|

Synlogic, Inc. (SYBX): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Synlogic, Inc. (SYBX) Bundle

You're looking at a company like Synlogic, Inc. right now, and the picture is sharp: they are deep in the high-stakes world of Live Biotherapeutics, with their lead asset for PKU heading into a critical Phase 3 readout in H1 2025. Honestly, this market is a battlefield; we see intense rivalry from established treatments and strong leverage from specialized CDMO suppliers, which is a real near-term cash flow concern given their runway was pegged into H1 2025. But, the barriers to entry are sky-high due to the novel science and regulatory hurdles, which is a big plus for long-term moats, even as payers hold significant power over pricing for this novel therapy. You need to see the full breakdown of these five forces to map your next move, so dig into the details below.

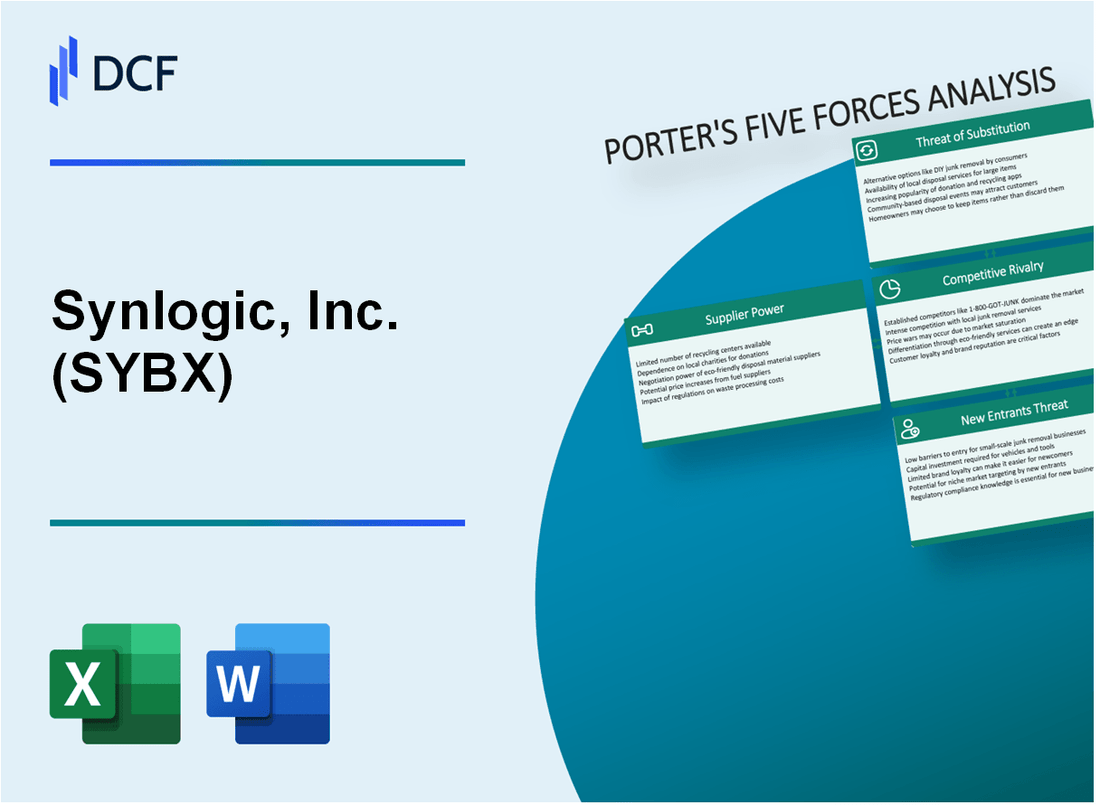

Synlogic, Inc. (SYBX) - Porter's Five Forces: Bargaining power of suppliers

You're analyzing Synlogic, Inc. (SYBX) and supplier power is a key area to watch, especially given the specialized nature of their Live Biotherapeutic Product (LBP) development. Honestly, for a company at this stage, the suppliers-especially those who can handle the manufacturing-hold a significant hand.

The power of suppliers for Synlogic, Inc. (SYBX) leans toward high because of the reliance on specialized Contract Development and Manufacturing Organizations (CDMOs) capable of handling LBPs. This isn't off-the-shelf small molecule production; it requires niche expertise. The Biologics Contract Manufacturing Market, which encompasses this area, was valued at USD 21.2 billion in 2024 and is projected to reach USD 23.8 billion in 2025, showing growth, but the specific segment for commercial-scale LBP manufacturing remains constrained by the small number of qualified facilities.

This specialized nature is tied directly to the proprietary technology platform. Developing these Synthetic Biotic medicines requires specific, highly-skilled synthetic biology expertise. While Synlogic, Inc. (SYBX) has built internal capabilities, the need for large-scale, GMP (Good Manufacturing Practice) production pushes them toward external partners. The sheer demand in the broader LBP space, which was valued at USD 73.25 Bn in 2024, puts pressure on the limited manufacturing base.

The strategic collaboration with Ginkgo Bioworks for strain engineering is a double-edged sword. It definitely helps Synlogic, Inc. (SYBX) by providing access to a world-class platform, but it creates a single-source dependency for that specific, high-throughput strain optimization work. Here's the quick math on that initial commitment:

| Collaboration Aspect | Value/Term | Date Established |

|---|---|---|

| Initial Synthetic Biology Services Payment (Synlogic to Ginkgo) | $30.0 million | 2019 |

| Initial Service Period Duration | Five years (extendable) | 2019 |

| Ginkgo Equity Investment in Synlogic (at a premium) | $80.0 million | 2019 |

What this estimate hides is the ongoing cost structure post-initial payment, but the initial outlay shows the value placed on securing that expertise. Still, for the actual drug substance manufacturing-the LBP production-the limited global capacity gives current CDMOs definite leverage. If a clinical candidate like SYNB1934 moves toward commercialization, securing long-term, large-volume manufacturing slots will be a negotiation where the CDMOs know they have few competitors for that specific LBP process.

The supplier power is further concentrated by the following factors:

- Reliance on CDMOs with validated LBP track records.

- High switching costs due to re-validating engineered strains.

- The need for specialized equipment only found in select facilities.

- The overall high growth trajectory of the LBP market itself.

Finance: draft a sensitivity analysis on a 15% increase in projected 2026 CDMO service costs by Friday.

Synlogic, Inc. (SYBX) - Porter's Five Forces: Bargaining power of customers

You're looking at the customer power dynamic for Synlogic, Inc. (SYBX) as of late 2025, and the picture is dominated by the company's recent strategic pivot. The bargaining power of customers-payers, physicians, and patients-must be assessed against the backdrop of a company that has effectively ceased internal R&D operations to preserve capital.

Low power for individual patients stems from the inherent nature of the rare diseases Synlogic targeted, such as Phenylketonuria (PKU) and Classical Homocystinuria (HCU). For these conditions, the unmet medical need remains significant, especially given the limitations in efficacy and safety of current medical treatment options for many patients. This desperation for effective alternatives inherently weakens the negotiating position of any single patient.

However, the power shifts dramatically toward major payers-insurers and government bodies. These entities face the rising tide of ultra-high-cost therapies, with novel treatments in the rare disease space carrying annual price tags that can surpass \$2 million in 2025. Payers demand robust clinical efficacy and clear cost-effectiveness data to justify reimbursement for these novel biotherapeutics. For instance, while some health technology assessment bodies accept higher Incremental Cost-Effectiveness Ratios (ICERs) for orphan drugs-the UK's NICE has accepted £100,000 per Quality-Adjusted Life Year (QALY) for highly specialized technologies, compared to a standard £20,000-£30,000-the scrutiny remains intense for any new entrant, including Synlogic's remaining pipeline asset, SYNB1353 for HCU.

Physician prescribing power is strong in specialty markets, but it is constrained by the limited therapeutic armamentarium. For PKU, treatment options beyond strict dietary management were historically few, giving prescribing physicians significant influence over the choice between existing therapies and a novel option. Still, the discontinuation of the pivotal SYNB1934 trial in early 2024 fundamentally altered this dynamic for that specific indication.

The analysis of SYNB1934 highlights a past opportunity that is now historical context. The asset targeted a specialty market with a potential worldwide revenue opportunity previously estimated at >\$1 billion; this figure was associated with the drug candidate before the Synpheny-3 Phase 3 study was terminated for futility. The company's current reality is one of extreme cash preservation following that trial's cessation. The focus has shifted entirely to executing a strategic alternative, such as a merger or sale, making the customer power dynamic for new products less immediately relevant than the power held by potential acquirers.

Here's a quick look at the financial state underpinning this strategic shift as of late 2025, which dictates the company's current negotiating leverage with any potential partner or buyer:

| Metric | Value as of September 30, 2025 | Context/Comparison |

|---|---|---|

| Cash and Cash Equivalents | \$15.6 million | Projected to fund operations for at least 12 months. |

| Net Cash Used in Operating Activities (9M 2025) | \$3.4 million | Down 89% from \$31.1 million in the prior year period. |

| R&D Expense (9M 2025) | \$16 thousand | Represents a 99.8% drop, confirming operational wind-down. |

| Shares Outstanding | 11,698,919 | As of November 6, 2025. |

| Accumulated Deficit | \$444.2 million | As of September 30, 2025. |

The power of the customer base is now largely channeled through the few remaining stakeholders-primarily potential acquirers-who value the company's preserved liquidity of \$15.6 million and its public shell status. The internal R&D engine, which once drove product-specific customer negotiations, is effectively offline, with R&D expenses reduced to just \$16 thousand for the nine-month period ending September 30, 2025.

Synlogic, Inc. (SYBX) - Porter's Five Forces: Competitive rivalry

You're looking at the competitive landscape for Synlogic, Inc. (SYBX) as of late 2025, and honestly, the rivalry in the specific Phenylketonuria (PKU) market is where the rubber met the road for the company. The established players have significant commercial footprints, which is a tough hurdle for any newcomer, especially one whose lead candidate failed to clear its final R&D hurdle.

The rivalry in the PKU space is defined by established, high-value assets. BioMarin Pharmaceutical's PALYNZIQ (pegvaliase-pqpz) is a major force, showing 20% year-over-year revenue growth in Q2 2025. For context, BioMarin booked $303.9 million from PALYNZIQ in 2024. Its competitor, KUVAN (sapropterin), still holds relevance, with BioMarin booking $180.8 million from it in 2024. The overall global PKU treatment market was valued at $0.92 billion in 2025.

| Competitor Product | 2024 Revenue (USD) | 2024 Market Share (%) | 2025 Market Value Estimate (USD Billion) |

|---|---|---|---|

| PALYNZIQ (pegvaliase) | 303.9 million | 41.94% | 0.92 |

| KUVAN (sapropterin) | 180.8 million | Declining due to generics |

The rivalry extends beyond the immediate PKU competitors into the broader Live Biotherapeutics (LBP) space. Companies like Seres Therapeutics and 4D Pharma operate in this area, where the scientific and regulatory bar is exceptionally high. Synlogic's own experience underscores this; the company had to discontinue its pivotal Synpheny-3 trial for SYNB1934 in February 2024 after the Data Monitoring Committee indicated the trial was unlikely to meet its primary endpoint.

The competition was, until recently, intensely R&D-focused. Synlogic had banked on positive top-line, Phase 3 data for SYNB1934, which was expected in H1 2025, but that data readout never materialized commercially due to the trial termination. This failure highlights the severe risk associated with competitive positioning when a platform fails to deliver clinical proof against established standards of care.

Still, Synlogic's approach was designed with a key competitive differentiator in mind, even if the program was ultimately shelved. The design centered on an oral, non-systemically absorbed mechanism for rare metabolic disease treatment. This contrasts with PALYNZIQ, which is an injectable enzyme substitution therapy.

- - PALYNZIQ (pegvaliase) market share in 2024 was 41.94%.

- - KUVAN (sapropterin) market share is tempered by emerging generic competition.

- - Global PKU market size in 2025 is estimated at $0.92 billion.

- - Synlogic's cash position as of September 30, 2025, was $15.6 million.

- - Synlogic's workforce as of September 30, 2025, was reduced to one full-time employee.

Synlogic, Inc. (SYBX) - Porter's Five Forces: Threat of substitutes

The threat of substitutes for Synlogic, Inc. (SYBX) products, particularly labafenogene marselecobac (SYNB1934) for Phenylketonuria (PKU), is substantial, coming from established treatments and emerging next-generation modalities.

High threat from existing, approved small molecule and enzyme replacement therapies for PKU.

- Existing therapies include sapropterin (Kuvan), which showed response rates of 10% to 40% in patients with more severe PKU in clinical trials.

- Injectable enzyme replacement therapy, pegvaliase (Palynziq), held the largest market share at 67.9% in 2024 and achieved target phenylalanine levels in 70% of adult patients in some analyses.

- The global PKU treatment market was valued at USD 1,180 million in 2025.

Future high-impact substitutes include gene therapy and mRNA-based treatments currently in development for metabolic disorders.

- R&D projects for gene therapies targeting metabolic disorders have seen a 50% increase.

- In late 2025, a personalized gene-editing therapy utilizing an mRNA-encoded base editor was administered to a patient with a rare metabolic disease.

- Multiple RNA-based drugs are slated for launch in 2025 in related rare disease spaces.

Dietary management remains a low-cost, primary substitute for PKU, despite its limitations and patient burden.

The traditional, strict, low-phenylalanine diet, supplemented by medical foods, represents the baseline for cost comparison. The annual cost to treat someone with medical foods was cited as approximately $7K per year. This contrasts sharply with the $70K per year cost cited for a pharmaceutical drug treatment, meaning the dietary substitute is priced at about 10 times less than some pharmaceutical options. Families reported spending over 300 h per year on shopping for and preparing special diet foods.

SYNB1934's potential to significantly lower phenylalanine (Phe) levels offers a functional advantage over many current substitutes.

Synlogic, Inc. (SYBX) is advancing SYNB1934 through its Synpheny-3 Phase 3 pivotal trial, which is set to enroll up to 150 patients with baseline Phe levels greater than 360μM.

| Metric | Existing Therapy (Sapropterin/Diet) | SYNB1934 (Phase 2 Data) |

| Response Rate (Phe reduction >20%) | 10% to 40% (Sapropterin in severe PKU) | 60% of patients met the criterion |

| Mean Phe Reduction (Responders) | Variable control | Averaged -42% |

| Mean Phe Reduction (All Comers) | N/A | -34% at Day 14 |

| Administration | Oral (Sapropterin) / Diet | Oral (Investigational) |

The Phase 2 data showed that for patients completing dosing, the day 14 mean change from baseline in fasting plasma Phe was -20% for the prior strain, SYNB1618, versus -34% for SYNB1934.

Synlogic, Inc. (SYBX) - Porter's Five Forces: Threat of new entrants

The threat of new entrants for Synlogic, Inc. remains low, primarily due to the substantial financial and regulatory hurdles inherent in developing a novel class of medicine like Synthetic Biotics.

The capital intensity of this sector creates a significant initial barrier. While Synlogic, Inc. has drastically reduced its operating expenses following a corporate restructuring in February 2024, the historical investment required to reach clinical stages is immense. New entrants face the same long development cycles typical of biotechnology, which demand sustained, high-level funding long before any revenue generation is possible. The accumulated deficit for Synlogic, Inc. stood at $444.2 million as of September 30, 2025, illustrating the scale of investment required to build a platform and pipeline.

Regulatory barriers for a novel class of medicine are significant. Live Biotherapeutic Products (LBPs) are regulated stringently, combining principles of both biologics and live-modified products. For a new entrant, navigating the evolving regulatory frameworks from agencies like the FDA is complex. The FDA expects developers to use at least two complementary methods for both microbial identification and active ingredient assessments. Furthermore, the only LBP-specific FDA guidance on Chemistry, Manufacturing and Control (CMC) in early clinical trials dates back to 2016, indicating that the framework is still maturing and requires developers to invest heavily in scientifically sound reasoning where uncertainty exists.

Intellectual property forms a strong moat. Synlogic, Inc.'s proprietary, engineered probiotic strains and the underlying synthetic biology platform are protected by patents; for example, a US Patent for a lead candidate was noted to extend until 2041. Establishing a competitive platform requires years of foundational research and significant investment in genetic engineering tools, such as CRISPR/Cas9, to confer functions not natively expressed by wild-type microorganisms.

Securing large-scale manufacturing capacity for LBPs acts as a major barrier to entry for smaller startups. Live biotherapeutics require specialized production platforms that adhere to strict aseptic conditions and robust quality controls to preserve viability and ensure safety. There is a noted market gap in affordable, modular biomanufacturing infrastructure, as current facilities demand massive capital investments. Very few Contract Development and Manufacturing Organizations (CDMOs) possess the dual expertise in both synthetic biology and Good Manufacturing Practice (GMP) for live microbes, forcing new entrants to either build expensive facilities or rely on a limited, high-cost external network.

Here's the quick math on Synlogic, Inc.'s capital position as of late 2025, which reflects the high capital hurdle for any new competitor:

| Financial Metric | Amount / Date |

|---|---|

| Cash and Cash Equivalents (as of Sep 30, 2025) | $15.6 million |

| Projected Cash Runway (from Sep 30, 2025) | At least the next 12 months |

| Accumulated Deficit (as of Sep 30, 2025) | $444.2 million |

| Example Patent Expiration Year (SYNB1934) | 2041 |

| Minimum Required ID/Assessment Methods (FDA for LBPs) | Two complementary methods |

What this estimate hides is the ongoing, high-cost requirement to advance even a single LBP candidate through late-stage clinical trials and scale-up, which is where most new entrants fail.

Finance: draft 13-week cash view by Friday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.