|

SEGRO Plc (SGRO.L): Porter's 5 Forces Analysis |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

SEGRO Plc (SGRO.L) Bundle

In the dynamic world of industrial real estate, understanding the nuances of competition is vital. SEGRO Plc navigates a landscape shaped by the bargaining power of suppliers and customers, intense rivalry, the threat of substitutes, and the looming presence of new entrants. Through Michael Porter’s Five Forces Framework, we’ll delve into how these elements influence SEGRO's strategy and market position, revealing critical insights that every investor and business analyst should grasp. Let's explore the forces at play beneath the surface.

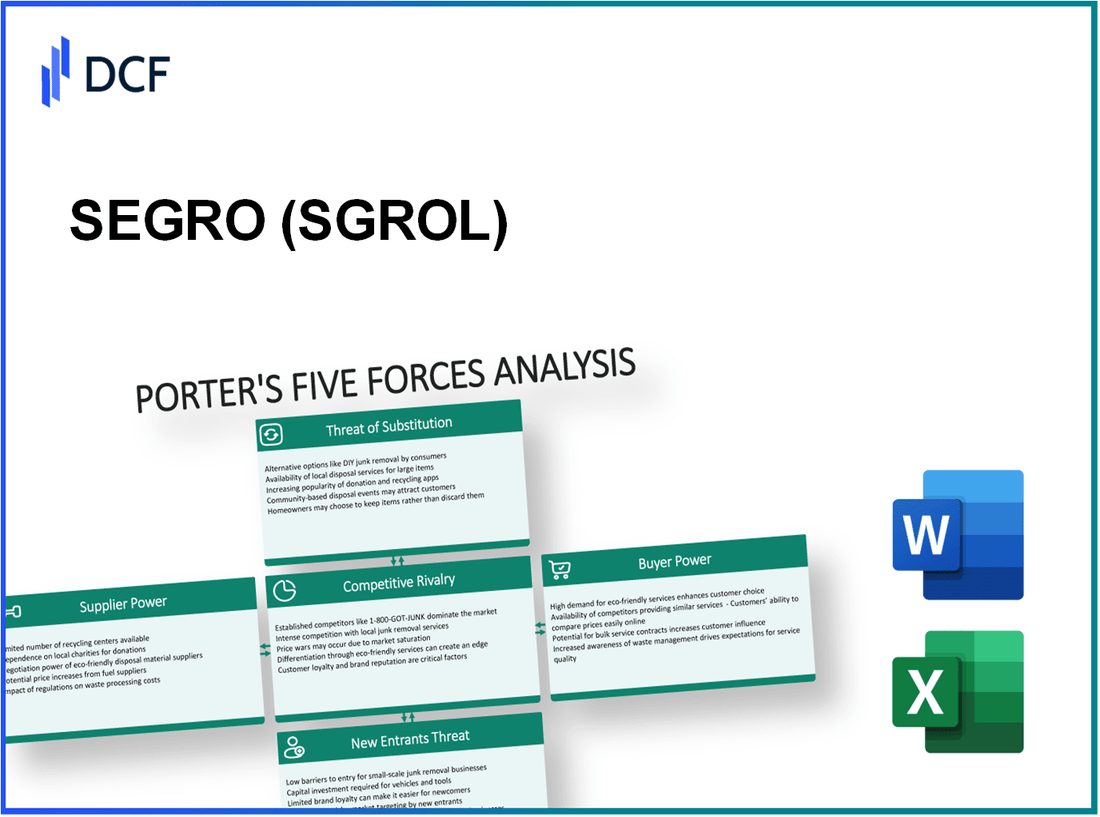

SEGRO Plc - Porter's Five Forces: Bargaining power of suppliers

The bargaining power of suppliers is a crucial factor influencing SEGRO Plc’s operations within the logistics and real estate sectors. With a focus on warehousing and distribution facilities, the dynamics of supplier relationships are pivotal to maintaining cost efficiencies and operational stability.

Limited suppliers for specialized real estate services are a defining feature of SEGRO’s market. The company relies on a small pool of specialized service providers for aspects such as architectural design, engineering services, and technology integration. For instance, SEGRO has engaged notable firms like Arcadis and JLL for consultancy, which can lead to potential price increases under tight supply conditions.

The dependence on local contractors for facility management is significant. SEGRO often collaborates with regional suppliers for maintenance and construction projects. Financial reports from 2022 indicated that facility management costs accounted for approximately 20% of operational expenditures. The reliance on local contractors can heighten supplier power, especially where few competent firms are available.

Moreover, the distribution of power among diverse utility and service providers plays a role in SEGRO’s cost structure. The company sources utilities from multiple vendors, including electricity and water suppliers. In the UK, electricity prices surged by more than 50% year-on-year by Q3 2022, reflecting the volatility and influence of utility providers on overall operating costs.

| Supplier Type | Dependence Level | Price Increase Potential (%) |

|---|---|---|

| Specialized Real Estate Services | High | 15-25 |

| Local Contractors for Facility Management | Medium | 10-20 |

| Utility Providers | Variable | 50 (2022) |

| Construction Materials Suppliers | Medium | 10-30 |

Potential cost increases from material suppliers are another critical aspect. The construction industry has faced significant inflation in recent years, with material costs climbing 25% since 2020. As reported by the Office for National Statistics, the rise in costs for materials like steel and cement greatly affects SEGRO’s project budgets and overall margins.

The influence of key construction firms on project timelines adds another layer of complexity. SEGRO collaborates with several large construction firms, which possess significant leverage in negotiations. Delays caused by these firms can lead to increased holding costs, estimated to be around £200,000 per month per site, depending on the development stage.

In summary, the bargaining power of suppliers for SEGRO Plc presents challenges that can impact operational costs and project execution timelines. The limited availability of specialized suppliers, dependence on regional contractors, and fluctuating material costs contribute to a landscape where supplier negotiation becomes crucial for maintaining profitability and operational efficiency.

SEGRO Plc - Porter's Five Forces: Bargaining power of customers

The bargaining power of customers in the context of SEGRO Plc is characterized by several critical factors that influence the company's operational dynamics and profitability.

High expectations for sustainable and green buildings

SEGRO has committed to advancing its sustainability efforts, which includes achieving a net-zero carbon goal by 2030. As of 2023, approximately 80% of SEGRO’s development pipeline is set to meet a BREEAM rating of at least 'Very Good'. This commitment caters to the increasing demand from tenants for eco-friendly spaces, reflecting a broader market trend where over 70% of industrial tenants prioritize sustainability in their leasing decisions.

Negotiation leverage by large retail and logistics clients

Large clients such as Amazon and DHL significantly influence SEGRO's negotiation landscape. These companies typically command favorable leasing terms due to their substantial space requirements and long-term contracts. For instance, in 2022, SEGRO reported that its largest tenants accounted for approximately 27% of its rental income, highlighting the concentrated revenue risk and the negotiation power held by these major clients.

Availability of alternative spaces in competitive locations

The logistics and warehousing market is competitive, with numerous alternatives available for customers. As of mid-2023, vacancy rates for UK industrial properties hovered around 4.5%, indicating relatively low supply constraints. Tenants can easily explore options in highly sought-after regions, thereby exerting pressure on SEGRO to maintain competitive pricing and amenities.

Customized leasing demands by major clients

Major clients often require tailor-made leasing agreements that include flexible terms and specific design features. In recent negotiations, SEGRO has seen an increase in demand for bespoke solutions, with over 35% of new leases involving customization to meet client needs. Such requirements necessitate proactive engagement from SEGRO to satisfy client expectations and retain business.

Impact of tenant retention strategies on bargaining dynamics

SEGRO employs various tenant retention strategies that significantly impact bargaining. In 2022, the company achieved a tenant retention rate of 92%, largely due to its emphasis on customer satisfaction and service. This high retention rate reduces the need for aggressive cost-cutting measures, allowing SEGRO to maintain a balanced negotiation power with existing tenants.

| Factor | Detail | Statistical Data |

|---|---|---|

| Sustainability Expectations | Percentage of development pipeline meeting BREEAM 'Very Good' | 80% |

| Revenue Concentration | Percentage of rental income from largest tenants | 27% |

| Market Competitiveness | Current UK industrial property vacancy rate | 4.5% |

| Customized Leasing | Percentage of new leases involving customization | 35% |

| Tenant Retention | Percentage of tenant retention rate in 2022 | 92% |

SEGRO Plc - Porter's Five Forces: Competitive rivalry

SEGRO Plc operates in a highly competitive arena within the logistics and industrial real estate sectors. The company faces intense competition from various developers, including but not limited to Prologis, Goodman Group, and Duke Realty. As of the end of 2022, SEGRO reported a market capitalization of approximately £10 billion, emphasizing its significant size in the industry.

In terms of market positioning, SEGRO strategically invests in prime locations. For instance, its properties are located in areas with high demand, such as London and the South East of England, where vacancy rates for logistics properties hovered around 3.6% in 2022, significantly below the national average of 5.8%.

Technological advancements also play a critical role in competitive differentiation. SEGRO has embraced automation, with over 25% of its portfolio featuring smart technology solutions. This allows for enhanced operational efficiencies and sustainability, which are increasingly important to tenants. In 2021, SEGRO invested £54 million in technology to upgrade its properties, underscoring its commitment to innovation.

The rivalry within the logistics and industrial sectors is further amplified by economic conditions. The demand for warehouse space surged during the COVID-19 pandemic, with e-commerce growth leading to an approximate 20% increase in demand for logistics properties. This surge has attracted new entrants into the market, intensifying competition.

Market dynamics show frequent entries and exits that impact the competition's intensity. In 2022 alone, new market entrants included 6 significant logistics firms entering the UK market, while 4 smaller players exited due to financial instability. This fluidity creates a continually shifting competitive landscape, raising the stakes for existing developers like SEGRO.

| Company | Market Capitalization (£ Billion) | Vacancy Rate (%) | Technology Investment (£ Million) |

|---|---|---|---|

| SEGRO Plc | 10 | 3.6 | 54 |

| Prologis | 30 | 4.1 | 100 |

| Goodman Group | 25 | 4.3 | 80 |

| Duke Realty | 20 | 5.0 | 70 |

SEGRO Plc - Porter's Five Forces: Threat of substitutes

The threat of substitutes for SEGRO Plc within the real estate market reflects several evolving trends shaped by technological advancements and changing consumer behaviors.

Shift towards e-commerce reducing traditional retail space needs

The surge in e-commerce has significantly impacted demand for traditional retail spaces. In the UK, online sales accounted for 27.6% of total retail sales as of 2023, up from 19.2% in 2019. This shift has led to an increased demand for logistics and distribution centers, with SEGRO benefitting by focusing on warehouse properties rather than traditional retail spaces.

Potential for alternative fulfillment solutions like urban warehousing

Urban warehousing is gaining traction as companies seek to reduce last-mile delivery times. Research indicates that urban logistics spaces are projected to grow by 10% annually, with urban warehouses becoming a preferred solution for many e-commerce businesses, including major retailers like Amazon, which leased approximately 1 million square feet of warehouse space in urban settings in 2022.

Increasing flexibility in remote working affecting office space demand

The rise of remote working has decreased the demand for traditional office spaces. A survey conducted in 2023 found that 58% of companies plan to adopt a hybrid work model permanently, leading to a projected decline in office occupancy rates, which could impact SEGRO’s investments in office properties.

Innovations in storage and distribution models

Innovative storage solutions such as micro-fulfillment centers are on the rise, allowing retailers to store products closer to consumers, thereby reducing reliance on larger warehouse spaces. In 2023, the market for micro-fulfillment centers is expected to grow by 30% year-over-year, signaling a shift in how goods are stored and distributed.

Emerging logistic technologies minimizing traditional space utilization

With advancements in logistics technologies such as automation and AI-driven inventory management, businesses are optimizing their space needs. In 2022, companies implementing AI in logistics reported a 15%+ reduction in required warehouse space due to improved inventory efficiency and faster fulfillment capabilities.

| Factor | Impact | Statistical Data |

|---|---|---|

| E-commerce Growth | Reduces demand for retail space | 27.6% of total sales in 2023 |

| Urban Warehousing | Increases demand for logistics spaces | 10% annual growth |

| Remote Work Flexibility | Reduces demand for office spaces | 58% companies adopting hybrid models |

| Micro-fulfillment Centers | Shifts storage models | 30% year-over-year growth in 2023 |

| Logistics Technology | Minimizes need for traditional space | 15%+ space reduction with AI |

SEGRO Plc - Porter's Five Forces: Threat of new entrants

The industrial real estate sector presents substantial challenges for new entrants, characterized by high capital requirements. For instance, the average cost of developing industrial warehouses in the UK can range from £80 to £200 per square foot, depending on location and specifications. This financial barrier makes it difficult for new players to secure necessary funding and compete effectively with established firms like SEGRO.

Regulatory and zoning restrictions further complicate the landscape for potential entrants. For example, securing planning permissions can take several years and involve complex local government processes. In the UK, the average timeframe for obtaining planning consent for industrial developments can exceed 16 months, which delays market entry and increases costs.

Moreover, incumbents benefit significantly from established relationships with key clients. SEGRO, for example, has longstanding contracts with major firms across the logistics and manufacturing sectors, including Amazon and DHL. The strength of these relationships provides a competitive edge that new entrants may find difficult to replicate.

While the industrial real estate market is competitive, there exists potential for new entrants to capitalize on niche markets. For instance, the surge in e-commerce has created opportunities for specialized logistics spaces tailored to last-mile delivery. However, these niches still require significant investment and expertise to penetrate.

Economies of scale further amplify the advantages of established firms. SEGRO, with a property portfolio valued at approximately £13.4 billion as of 2023, can leverage its size to reduce costs per unit of space. This operational efficiency allows it to offer competitive lease rates, making market entry for newcomers even more challenging.

| Factor | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Cost of developing industrial warehouses ranging from £80 to £200 per square foot. | High |

| Regulatory Barriers | Average planning consent timeframe exceeds 16 months. | High |

| Client Relationships | Long-term contracts with major clients like Amazon and DHL. | High |

| Niche Market Opportunities | Potential in e-commerce logistics; significant investment required. | Moderate |

| Economies of Scale | SEGRO's property portfolio valued at £13.4 billion. | Very High |

The dynamics of SEGRO Plc's business environment, shaped by Porter's Five Forces, underscore the complex interplay between supplier power, customer expectations, and competitive rivalry, all while navigating the evolving landscape of substitutes and new entrants. Understanding these forces is essential for strategic positioning and sustaining growth in the fast-paced industrial real estate sector.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.