|

EMBASSY OFFICE PAR (EMBASSY-RR.NS): BCG Matrix [Dec-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

EMBASSY OFFICE PAR (EMBASSY-RR.NS) Bundle

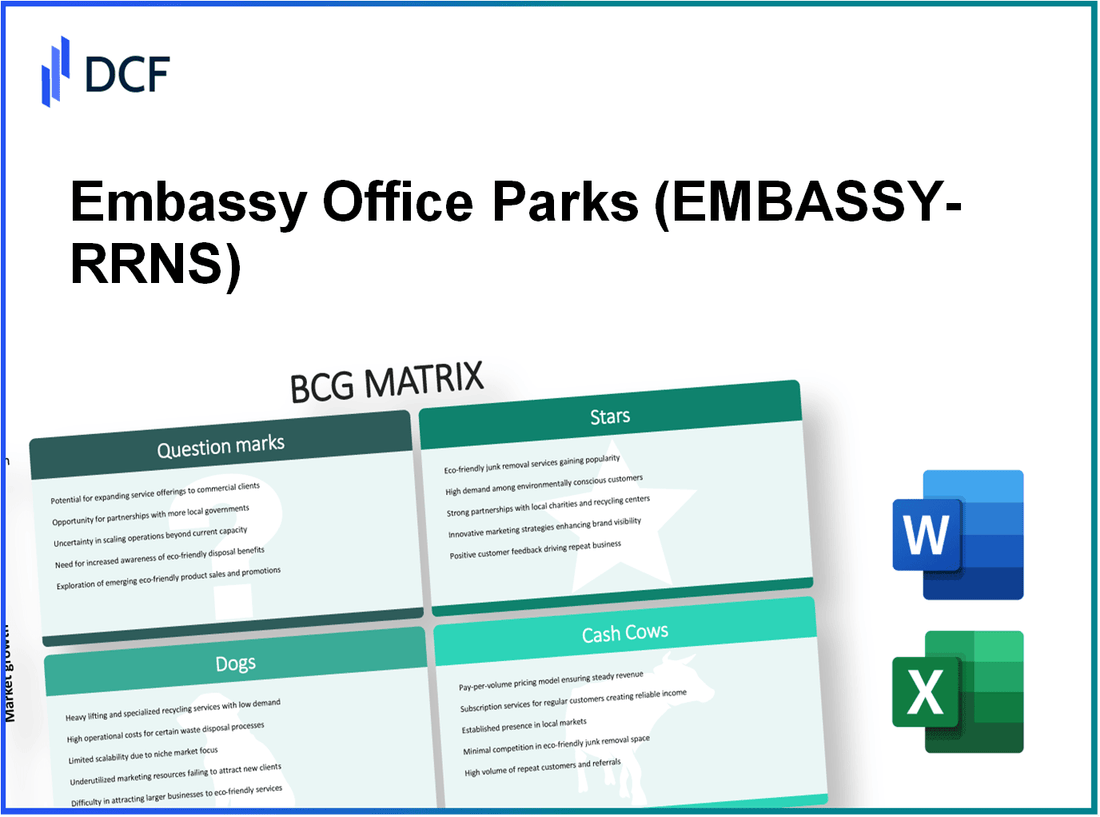

Embassy Office Parks' portfolio balances powerful cash engines-flagship Manyata and high-occupancy joint ventures that fund distributions-with fast-growing stars like Bangalore Grade A developments, TechVillage, Noida clusters and sustainability initiatives that promise outsized rental growth and value capture; management is sensibly recycling cash into an 11-11.5% yield development pipeline while testing question-mark plays (hospitality, solar, retail, Chennai entry) that could add diversification but need careful capital discipline, and pruning legacy dogs-standalone non-core assets, underperforming SEZ blocks and peripheral land-to free capital for higher-return projects.

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - BCG Matrix Analysis: Stars

Stars

Bangalore Grade A Development Pipeline

This segment serves as the high-growth engine for Embassy REIT with an observed 15% annual rental growth rate in the North Bangalore micro-market. The current development pipeline totals 6.1 million sq ft of premium Grade A office space, requiring total CAPEX of ₹2,200 crore. These projects command an average rental premium of 20% versus prevailing market rents due to strategic positioning within emerging suburban employment nodes and integrated ecosystem amenities. Expected yield on cost for the pipeline is 11.5%, with projects capturing approximately 35% of new absorption in the city. At the December 2025 valuation, the Bangalore development pipeline contributes ~25% of total portfolio value.

| Metric | Value |

|---|---|

| Development Area | 6.1 million sq ft |

| CAPEX Required | ₹2,200 crore |

| Annual Rental Growth (North Bangalore) | 15% |

| Rental Premium vs Market | 20% |

| Yield on Cost | 11.5% |

| Share of New Absorption | 35% |

| Contribution to Portfolio Value (Dec 2025) | 25% |

- Priority: Accelerate phased deliveries to lock tenant commitments and realize yield on cost.

- Risk: Construction cost inflation vs targeted CAPEX; mitigate via fixed-price contracts where possible.

- Opportunities: Monetize early via forward-leases or development JV exits to recycle capital.

Embassy TechVillage Growth Assets

Embassy TechVillage (Outer Ring Road) maintains a dominant market share of ~40% within the tech tenant segment in its sub-market. Operational area stands at 9.2 million sq ft with occupancy at 98%. Recent renewals delivered an 18% mark-to-market rental spread, driving a 14% year-on-year increase in Net Operating Income (NOI). The REIT has earmarked ₹850 crore in CAPEX for infrastructure and amenity upgrades to preserve market leadership and support future rent escalation. This cluster is a primary driver behind a projected 7% uplift in annual distributions for FY2026.

| Metric | Value |

|---|---|

| Operational Area | 9.2 million sq ft |

| Occupancy | 98% |

| Tech Tenant Market Share (sub-market) | 40% |

| Mark-to-Market Rental Spread (recent renewals) | 18% |

| YOY NOI Growth | 14% |

| CAPEX Allocated (upgrades) | ₹850 crore |

| Contribution to FY2026 Distribution Growth | Primary driver of +7% |

- Strategic action: Complete planned CAPEX to sustain rental premiums and retain high-quality tenants.

- Financial focus: Leverage high occupancy and NOI growth to support distribution increases and debt servicing.

- Tenant risk: Concentration to tech sector mitigated by long WALE and diversified tenant roster within campus.

Premium Noida Office Clusters

Noida cluster has emerged as a star with a micro-market growth rate of ~12%, propelled by relocation of global capability centers and shared services. These assets account for ~10% of total portfolio revenue and demonstrate an operating margin of ~85%. During the last two quarters, the REIT leased 0.5 million sq ft of incremental space in Noida. Annual capital appreciation in this micro-market stands near 9%, outperforming national commercial real estate benchmarks. Current occupancy levels average 92%, and management targets a 10% market share of the regional Grade A supply.

| Metric | Value |

|---|---|

| Market Growth Rate (Noida) | 12% |

| Portfolio Revenue Contribution | 10% |

| Operating Margin | 85% |

| New Leases (last 2 quarters) | 0.5 million sq ft |

| Annual Capital Appreciation | 9% |

| Occupancy | 92% |

| Target Regional Grade A Market Share | 10% |

- Growth lever: Capture relocation demand from multinational GCCs via tailored leasing solutions.

- Monetization: Consider selective asset recycling to fund higher-yield development elsewhere.

- Margin resilience: High operating margin supports flexibility on tenant incentives to sustain occupancy.

Sustainable Smart Workspace Initiatives

Embassy REIT has invested ₹400 crore in smart building and ESG technologies to capture rising demand for sustainable workspaces, estimated at ~20% market demand for ESG-compliant space. Green-certified assets command a rental premium of ~7% over non-certified peers and have driven a 15% reduction in operating costs across upgraded properties, directly improving portfolio ROI. Current inquiry mix indicates ~82% of new corporate site-selection requests specify high-sustainability features. This initiative is growing approximately 2x the pace of the traditional office market as of late 2025.

| Metric | Value |

|---|---|

| Investment in Smart/ESG Tech | ₹400 crore |

| Market Demand for ESG Spaces | 20% |

| Rental Premium (green-certified vs non-certified) | 7% |

| Operating Cost Reduction | 15% |

| Share of New Corporate Inquiries Seeking ESG Features | 82% |

| Growth Rate vs Traditional Market | ~2x |

- Value creation: ESG tech delivers rental premium, lower opex, and improved tenant retention.

- Capital strategy: Prioritize ESG upgrades in high-vacancy-risk assets to drive differential pricing.

- Market signaling: Leverage certification credentials to accelerate leasing velocity and institutional investor interest.

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - BCG Matrix Analysis: Cash Cows

Cash Cows

Embassy Manyata Business Park Operations

As the flagship cash-generating asset, Embassy Manyata Business Park comprises 12,000,000 sq ft of operational area with a sustained occupancy of 95%. The asset produces a Net Operating Income (NOI) of INR 1,200 crore annually, representing 35% of the REIT's total revenue. Weighted Average Lease Expiry (WALE) stands at 7.2 years, supporting highly predictable cash flows and distribution capacity. Operating margin is 88%, and maintenance CAPEX is low at 2% of revenue (INR 24 crore annually). The asset yields a steady distribution of 6.5% for unitholders and exhibits low rental volatility (standard deviation of monthly collections ~0.8%).

| Metric | Value |

|---|---|

| Operational Area | 12,000,000 sq ft |

| Occupancy | 95% |

| Net Operating Income (Annual) | INR 1,200 crore |

| Share of REIT Revenue | 35% |

| WALE | 7.2 years |

| Operating Margin | 88% |

| Maintenance CAPEX | 2% of revenue (INR 24 crore) |

| Distribution Yield | 6.5% |

| Collection Volatility | ~0.8% std. dev. |

Embassy GolfLinks Joint Venture

The Embassy GolfLinks JV (50% stake) in Central Bangalore spans 2,700,000 sq ft and maintains 99% occupancy. It contributes INR 250 crore to annual cash flow, driven by contractual rental escalations of 10% every three years and negligible tenant churn (annual churn <2%). Operating margin is approximately 90%, with near-zero growth CAPEX required (annual growth CAPEX <0.5% of revenue; maintenance CAPEX ~1.5%). The JV's strong cash conversion enables redeployment of capital to higher-growth developments while preserving predictable distributable income.

| Metric | Value |

|---|---|

| REIT Stake | 50% |

| Operational Area | 2,700,000 sq ft |

| Occupancy | 99% |

| Annual Cash Contribution | INR 250 crore |

| Contractual Escalations | 10% every 3 years |

| Tenant Churn | <2% annually |

| Operating Margin | 90% |

| Growth CAPEX | <0.5% of revenue |

| Maintenance CAPEX | ~1.5% of revenue |

Embassy TechZone Pune Stable Assets

Embassy TechZone Pune comprises 2,200,000 sq ft in Hinjewadi with 88% leasing to blue-chip MNCs, contributing 8% of the portfolio revenue. The segment delivers a stable ROI of 9.5% and shows low rental collection volatility (monthly shortfalls <0.5%). WALE is 5.5 years, supporting medium-term income stability in Pune. Maintenance costs are controlled at 3% of segment revenue. Annualized cash contribution is approximately INR 275 crore (est.), with distributable cash conversion ratio >80%.

| Metric | Value |

|---|---|

| Operational Area | 2,200,000 sq ft |

| Occupancy (Leased to MNCs) | 88% |

| Share of Portfolio Revenue | 8% |

| Return on Investment | 9.5% |

| WALE | 5.5 years |

| Maintenance Costs | 3% of segment revenue |

| Annual Cash Contribution (Est.) | INR 275 crore |

| Cash Conversion Ratio | >80% |

Embassy Oxygen Noida Mature Blocks

Embassy Oxygen Noida's mature blocks account for 6% of total NOI with 91% occupancy across the SEZ office inventory. The segment holds a 15% market share in the local SEZ office space and generates annual revenue of INR 180 crore. Lease structures include standard 15% escalations (timing per lease cycle), providing an inflation hedge. Maintenance and growth CAPEX needs are minimal (maintenance CAPEX ~2.5% of revenue; growth CAPEX negligible), preserving steady distributable cash for the REIT's defensive allocation in the National Capital Region.

| Metric | Value |

|---|---|

| Occupancy | 91% |

| Share of Total NOI | 6% |

| Annual Revenue | INR 180 crore |

| Local SEZ Market Share | 15% |

| Lease Escalations | 15% standard |

| Maintenance CAPEX | ~2.5% of revenue |

| Growth CAPEX | Negligible |

- Total combined operational area of cash cow assets: 19,900,000 sq ft

- Combined annual NOI from cash cows: INR ~1,905 crore (Manyata INR 1,200 cr + GolfLinks INR 250 cr + TechZone Pune INR 275 cr est. + Oxygen INR 180 cr)

- Weighted average occupancy across cash cows: ~93.25%

- Weighted average WALE across cash cows: ~6.4 years (weighted by NOI/estimates)

- Average operating margin across cash cows: ~89%

- Aggregate maintenance CAPEX as % of cash cow revenue: ~2.25%

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - BCG Matrix Analysis: Question Marks

Question Marks - Dogs

Hospitality and Hotel Portfolio Expansion

The hospitality portfolio comprises 1,096 keys across Hilton-branded hotels showing revenue growth of 18% year-on-year. Average Daily Rate (ADR) has risen to INR 12,500. Despite strong top-line growth, contribution to Net Operating Income (NOI) is below 10%. A new 500-key hotel at Embassy TechVillage is under CAPEX deployment to capture recovering corporate travel demand. Current Return on Investment (ROI) for the segment is 8%, below the core office ROI, while estimated market share in the luxury corporate hospitality niche within the relevant micro-markets is 12%.

| Metric | Value |

|---|---|

| Number of Keys | 1,096 |

| Revenue Growth (YoY) | 18% |

| Average Daily Rate (ADR) | INR 12,500 |

| NOI Contribution | <10% |

| New Hotel CAPEX | 500-key development (CAPEX deployed) |

| Segment ROI | 8% |

| Market Share (luxury corporate niche) | 12% |

- High revenue growth but low NOI contribution indicates capital intensity and long payback.

- Key risks: construction cost overruns, slower business travel recovery, margin pressure from operations.

- Opportunities: ADR upside, cross-selling to office tenants, yield management to improve ROI above 8%.

Renewable Energy and Solar Plant

A commissioned 100 MW solar plant supplies green energy to business parks in South India. Initial investment stands at INR 150 crore and the plant represents approximately 5% of total REIT asset value. The internal rate of return (IRR) is estimated at 9%. The primary strategic objective is meeting the portfolio renewable energy target of 25%. The plant currently covers 40% of Bangalore assets' internal power needs. Regulatory uncertainty on cross-subsidy charges poses downside to cost-saving projections.

| Metric | Value |

|---|---|

| Installed Capacity | 100 MW |

| Investment | INR 150 crore |

| Share of Asset Value | 5% |

| Internal Rate of Return (IRR) | 9% |

| Renewable Energy Target | 25% of portfolio |

| Coverage of Bangalore Internal Power | 40% |

| Regulatory Risk | Cross-subsidy charges (uncertain) |

- Strategic value is compliance and resilience rather than immediate high ROI.

- Risks include regulatory cost changes and slower unit-level savings realization.

- Expansion can increase self-sufficiency beyond 40% and improve blended IRR if capex is optimized.

Retail and Ancillary Services

Retail within integrated parks is experiencing a 22% increase in footfalls as office occupancy rises. Retail contributes roughly 3% to total REIT revenue and requires high management intensity, regular tenant improvements, and active leasing. New 50,000 sq ft food & beverage (F&B) hubs are being trialed to boost park attractiveness. Retail margins are approximately 60% of office space margins, driven down by higher common area maintenance (CAM) costs. Market share in organized retail within these micro-markets is under 5%.

| Metric | Value |

|---|---|

| Footfall Growth | 22% |

| Revenue Contribution | 3% |

| F&B Hub Trial Size | 50,000 sq ft |

| Retail Margin vs Office Margin | 60% (relative) |

| Market Share (organized retail) | <5% |

| Management Intensity | High (frequent TI) |

- Retail is high-growth in footfall but low revenue share and margin dilution relative to offices.

- Active asset management and curated F&B/amenity mix can lift spend per visit and rental reversion.

- Scale required to move market share beyond sub-5% and to justify ongoing TI spend.

Chennai Market Entry Strategy

Evaluating acquisition of ~1.5 million sq ft Grade A asset in Chennai to diversify geography. Target market growth is ~11% with REIT currently at 0% market share in Chennai. Initial acquisition CAPEX is estimated at INR 900 crore. Projected ROI for this market entry is ~10%, but the move involves regulatory, leasing, and integration risks in a new jurisdiction. The opportunity is categorized as high-risk, high-reward for fiscal 2026.

| Metric | Value |

|---|---|

| Target Acquisition Size | 1.5 million sq ft |

| Market Growth Rate (Chennai) | 11% |

| Current Market Share (Chennai) | 0% |

| Estimated CAPEX (Acquisition) | INR 900 crore |

| Projected ROI | 10% |

| Risk Profile | High (regulatory & integration) |

| Target Timeline | FY2026 |

- Required capital intensity (INR 900 crore) versus projected 10% ROI yields modest near-term returns compared with core office assets.

- Success hinges on lease-up speeds, tenant mix, local regulatory navigation, and integration efficiencies.

- Alternative strategies include JV structures, phased acquisition, or opportunistic build-to-core to mitigate entry risk.

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - BCG Matrix Analysis: Dogs

Question Marks - Dogs

Legacy Standalone Non Core Assets

These older office assets in secondary micro-markets exhibit a 22% vacancy rate versus a portfolio average of 9%. They contribute 3.8% to total portfolio revenue, with rental growth stagnating at 2% YoY. Renovation CAPEX requirements average INR 18 crore per asset, with estimated upgrade cycles of 24-36 months. Return on Equity for this segment is 5%, well below the portfolio average ROE of 12%. Market share in respective sub-markets is ~3%, while operating margins have compressed to 65% from a prior 75% due to rising maintenance and utilities (+12% YoY).

| Metric | Value |

|---|---|

| Vacancy Rate | 22% |

| Revenue Contribution | 3.8% of portfolio |

| Rental Growth (YoY) | 2% |

| Average Renovation CAPEX | INR 18 crore per asset |

| Return on Equity | 5% |

| Sub-market Share | 3% |

| Operating Margin | 65% |

Embassy One Standalone Office (North Bangalore)

Embassy One records 70% occupancy despite premium positioning; it represents 2% of total leasable area (GLA). Effective rents declined by 5% over the last 12 months; marketing expenses equal 10% of asset-level revenue. Economies of scale are limited due to boutique size; market share in the luxury boutique office segment is <2%. Contribution to Net Operating Income (NOI) has been flat at 1.5% for three years. Estimated annual operating cost per sq ft is INR 220 compared with park average INR 160.

| Metric | Value |

|---|---|

| Occupancy | 70% |

| GLA Contribution | 2% of portfolio |

| Effective Rent Change (YoY) | -5% |

| Marketing Spend (% of Revenue) | 10% |

| NOI Contribution | 1.5% |

| Operating Cost (per sq ft / annum) | INR 220 |

| Market Share (segment) | <2% |

Underperforming SEZ Blocks in Pune

Older SEZ-designated blocks face structural demand erosion following sunset of tax incentives. Vacancy in these blocks is 25% versus 12% for the broader Pune portfolio. Revenue growth for this sub-segment is -3% YoY. Estimated CAPEX to convert SEZ units to non-SEZ use is INR 120 crore, with payback period currently uncertain (modelled payback >8 years under conservative leasing scenarios). These blocks drag portfolio occupancy by ~4 percentage points as of Dec 2025. Tenant churn has increased to 28% annualized from 15% prior to SEZ changes.

| Metric | Value |

|---|---|

| Vacancy (SEZ blocks) | 25% |

| Vacancy (rest of Pune) | 12% |

| Revenue Growth (YoY) | -3% |

| Conversion CAPEX | INR 120 crore |

| Portfolio Occupancy Drag | 4 percentage points |

| Tenant Churn | 28% annualized |

| Estimated Payback (conservative) | >8 years |

Peripheral Land Parcels

The REIT holds multiple small peripheral land parcels not slated for development within five years. These non-income generating assets account for 2% of Net Asset Value (NAV) but produce zero cash flow. Annual holding costs (property tax, security, minimal maintenance) represent a 1% annual drag on cash reserves. Market growth for these micro-locations is ~3% CAGR. Management is reviewing possible liquidation to redeploy capital into development pipeline targeting an 11% stabilized yield.

| Metric | Value |

|---|---|

| NAV Contribution | 2% |

| Cash Flow | Zero |

| Annual Holding Cost Impact | 1% of cash reserves |

| Local Market Growth | 3% CAGR |

| Target Redeployment Yield | 11% |

Key tactical implications for these Dog/Question Mark assets:

- Prioritise divestment of legacy standalone non-core assets with vacancy <- high operating costs and ROE 5%.

- Consider repositioning or sale of Embassy One if marketing spend to revenue ratio cannot be reduced below 6% within 12 months.

- Perform detailed CAPEX vs. sale-price modelling for SEZ blocks; conversion CAPEX INR 120 crore vs expected market sale valuations to determine disposition.

- Accelerate review and potential liquidation of peripheral land parcels to recycle 2% NAV into 11% yield development opportunities.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.