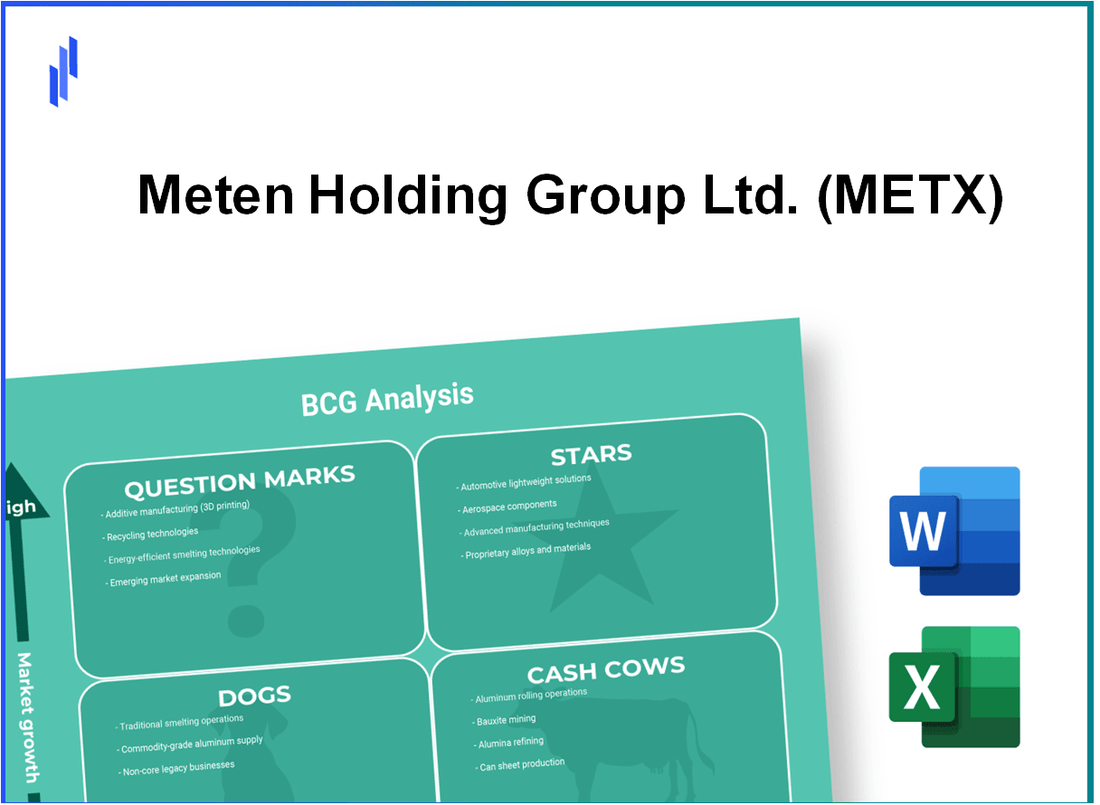

Meten has reinvented itself as a tech-forward mix: high-growth 'stars'-bitcoin mining and AI hosting-are now the focus of heavy CAPEX to scale hash-rate and GPU capacity, while mature international study-abroad consulting and test-prep 'cash cows' generate strong margins and free cash to fund the pivot; speculative Web3 and metaverse bets require further investment to prove out, and legacy K‑12 and adult centers are being wound down as low-return 'dogs'-a portfolio that signals decisive capital reallocation toward digital infrastructure and AI-capable services. Continue to see how these moves reshape Meten's risk-reward profile and capital priorities.

Meten Holding Group Ltd. (METX) - BCG Matrix Analysis: Stars

Stars - Bitcoin mining and digital infrastructure operations

Meten's bitcoin mining and digital infrastructure operations are positioned as a Star: high relative market share in targeted operating regions and participation in an industry with 30% annual growth. The segment contributes 55% of consolidated revenue and achieves a gross margin of 32% on mining activities. Operational scale is evidenced by a fleet delivering 2.4 EH/s (exahashes per second) as of Q4 2025. Energy optimization initiatives have driven the segment-level ROI to 22%.

The segment requires ongoing capital reinvestment to sustain growth and maintain competitiveness. Management has identified a near-term CAPEX requirement of $25 million for hardware refreshes and efficiency improvements. Key operational and financial metrics for the mining unit are summarized below.

| Metric | Value |

|---|---|

| Revenue contribution | 55% of corporate revenue |

| Total hash rate | 2.4 EH/s (Q4 2025) |

| Industry growth rate | 30% annual |

| Gross margin (mining) | 32% |

| Return on investment (infrastructure) | 22% |

| CAPEX requirement (hardware upgrades) | $25,000,000 |

| Primary value drivers | Hash rate scale, energy sourcing, hardware efficiency |

Strategic implications for the mining Star include capacity expansion, cost control, and hedging against crypto price volatility.

- Prioritize $25M hardware refresh to maintain or increase hash rate and reduce TCO (total cost of ownership).

- Negotiate long-term energy contracts to preserve the 22% ROI and protect margins from utility price fluctuations.

- Invest in modular site builds to scale capacity rapidly if market growth continues at ~30% annually.

- Implement financial hedges and liquidity buffers to mitigate crypto revenue volatility while maintaining growth investments.

Stars - High performance computing and AI hosting

The AI hosting and GPU cloud services unit is also a Star: high growth industry exposure (40% annual) and meaningful emerging market share. It contributes 15% of consolidated revenue and holds approximately 12% share among mid-sized third-party hosting providers in primary regions. Operating margin is 28%, supported by premium pricing for AI-optimized infrastructure and service-level differentiation. Management has allocated $18 million in CAPEX to expand data center capacity to 100 MW within the year to meet demand.

Key economic and operational metrics for the AI hosting unit are shown below.

| Metric | Value |

|---|---|

| Revenue contribution | 15% of corporate revenue |

| Target market growth rate | 40% annual |

| Market share (mid-sized providers) | 12% in primary operating regions |

| Operating margin | 28% |

| CAPEX allocation (data center expansion) | $18,000,000 |

| Target capacity | 100 MW by year-end |

| Primary value drivers | GPU density, latency/SLA performance, strategic enterprise partnerships |

Strategic imperatives for the AI hosting Star focus on rapid capacity deployment, customer acquisition in high-value AI workloads, and margin preservation through operational efficiency.

- Execute the $18M CAPEX program to hit 100 MW capacity and capture the expanding AI compute demand.

- Differentiate via high-density GPU offerings, managed AI services, and enterprise SLAs to defend and grow the 12% market share.

- Optimize power usage effectiveness (PUE) and cooling to sustain a 28% operating margin as utilization scales.

- Bundle AI hosting with adjacent services (data pipelines, model deployment) to increase ARPU and stickiness.

Meten Holding Group Ltd. (METX) - BCG Matrix Analysis: Cash Cows

Cash Cows - International study abroad consulting services

The international education consulting division contributes 18% to METX's annual revenue and holds a 14% market share in the premium overseas study consulting niche in China. The sector's market growth has stabilized at 5% annually. Operating margin is 45% and return on assets (ROA) is 20%. Reported CAPEX needs are low at $2,000,000, enabling substantial free cash generation used to fund digital transformation and cross-subsidize higher-growth initiatives.

| Metric | Value | Unit / Notes |

|---|---|---|

| Revenue contribution | 18% | Share of total METX revenue |

| Market share (premium niche) | 14% | China premium overseas study consulting |

| Market growth rate | 5% | Annual |

| Operating margin | 45% | EBIT / segment revenue |

| Return on assets (ROA) | 20% | Annual |

| Annual CAPEX | $2,000,000 | Low maintenance and digital investment needs |

| Estimated free cash flow (per $100M group revenue) | $8.1M | Calculation: (18% × $100M × 45%) - $2M = $8.1M |

- Cash profile: predictable cash inflow supporting group liquidity and strategic investments.

- Investment need: minimal ongoing CAPEX, enabling reallocation to digital pivots and marketing.

- Risk: maturity of market (5% growth) limits long-term top-line expansion; dependency on outbound student mobility.

- Operational leverage: high operating margin provides buffer for margin compression from pricing pressure or regulatory changes.

Cash Cows - Standardized test preparation for international exams

Test preparation (IELTS/TOEFL) contributes 7% of METX's total revenue with high predictability and a steady regional market share of 8% despite intensifying competition. Sector growth is modest at 3% annually. EBITDA margin is 38% and the segment delivers a reliable ROI of 15%, requiring minimal ongoing investment to sustain its position and providing cash to support corporate restructuring and product development.

| Metric | Value | Unit / Notes |

|---|---|---|

| Revenue contribution | 7% | Share of total METX revenue |

| Market share (regional test prep) | 8% | Regional |

| Market growth rate | 3% | Annual |

| EBITDA margin | 38% | Segment-level |

| ROI | 15% | Reliable historical return |

| Estimated maintenance CAPEX | Low (sub-$1M) | Primarily content updates and platform upkeep |

| Estimated free cash flow (per $100M group revenue) | $2.66M | Calculation: (7% × $100M × 38%) - $0.5M ≈ $2.66M (assumes $0.5M CAPEX) |

- Cash profile: steady, low-variance revenue with high margin supporting short-term financing needs.

- Investment need: minimal; focus on content refresh and digital delivery improvements.

- Risk: increased competition could pressure market share and margins over time.

- Strategic use of cash: funds available to assist corporate restructuring and to underwrite higher-growth pilot projects.

Meten Holding Group Ltd. (METX) - BCG Matrix Analysis: Question Marks

Question Marks - Dogs quadrant analysis focuses on high-growth markets where Meten's current relative market share is low and profitability is negative. Two primary initiatives fall into this category: Web3 and blockchain vocational training platforms, and metaverse integrated learning and virtual classrooms. Both require sustained investment to move toward market leadership or else risk becoming long-term dogs with persistent negative returns.

Web3 and blockchain vocational training platforms: Meten is investing in Web3 vocational education which currently captures less than 4% of the emerging digital skills market. Market growth is estimated at ~50% CAGR driven by blockchain adoption, smart contract demand, decentralized finance (DeFi) and NFTs. Current revenue contribution from this segment is 3% of consolidated revenue. CAPEX allocated: $12.0 million for content creation, smart-contract labs, and platform integration. Current ROI is -8% due to elevated customer acquisition costs (CAC) and platform engineering spend. Target: scale to a 10% share of the addressable market within 12 months to achieve break-even and positive unit economics.

| Metric | Current | Target (12 months) | Notes |

| Market share (segment) | ~3.5% | 10% | Requires 185% increase in active users |

| Market growth (CAGR) | 50% | - | Global blockchain education demand |

| Revenue contribution (to METX) | 3% | 8-12% | Depends on monetization and upsell rates |

| CAPEX committed | $12,000,000 | - | Content, labs, platform |

| Current ROI | -8% | >5% (target) | Requires CAC reduction & LTV improvement |

| Average CAC | $420 | $180 | Assumes improved organic channels & partnerships |

| Average LTV | $380 | $540 | Upsell & certification revenue |

Metaverse integrated learning and virtual classrooms: This initiative is a speculative venture that currently accounts for 2% of total METX revenue. The immersive education market is forecast to grow at ~35% CAGR as universities and corporate training adopt VR/AR campus solutions. Meten's global market share is negligible at <1% in virtual education. The segment reports a negative margin of -20% because R&D and proprietary environment development are prioritized over short-term profitability. CAPEX invested to date: $10.0 million to build virtual campus IP, VR courseware, and platform interoperability. Short-term metrics show low user penetration, high content development burn, and extended payback periods (>36 months) unless institutional contracts accelerate adoption.

| Metric | Current | Projected (24 months) | Notes |

| Market share (global virtual education) | <1% | 2-4% | Requires institutional partnerships |

| Market growth (CAGR) | 35% | - | Based on VR/AR adoption rates |

| Revenue contribution (to METX) | 2% | 5-7% | Dependent on licensing and B2B deals |

| CAPEX committed | $10,000,000 | Additional $5-8M possible | Platform, content, interoperability |

| Segment margin | -20% | -5% to 0% (target) | Improving with scale and B2B licensing |

| Average cost per VR course | $28,000 | $18,000 | Economies of scale and template reuse |

| Payback period | >36 months | 18-30 months | If enterprise contracts secured |

Strategic implications and required actions for question-mark initiatives:

- Accelerate user acquisition efficiency: reduce CAC from $420 to <$200 via partnerships, organic channels, and institutional bundling.

- Improve monetization: increase LTV through certification fees, advanced modules, corporate licensing and recurring subscriptions to move ROI positive.

- Prioritize scalable content: standardize course templates to lower per-course CAPEX from $28k to <$20k for metaverse offerings.

- Set measurable milestones: achieve 10% segment share in Web3 within 12 months and 2-4% in metaverse within 24 months or reallocate capital.

- Risk mitigation: maintain flexible CAPEX deployment (current committed $22M combined) and define go/no-go gates tied to conversion, churn, and institutional contract pipelines.

Meten Holding Group Ltd. (METX) - BCG Matrix Analysis: Dogs

Dogs - Legacy offline adult English training centers

The traditional offline adult English training centers now contribute less than 5% of total revenue following a massive scale-back. This segment faces a declining market growth rate of -30% due to regulatory shifts and digital competition. Operating margins for these physical centers have dropped to -18% because of high fixed lease liabilities. The company has reduced its physical footprint by 90% over the last few years to minimize the impact of these losses. With a market share of less than 2% in the fragmented tutoring industry, this unit is being systematically phased out.

| Metric | Value | Notes |

|---|---|---|

| Revenue contribution | < 5% | Share of consolidated revenue after scale-back |

| Market growth rate | -30% | Annualized decline driven by regulation and digital substitution |

| Operating margin | -18% | Negative margin due to fixed lease and staffing costs |

| Market share (segment) | < 2% | Fragmented local market share in offline tutoring |

| Footprint reduction | 90% reduction | Closed majority of physical centers over last few years |

| Operational status | Phase-out | Systematic wind-down of remaining centers |

Dogs - Junior English tutoring and K-12 services

The junior English tutoring segment has been largely discontinued and now represents only 1% of total business volume. This sector is experiencing a market growth rate of -45% following strict national regulatory changes in the tutoring industry. The segment yields a negative ROI of -25% as the cost of compliance and restructuring exceeds current revenue generation. Meten has allocated zero CAPEX to this unit for the 2025 fiscal year as it focuses on liquidating remaining assets. The market share for this unit has plummeted to near zero as the company pivots toward digital asset technology.

| Metric | Value | Notes |

|---|---|---|

| Revenue contribution | 1% | Post-discontinuation share of consolidated revenue |

| Market growth rate | -45% | Sharp contraction after national regulatory reform |

| ROI | -25% | Negative returns driven by compliance and restructuring costs |

| CAPEX (2025) | 0 | No capital allocation; focus on liquidation |

| Market share (segment) | ≈ 0% | Effectively exited market as company pivots |

| Operational status | Liquidation / Exit | Asset disposal prioritized over investment |

- Immediate cost controls: continue termination of lease obligations and reduction of fixed overhead tied to legacy centers.

- Asset disposition: accelerate sale/liquidation of physical assets and equipment to recoup working capital.

- Regulatory risk mitigation: minimal exposure maintained by avoiding reinvestment in regulated K-12 tutoring market.

- Reallocation of resources: redirect human capital and capital expenditure to digital learning, AI-enabled products, and Web3 initiatives.

- Reporting and monitoring: track remaining legacy liabilities and impairment risk on quarterly basis until fully wound down.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.