|

EMBASSY OFFICE PAR (EMBASSY-RR.NS): 5 FORCES Analysis [Dec-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

EMBASSY OFFICE PAR (EMBASSY-RR.NS) Bundle

How defensible is EMBASSY OFFICE PAR (EMBASSY‑RR.NS) in today's fierce commercial real‑estate market? This quick Porter's Five Forces snapshot cuts through the headlines-showing how scale, balance‑sheet strength, premium Bengaluru footholds and ESG leadership mute supplier and tenant pressure, while rising sector competition, hybrid work dynamics and land scarcity shape future risks. Read on to see which forces most threaten-or reinforce-Embassy's market dominance.

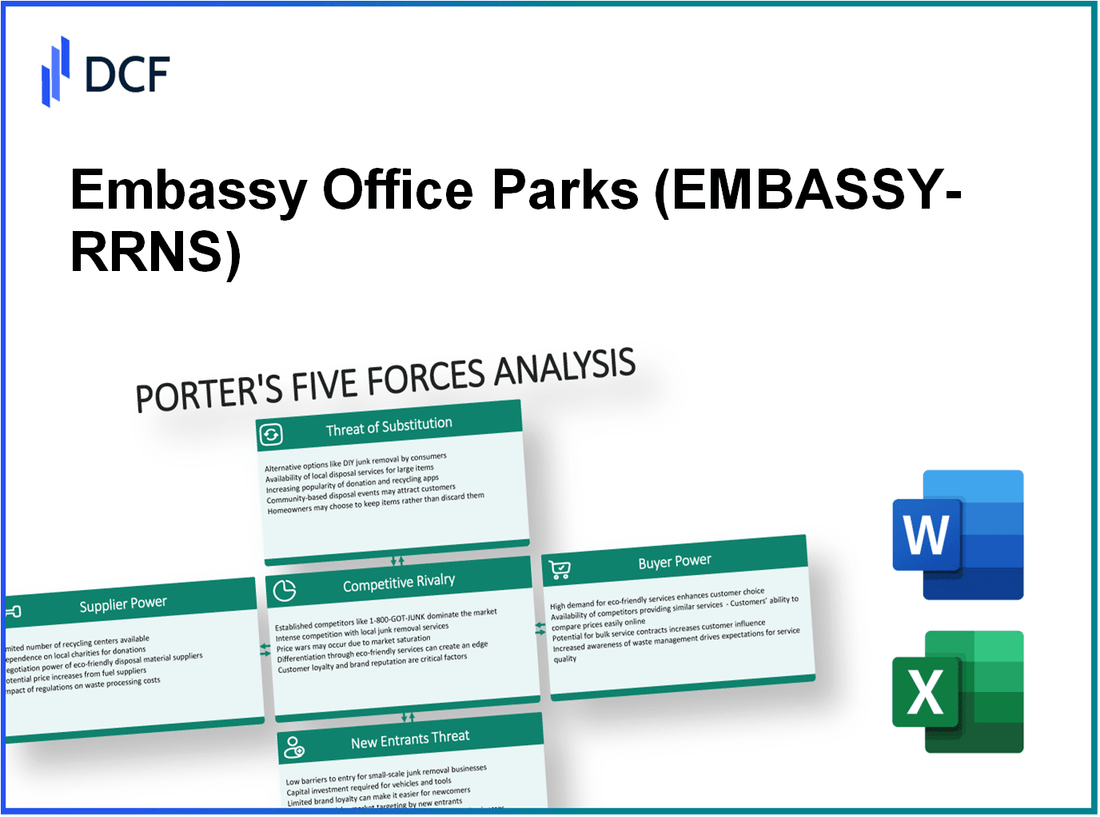

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - Porter's Five Forces: Bargaining power of suppliers

Construction cost inflation limits supplier leverage. Embassy REIT manages a 7.2 million sq ft development pipeline with projected capex of ~₹3,800 crores over the next four years. Despite rising material and labor costs, the REIT's scale and portfolio economics preserve a competitive yield-on-cost for new deliveries - for example, a 0.9 million sq ft Bengaluru project that was 100% pre-leased on completion. The REIT's ability to self-fund via debt markets and maintain a net debt-to-GAV of 33% (Dec 2025) reduces dependency on any single contractor or materials supplier, constraining supplier bargaining power. ESG-compliant Grade-A requirements attract specialized vendors seeking long-term, high-volume contracts, further diluting supplier leverage.

The following table summarizes key metrics that constrain supplier power in construction and vendor relationships:

| Metric | Value | Relevance to Supplier Power |

|---|---|---|

| Development pipeline | 7.2 million sq ft | Scale enables volume procurement and contract standardization |

| Projected investment | ~₹3,800 crores (next 4 years) | Predictable capex reduces ad-hoc supplier pricing leverage |

| Recent large delivery | 0.9 million sq ft, 100% pre-leased (Bengaluru) | Pre-leasing reduces market risk and strengthens negotiating position |

| Net debt-to-GAV | 33% (Dec 2025) | Strong balance sheet limits contractor hold-up risk |

| Raised debt | ₹4,225 crores at blended coupon 7.18% | Access to funding reduces urgency to accept supplier-inflated prices |

| ESG/Grade-A demand | High (portfolio focus) | Creates a supplier ecosystem oriented to long-term partnerships |

Capital providers exert moderate influence on costs. Embassy REIT's funding track record - refinancing ₹6,300 crores at an average 7.98% in FY2025, a landmark 10-year NCD of ₹2,000 crores (late 2025), and ₹400 crores of commercial paper at 6.44% p.a. - demonstrates access to diverse, cost-competitive institutional capital. Total net debt stands at ₹20,183 crores while NOI grew 15% YoY to ₹927 crores in Q2 FY2026, preserving interest coverage and bargaining power with lenders. As a dual AAA-rated entity, the REIT faces low lender-driven pricing pressure, enabling favorable covenant and pricing negotiations with banks and bond investors.

- Refinancing activity: ₹6,300 crores at 7.98% (FY2025)

- 10-year NCD: ₹2,000 crores (India's first by a REIT, late 2025)

- Commercial paper: ₹400 crores at 6.44% p.a.

- Total net debt: ₹20,183 crores

- NOI: ₹927 crores in Q2 FY2026 (15% YoY growth)

Utility and energy suppliers face competitive pressure from the REIT's captive generation and integrated infrastructure. Embassy operates a 100 MW solar park supplying renewable energy to tenants, materially reducing exposure to state-run electricity boards and their price-setting power for a significant portion of portfolio consumption. The captive renewable capacity supports ESG credentials (5-star British Safety Council rating) and acts as a cost hedge against utility inflation. The hospitality business's operational resilience - 12% YoY EBITDA growth and 16% ADR rise - offsets rising service costs, lessening supplier-induced margin pressure.

Key operational/utility metrics:

| Item | Data | Implication |

|---|---|---|

| Solar park capacity | 100 MW | Reduces purchased power volumes and price exposure |

| ESG rating | 5-star (British Safety Council) | Attracts green suppliers and preferential vendor terms |

| Hospitality EBITDA growth | +12% YoY | Improves overall margin resilience versus supplier cost rises |

| Hospitality ADR growth | +16% YoY | Revenue offset to supplier-driven cost increases |

Landlord-sponsor relationships provide strategic supply advantages. Embassy REIT holds a Right of First Offer (ROFO) over the Embassy Sponsor's pipeline, creating a steady, sponsor-aligned supply of institutional-grade assets without open-market competition. In 2025 the REIT evaluated multiple sponsor and third-party acquisitions and acquired the 5.0 million sq ft Embassy Splendid TechZone for an enterprise value of ₹1,269 crores. The sponsor's incentive alignment and predictable pipeline neutralize traditional landowner bargaining power and support a high portfolio occupancy by value (93%), enabling continued strong distributions - record quarterly distributions of ₹617 crores.

- ROFO pipeline: preferential access to sponsor assets

- Recent strategic acquisition: Embassy Splendid TechZone - 5.0 million sq ft; EV ₹1,269 crores

- Portfolio occupancy by value: 93%

- Quarterly distributions: ₹617 crores (record)

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - Porter's Five Forces: Bargaining power of customers

Global Capability Centers (GCCs) and technology firms accounted for ~70% of Embassy REIT's leasing activity as of December 2025; in Q2 FY2026 the REIT leased 1.5 million sq ft across 20 deals, with ~1.0 million sq ft going to marquee global names. Despite large-volume requirements from these customers, bargaining power is constrained by scarcity of Grade-A office space in prime micro-markets (notably Bengaluru), supporting landlord pricing power and resulting in a 38% re-leasing spread on 1.0 million sq ft of new leases. The portfolio WALE of 8.4 years provides long-term revenue visibility and reduces short-term churn risk.

| Metric | Value | Period |

|---|---|---|

| Share of leasing by GCCs & Tech | ~70% | Dec 2025 |

| Leased area (Q2 FY2026) | 1.5 million sq ft (20 deals) | Q2 FY2026 |

| Re-leasing spread (new leases) | +38% | 1.0 million sq ft |

| WALE (by rental income) | 8.4 years | Dec 2025 |

High occupancy levels across the portfolio significantly restrict tenant negotiation leverage. Portfolio occupancy reached 93% by value and 90% by area in late 2025; Mumbai and Chennai recorded 100% and 95% occupancy respectively. High utilization has allowed rent escalations to be implemented, supporting a 13% YoY growth in revenue from operations to ₹1,124 crore in Q2 FY2026. Even with 1.6 million sq ft of renewals in FY2025, Embassy REIT achieved an 11% renewal spread, indicating elevated switching costs and tenant "stickiness" reinforced by over 200,000 employees using on-campus lifestyle and cultural amenities.

- Occupancy (by value): 93% (late 2025)

- Occupancy (by area): 90% (late 2025)

- Mumbai occupancy: 100%; Chennai occupancy: 95%

- Revenue from operations: ₹1,124 crore (Q2 FY2026), +13% YoY

- Renewals in FY2025: 1.6 million sq ft; renewal spread: +11%

- Employees in ecosystem: 200,000+

Portfolio diversification dilutes individual tenant bargaining power. Embassy REIT hosts 272 leading companies, with the top 10 tenants representing a balanced share across sectors; Financial Services comprise 34% and Technology 25% of rental income. The fragmented occupier mix means that loss of a single large tenant would have limited impact on overall NOI; management guidance for FY2026 NOI remains ₹3,589-3,811 crore. In Q1 FY2026, 25 deals totaling 2.0 million sq ft were signed, underscoring diffuse demand across small and mid-tier occupiers as well as marquee firms.

| Occupier / Portfolio Metric | Value |

|---|---|

| Number of occupiers | 272 companies |

| Top sector concentration - Financial Services | 34% of rental income |

| Top sector concentration - Technology | 25% of rental income |

| Deals signed (Q1 FY2026) | 25 deals; 2.0 million sq ft |

| FY2026 NOI guidance | ₹3,589-3,811 crore |

Premium, infrastructure-style positioning attracts price-insensitive corporate clients that prioritize quality, ESG, and integrated ecosystems over lowest-cost options. The REIT's 14 office parks, high ESG compliance and integrated hospitality/lifestyle offerings have driven a 15% YoY growth in Net Operating Income-outpacing the 13% revenue growth-and demonstrate improved operational leverage. Hospitality ADR rose 16%, reflecting willingness to pay for integrated services. With a Gross Asset Value (GAV) of ₹63,980 crore, the assets are viewed as essential infrastructure for global firms' India operations, reducing tenant success at negotiating rent concessions in a tight, high-demand market.

- Office parks: 14 infrastructure-style campuses

- GAV: ₹63,980 crore

- Net Operating Income growth: +15% YoY (period ending Q2 FY2026)

- Hospitality ADR growth: +16% YoY

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - Porter's Five Forces: Competitive rivalry

Consolidation among top-tier REITs intensifies competition. Embassy REIT competes directly with major listed peers such as Mindspace Business Parks REIT and Brookfield India Real Estate Trust in a rapidly maturing market. As of December 2025, the Indian REIT sector's total Gross Asset Value (GAV) reached approximately ₹2.3 lakh crore, with Embassy holding a leadership position by area across Asia. Recent market entrants - Knowledge Realty Trust (listed August 2025) and the IPO filing of Bagmane Prime Office REIT for $445.6 million - broaden options for institutional capital and tenants, increasing competitive choice.

Despite increased supply and choice, Embassy preserved market leadership by delivering 2.5 million square feet (msf) of new development in FY2025 and reporting an all-time high distribution of ₹617 crore in the latest quarter. This level of distribution reflects management's response to competitive pressure to maintain attractive yield profiles and supports retention of large institutional investors.

| Metric | Embassy REIT (Latest) | Peer Avg / Market |

|---|---|---|

| Indian REIT sector GAV (Dec 2025) | ₹2.3 lakh crore | - |

| Embassy new development (FY2025) | 2.5 msf | Industry new supply: ~6-8 msf (FY2025) |

| Latest quarterly distribution | ₹617 crore | Peer median: ₹280-420 crore |

| Total portfolio area | 51.1 msf | Top-tier peers: 20-40 msf |

| FY2025 revenue / NOI growth | +10% / +10% YoY (post 5.0 msf acquisition) | Peer range: +3% to +12% YoY |

| Cost of debt (Embassy) | 7.18% | Peer range: 7.5%-8.5% |

| Total returns (12 months) | >25% | Peer range: 8%-20% |

| NAV per unit (YoY) | ₹445.91 (+7% YoY) | Sector: +2%-6% YoY |

Bengaluru market dominance provides a defensive moat. Bengaluru represents roughly 75% of Embassy REIT's GAV, concentrating the portfolio in India's strongest office market. In Q2 FY2026 Bengaluru led demand, accounting for over 85% of the REIT's 1.5 msf of new leasing. Embassy's Manyata Business Park, with approximately 16 msf of leasable area, remains a primary destination for GCCs and large occupiers, creating localized pricing power in key micro-markets.

- Geo-concentration: 75% of GAV in Bengaluru provides scale and bargaining power with occupiers and vendors.

- Micro-market leadership: Manyata Business Park (16 msf) acts as a first-choice asset for global and domestic large tenants.

- ESG differentiation: 5-star British Safety Council rating strengthens tenant attraction and retention versus peers.

Competitive rivalry is also manifested in the ESG and certification race. Embassy's 5-star British Safety Council rating and portfolio-level sustainability credentials support premium rents and lower vacancy risk versus smaller or newer entrants that lack similar certification coverage.

Aggressive acquisition strategies define the competitive landscape. The REIT sector is in a growth phase; Embassy is actively evaluating multiple third-party and sponsor-led acquisitions to maintain scale advantages. In FY2025 Embassy acquired a 5.0 msf high-quality asset, contributing to 10% YoY increases in both revenue and NOI. Embassy's ability to raise debt at a 7.18% yield-to-maturity provides a cost-of-capital edge when bidding for large, trophy assets.

- FY2025 strategic acquisition: 5.0 msf asset added; incremental revenue and NOI growth: +10% YoY.

- Debt advantage: 7.18% borrowing cost vs. peer average 7.5%-8.5%, enabling more competitive bids.

- Capital markets access: Total returns >25% over 12 months aid fundraising for acquisitions.

Yield-based competition for institutional investors intensified after SEBI's reclassification of REITs as equity instruments effective January 2026. Inclusion in major indices has become a strategic objective, amplifying the need for predictable distribution growth. Embassy is guiding for 10% distribution growth in FY2026, targeting DPU of ₹24.50-₹26.00 to remain attractive to yield-focused investors.

| Yield / Distribution Metrics | Value |

|---|---|

| Guided DPU growth (FY2026) | +10% |

| Target DPU (FY2026) | ₹24.50-₹26.00 |

| Cumulative distributions since 2019 listing | >₹12,000 crore |

| NAV per unit (latest) | ₹445.91 (+7% YoY) |

| Investor appeal | Dual-return profile: capital appreciation + distributions |

Competition for institutional capital is yield-driven: rivals focus on distribution growth and track records. Embassy's cumulative distributions (>₹12,000 crore since 2019), NAV appreciation (+7% YoY to ₹445.91/unit) and strong total returns create higher switching costs for investors and strengthen retention versus newer or smaller REITs and hybrid products entering the market.

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - Porter's Five Forces: Threat of substitutes

Return-to-office mandates diminish the remote work threat. While hybrid work models persist, a significant trend in 2025 shows large IT/ITeS and global firms mandating a return to the office for at least three days per week. This shift supported stronger absorption rates, with Embassy REIT achieving record Q1 FY2026 leasing of 2.0 million sq ft. Research indicates that by late 2025 office attendance stabilized at levels that require firms to expand rather than contract footprints; Embassy's portfolio occupancy rose to 93% by value, demonstrating that 'work from home' is a weakened substitute for physical office space.

The following table summarizes key metrics that illustrate diminishing substitute risk from remote work and hybridization:

| Metric | Value | Period | Implication |

|---|---|---|---|

| Q1 FY2026 leasing | 2.0 million sq ft | Q1 FY2026 | Record absorption; robust demand |

| Portfolio occupancy (by value) | 93% | Late 2025 | High utilization; low substitution |

| Office attendance baseline | ~3 days/week | 2025 trend | Supports need for physical office space |

| Development pipeline | 7.2 million sq ft | FY2025-FY2027 | 42% pre-leased; long-term commitment |

Flex-space operators act as both partners and competitors. Co-working and flexible office providers such as WeWork India and Smartworks have grown their footprints, but a large portion of these operators lease space within Embassy parks, creating a 'co-opetition' dynamic. In FY2025 Global Capability Centers (GCCs) accounted for 60% of annual leasing, and these tenants prefer long-term, customized Grade-A space. Embassy REIT's 8.4-year weighted average lease expiry (WALE) underscores that core tenants retain long-duration commitments rather than substituting with short-term flex leases.

Key facts on flex-space interaction and lease durability:

- Flex operators often operate as tenants within Embassy-owned assets, aligning incentives between provider and landlord.

- FY2025: GCCs = 60% of leasing volume; preference for bespoke Grade-A space.

- WALE = 8.4 years; indicates low propensity for tenant substitution to short-term flex models.

- Flex-space growth supports occupancy and yields when integrated, rather than replacing REIT assets.

Strata-sold offices offer a lower-quality alternative to REIT assets. Individual investors purchasing single floors or units in strata-sold buildings provide supply that appears superficially competitive but lacks scale, professional asset management, integrated ESG credentials, and consistent amenities. Embassy REIT divested 376,000 sq ft of strata-owned blocks at Manyata for ₹5.3 billion to recycle capital into wholly-owned, more efficient assets-an explicit strategy to reduce exposure to fragmented, inferior substitutes.

Financial and performance indicators that favor consolidated REIT ownership over strata models:

| Indicator | Strata-sold outcome | REIT outcome |

|---|---|---|

| Recent strata divestment | 376,000 sq ft sold | Capital recycled into owned assets |

| Divestment proceeds | ₹5.3 billion | Reinvestment to improve asset quality |

| NOI growth | Not applicable (fragmented assets) | 15% YoY rise to ₹927 crore (Q2 FY2026) |

| Tenant requirements | Limited scale, minimal ESG compliance | Scale and ESG compliance demanded by MNCs |

Digital collaboration tools fail to replace physical innovation hubs. Despite AI, VR, and enterprise collaboration platforms maturing, global firms are consolidating into large campuses to accelerate innovation, mentorship, and client engagement. Embassy REIT's CEO stated in late 2025 that the Indian office market is near one billion sq ft, driven by consolidation. The REIT's 7.2 million sq ft development pipeline is 42% pre-leased, showing multi-year commitments to physical space. The hospitality segment's 12% EBITDA growth further signals that face-to-face meetings and corporate travel are rebounding-digital tools act as supplements, not substitutes.

Quantitative indicators that demonstrate digital tools as complements rather than substitutes:

- Development pipeline: 7.2 million sq ft - 42% pre-leased (FY2025).

- Hospitality EBITDA growth: +12% (latest reported period), reflecting revived business travel and meetings.

- Pre-leasing lead times: multi-year commitments indicate confidence in long-term physical occupancy.

- Occupancy and NOI metrics: 93% occupancy by value; NOI ₹927 crore in Q2 FY2026 (+15% YoY).

Net effect on threat of substitutes: materially diminished. Remote work, flex-space, strata assets, and digital collaboration provide alternative models, but empirical leasing, occupancy, WALE, NOI growth, and pre-leasing rates all indicate that Embassy's Grade-A, professionally managed parks remain largely non-substitutable for the needs of large multinational and GCC tenants.

EMBASSY OFFICE PAR (EMBASSY-RR.NS) - Porter's Five Forces: Threat of new entrants

High capital requirements create a formidable entry barrier. Entering the Grade-A office market at Embassy REIT scale requires massive upfront capital: Embassy's reported Gross Asset Value (GAV) of ₹63,980 crore and 51.1 million sq ft under management set the investment quantum for parity. New entrants would need multi-thousand crore equity commitments plus leverage capacity to acquire land, complete developments and fund operating shortfalls until stabilization.

Key financial datapoints that demonstrate incumbent advantage:

- Gross Asset Value: ₹63,980 crore

- Gross Leasable Area: 51.1 million sq ft

- Recent debt raise: ₹4,225 crore at 7.18% coupon

- Solar park capacity (sunk cost): 100 MW

- Hotel keys (sunk cost): 1,614 keys

| Barrier | Embassy Metric | Implication for New Entrants |

|---|---|---|

| Scale of assets | 51.1 million sq ft; GAV ₹63,980 crore | Requires multi-thousand crore capital to match scale |

| Access to low-cost debt | ₹4,225 crore at 7.18% coupon | New entrants face higher borrowing costs absent track record |

| Sunk infrastructure | 100 MW solar; 1,614 hotel keys | Operational synergies and tenant attraction difficult to replicate |

Regulatory complexity and REIT-specific hurdles protect incumbents. Operating a REIT in India requires compliance with SEBI regulations, minimum thresholds for rent-producing assets (80% rule), investor disclosure regimes and distribution norms. Embassy REIT, as an early and large listed REIT in India, benefits from a multi-year compliance history, audited reporting, and established investor relations processes that reduce regulatory execution risk.

- SEBI compliance: multi-year listed REIT reporting track record

- Asset mix requirement: ≥80% in rent-generating assets

- Capital markets access: need for high credit rating to lower borrowing spreads

- ESG and tenant due diligence: established frameworks demanded by global occupiers

| Regulatory/Capital Requirement | Embassy Status | New Entrant Challenge |

|---|---|---|

| Minimum rent asset threshold | Complies with ≥80% rent-producing assets | Must structure portfolio to meet threshold before listing |

| Credit rating requirement | Dual AAA access demonstrated (market access at competitive rates) | New players need time and track record to achieve similar ratings |

| Classification and tax/regulatory shifts | Adapted to SEBI reclassification of REITs as equity instruments | Regulatory changes favor incumbents with established compliance teams |

Limited availability of prime land parcels in key micro-markets increases entry difficulty. Large contiguous land banks in established commercial hubs are scarce; Embassy Manyata Business Park's 122-acre campus and a 7.2 million sq ft development pipeline on owned land exemplify this scarcity. Acquisition costs, land assembly time and entitlement risks make greenfield entry in core micro-markets capital- and time-intensive.

- Embassy Manyata land bank: 122 acres

- Development pipeline on owned land: 7.2 million sq ft

- 2025 delivery: 0.9 million sq ft 100% pre-leased in Bengaluru

| Location | Embassy Asset | New Entrant Barrier |

|---|---|---|

| North Bengaluru | Manyata Business Park - 122 acres | Impossible to assemble comparable contiguous land at scale today |

| Development pipeline | 7.2 million sq ft on controlled land | Allows growth without land acquisition delays |

| Pre-leased delivery | 0.9 million sq ft delivered in 2025, 100% pre-leased | Demonstrates tenant pull and delivery capability |

Strong brand equity and tenant relationships discourage new competition. Embassy REIT hosts 272 blue‑chip occupiers, sustains a 93% occupancy rate and engages a community of 200,000+ employees through its 'Energize' program. Long-term tenancy, stable cash flows and consistent distributions (cumulative distributions > ₹12,000 crore to date) create loyalty and lower churn, making poaching tenants economically unattractive for newcomers.

- Number of occupiers: 272 blue-chip tenants

- Occupancy rate: 93%

- Employee community engaged: >200,000

- Cumulative distributions: >₹12,000 crore

- 2025 total returns: >25% (indicative performance benchmark)

| Brand/Tenant Metric | Embassy Figure | Competitive Implication |

|---|---|---|

| Occupiers | 272 blue‑chip companies | Entrenched tenant relationships reduce churn risk |

| Occupancy | 93% | High utilization limits available large-block space for new entrants |

| Cumulative distributions | >₹12,000 crore | Investor trust and yield track record hard to match |

| 2025 performance | >25% total returns (reported) | Sets high performance benchmark for new funds/developers |

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.