|

Aster DM Healthcare Limited (ASTERDM.NS): Porter's 5 Forces Analysis |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Aster DM Healthcare Limited (ASTERDM.NS) Bundle

In the dynamic world of healthcare, understanding the competitive landscape is vital for stakeholders. Aster DM Healthcare Limited navigates a complex interplay of factors influencing its market position, from the bargaining power of suppliers and customers to the looming threat of substitutes and new entrants. Discover how Michael Porter’s Five Forces Framework delineates these forces, shaping the strategic decisions that define Aster's operations and growth in an ever-evolving industry.

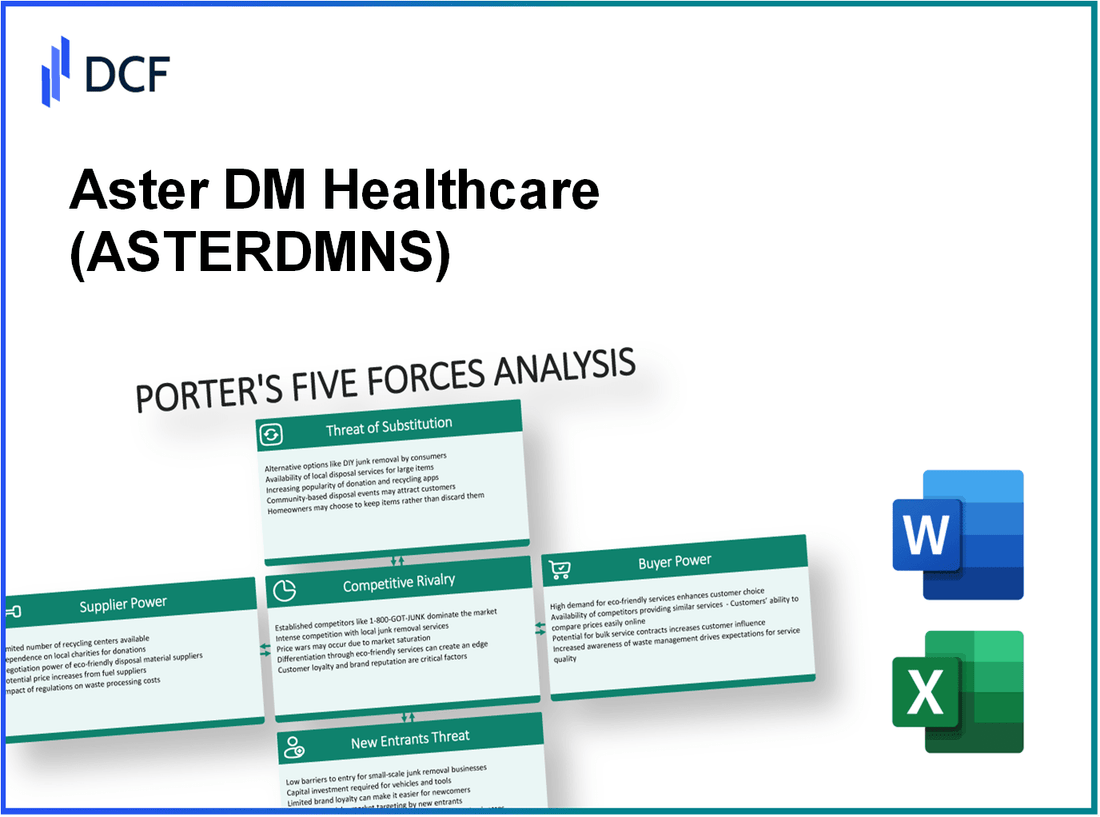

Aster DM Healthcare Limited - Porter's Five Forces: Bargaining power of suppliers

The bargaining power of suppliers within Aster DM Healthcare Limited's operational framework is influenced by several critical factors affecting their pricing strategies and overall negotiations.

Limited supplier alternatives in medical equipment

Aster DM Healthcare relies heavily on specialized medical equipment, where supplier options are often limited. The market is characterized by a few dominant players, with companies like GE Healthcare, Siemens Healthineers, and Philips holding significant market shares. For instance, in 2022, GE Healthcare accounted for approximately 21% of the global medical imaging market.

Dependency on high-quality pharmaceutical suppliers

The healthcare provider is also dependent on high-quality pharmaceutical suppliers. In 2023, Aster DM's revenue from pharmaceuticals constituted around 30% of its total revenue, necessitating strong relationships with suppliers like Novartis and Merck, who provide essential medications. The pharmaceutical industry is experiencing price increases, with reports indicating a 6.5% average annual price increase across the sector.

Potential for volume discounts with bulk purchasing

Aster DM Healthcare benefits from the potential for volume discounts through bulk purchasing strategies. In 2022, the company reported savings of up to 15% on procurement costs through negotiated contracts with suppliers, resulting from increased order volumes. This strategy enhances the company’s overall profitability, allowing it to maintain competitive pricing for patients.

Suppliers might integrate forward in healthcare services

Healthcare suppliers are increasingly looking to integrate forward into healthcare services, thereby increasing their bargaining power. Companies like Cardinal Health have ventured into direct healthcare service offerings, which can limit supplier options for companies like Aster DM Healthcare. This trend emphasizes the need for Aster to strengthen its supplier relationships to mitigate risks associated with supplier consolidation.

Price sensitivity due to critical supply needs

Due to critical supply needs, Aster DM Healthcare faces considerable price sensitivity. A study indicated that hospitals often allocate about 40% of their total expenditures to supplies and pharmaceuticals, demonstrating the financial impact of supplier pricing on operations. Moreover, disruptions in supply chains have heightened awareness of this dependency, particularly during the COVID-19 pandemic, where certain essential supplies surged in price by over 25%.

| Factor | Detail | Relevant Data |

|---|---|---|

| Market Share of Key Suppliers | GE Healthcare | 21% of medical imaging market (2022) |

| Revenue from Pharmaceuticals | Percentage of Aster DM's Total Revenue | 30% (2023) |

| Average Annual Price Increase in Pharmaceuticals | Pharmaceutical Industry | 6.5% |

| Procurement Cost Savings | Volume Discount Achieved | 15% (2022) |

| Healthcare Expenditures on Supplies | Percentage of Hospital Expenditures | 40% |

| Price Surge During COVID-19 | Essential Supplies | 25% |

Aster DM Healthcare Limited - Porter's Five Forces: Bargaining power of customers

The bargaining power of customers in the healthcare industry significantly impacts Aster DM Healthcare Limited's operations and profitability. Understanding the dynamics of customer influence helps assess the competitive landscape in which Aster operates.

Patients have increasing access to health information

Patients today are well-informed, with access to vast amounts of health information through digital platforms. According to a 2023 report by Statista, approximately 77% of Internet users globally have researched health-related topics online. This access empowers patients to make informed choices regarding their healthcare providers, influencing service pricing and quality expectations.

Insurance companies demand cost-effective services

Insurance companies, as significant clients, exert considerable pressure on healthcare providers like Aster DM Healthcare. In 2022, the global health insurance market was valued at $2.09 trillion, with expectations to grow at a CAGR of 6.3% through 2030, according to ResearchAndMarkets.com. Insurers increasingly demand that healthcare services be cost-effective, which forces providers to optimize operational efficiencies to maintain profit margins.

Patient loyalty influenced by quality of care

Quality of care is a crucial factor in patient loyalty. As per the 2023 J.D. Power U.S. Patient Satisfaction Study, patient satisfaction has a direct correlation with loyalty, where 80% of patients are likely to return to a provider that delivers excellent care. Aster DM Healthcare's focus on patient-centric services has led to a steady increase in its Net Promoter Score (NPS), which rose to 52 in 2023, indicating strong patient loyalty.

Low switching costs for patients choosing providers

Patients often face low switching costs when choosing between healthcare providers. A study from Deloitte indicated that 60% of consumers would switch providers primarily due to convenience and perceived service quality. Aster DM Healthcare competes with both local clinics and larger hospital networks, resulting in thin margins and necessitating exceptional service to retain customers.

Large institutional clients may negotiate better rates

Large institutional clients such as government health services and corporate health programs have substantial bargaining power, leading to better negotiated rates. For instance, in 2023, Aster DM Healthcare entered agreements with major institutions, reducing service fees by an average of 15% to secure long-term contracts. This move, while essential for maintaining relationships, can compress profit margins across services.

| Factor | Details | Impact on Aster DM Healthcare |

|---|---|---|

| Access to Health Information | 77% of Internet users research health online | Increases pricing and quality pressures |

| Insurance Market Value | $2.09 trillion in 2022 | Push for cost-effective healthcare services |

| Patient Satisfaction | 80% likelihood of returning with excellent care | Essential for retaining patients |

| Switching Costs | 60% willing to switch for better service | Increases competition among providers |

| Institutional Negotiated Rates | 15% average reduction in fees | Compression of profit margins on services |

These factors illustrate the high bargaining power of customers within the healthcare sector and how they directly affect Aster DM Healthcare’s strategies and financial outcomes.

Aster DM Healthcare Limited - Porter's Five Forces: Competitive rivalry

The competitive landscape for Aster DM Healthcare Limited is characterized by the presence of numerous healthcare providers across its operational regions. As of 2023, the Indian healthcare market is projected to grow from USD 194 billion in 2020 to approximately USD 372 billion by 2025, indicating a robust expansion that attracts various players into the market.

In markets such as the UAE, Aster faces competition from over 500 healthcare entities, including prominent groups like NMC Health and Mediclinic. This saturation compels Aster DM Healthcare to continuously enhance its service offerings to maintain its market share.

Intense competition manifests not only in the number of providers but also in the quality and specialization of services. Aster DM Healthcare emphasizes specialized care in areas such as oncology, cardiology, and orthopedics, competing with established brands like Apollo Hospitals and Fortis Healthcare. These companies are known for their advanced treatments and have invested heavily in cutting-edge technologies, which Aster must match or exceed.

| Healthcare Provider | Specialization Areas | Annual Revenue (2022, INR in Cr) | Number of Hospitals |

|---|---|---|---|

| Aster DM Healthcare | Multi-specialty | 4,322 | 26 |

| Apollo Hospitals | Multi-specialty, Cardiology | 12,947 | 70 |

| Fortis Healthcare | Multi-specialty, Orthopedics | 3,300 | 39 |

| NMC Health | Multi-specialty, Emergency Services | 6,500 | 14 |

Price wars are increasingly common in the healthcare sector. Providers often engage in competitive pricing strategies to attract patients. Aster DM Healthcare has been known to offer promotional rates for diagnostic services, which impacted its bottom line but was essential to retain clientele amidst escalating competition.

Innovation in patient care represents a notable competitive edge. Aster DM has been at the forefront of digital health initiatives, implementing telemedicine services and electronic health records (EHR) which cater to the increasing demand for accessible healthcare. In 2022, Aster reported an increase of 25% in telemedicine consultations compared to the previous year, reflecting the shifting patient behaviors and preferences.

However, high operational costs remain a critical factor influencing competitive behavior in the healthcare industry. Aster DM Healthcare reported operational costs accounting for approximately 75% of its revenue in 2022. This financial pressure drives companies to optimize their operations and seek efficiencies. The average operating margin for hospitals in India hovers around 20%, indicating a competitive environment where cost management can significantly impact profitability.

Aster DM Healthcare Limited - Porter's Five Forces: Threat of substitutes

The threat of substitutes in the healthcare sector is significant and has been growing due to various factors affecting consumer choices.

Alternative medicine gaining popularity

Alternative medicine has seen a rise in acceptance, with the global complementary and alternative medicine market valued at approximately USD 82.2 billion in 2021 and projected to grow at a compound annual growth rate (CAGR) of 19.8%, reaching USD 177.8 billion by 2028.

Telemedicine services offering convenience

Telemedicine has gained traction, especially post-COVID-19, with the telehealth market expected to reach USD 636.38 billion by 2028, growing at a CAGR of 37.7% from 2021. In 2022, about 37% of patients reported having used telehealth services, a significant rise from 11% in 2019.

Public healthcare systems as a low-cost option

Public healthcare systems often serve as a viable alternative, especially in regions where Aster DM Healthcare operates. For instance, the Indian public healthcare sector received a budget allocation of USD 10.7 billion for healthcare in 2021, allowing for extensive coverage and accessibility.

Wellness and preventive care programs

There is a growing trend towards wellness and preventive care, with the global wellness market valued at USD 4.4 trillion in 2021. Preventive care services, such as screenings and health assessments, are increasingly being offered through employer-sponsored health programs.

Health-tech wearables providing self-monitoring options

The health-tech wearables market reached a value of USD 38.1 billion in 2021 and is expected to grow at a CAGR of 23.2% to surpass USD 100 billion by 2028. Devices such as smartwatches and fitness trackers enable consumers to monitor their health metrics, potentially reducing their reliance on conventional healthcare services.

| Substitute Category | Market Value (2021) | Projected Market Value (2028) | CAGR (%) |

|---|---|---|---|

| Alternative Medicine | USD 82.2 billion | USD 177.8 billion | 19.8% |

| Telemedicine | USD 45.41 billion | USD 636.38 billion | 37.7% |

| Public Healthcare Funding (India) | USD 10.7 billion | N/A | N/A |

| Wellness Market | USD 4.4 trillion | N/A | N/A |

| Health-tech Wearables | USD 38.1 billion | USD 100 billion | 23.2% |

The increasing availability of cost-effective and innovative healthcare solutions channels a competitive force against traditional providers like Aster DM Healthcare. This dynamic environment necessitates ongoing strategic adaptations to maintain market relevance and customer loyalty.

Aster DM Healthcare Limited - Porter's Five Forces: Threat of new entrants

The healthcare sector's landscape presents significant barriers to entry for new competitors, particularly in markets where Aster DM Healthcare operates. These factors can influence the overall threat posed by potential entrants.

High capital requirements for entry

The healthcare industry often requires substantial investment to establish operations. For instance, the average cost to set up a multi-specialty hospital can exceed USD 20 million or more, depending on location and specialization. This includes costs for infrastructure, medical equipment, and initial staffing. Additionally, Aster DM Healthcare reported a capital expenditure of approximately USD 26 million in 2022, highlighting the financial commitment necessary to maintain and expand services.

Strict regulatory environment

The healthcare sector is highly regulated, with numerous compliance requirements that must be met. For example, in India, the National Accreditation Board for Hospitals and Healthcare Providers (NABH) sets rigorous standards for hospitals, affecting licensing and operational procedures. Failure to comply can result in penalties or the revocation of licenses, creating a discouraging environment for new entrants.

Established brand loyalty and reputation challenges

Aster DM Healthcare has built a strong brand presence across the Middle East and India. The company's established reputation is underscored by its network of over 3000 medical professionals and a diverse portfolio of healthcare services. This brand loyalty can be challenging for new entrants to overcome, as patients often prefer well-known and trusted institutions for their medical care.

Need for skilled workforce and medical professionals

The demand for skilled healthcare workers remains high. According to the World Health Organization, there is a projected shortage of 18 million health workers globally by 2030. Aster DM Healthcare's workforce comprises approximately 20,000 healthcare professionals, highlighting the challenges new entrants face in recruiting qualified personnel in a competitive labor market.

Potential for technological disruptors entering market

The increasing reliance on healthcare technology poses both a challenge and an opportunity for entrants. Investment in telemedicine and AI-driven diagnostics is on the rise. The global telemedicine market was valued at approximately USD 55 billion in 2020 and is expected to reach USD 175 billion by 2026, growing at a CAGR of 20%. This growth may attract new entrants with tech-focused solutions, potentially disrupting traditional healthcare models.

| Factor | Details | Impact |

|---|---|---|

| Capital Requirements | USD 20 million+ to establish operations | High barrier for new entrants |

| Regulatory Compliance | Standards set by NABH and other bodies | Discourages market entry |

| Brand Loyalty | Strong presence across Middle East and India; 3000+ professionals | Challenges for new competitors |

| Workforce Demand | Shortage of 18 million health workers by 2030 | Limits recruitment for newcomers |

| Technological Trends | Telemedicine market projected to grow to USD 175 billion by 2026 | Opportunity for tech-focused entrants |

Understanding Aster DM Healthcare Limited through the lens of Porter's Five Forces reveals a complex interplay of market dynamics, from the intense competition among providers to the significant bargaining power held by both suppliers and customers. As the landscape evolves, with emerging alternatives and disruptive technologies, Aster must navigate these forces strategically to maintain its edge in the healthcare sector.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.