|

Wavestone SA (WAVE.PA): Porter's 5 Forces Analysis |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Wavestone SA (WAVE.PA) Bundle

Understanding the dynamics of competition in the consulting industry is pivotal for any stakeholder looking to navigate the landscape effectively. In this analysis of Wavestone SA, we'll explore Michael Porter’s Five Forces Framework, uncovering how the bargaining power of suppliers and customers, the intensity of competitive rivalry, the threat of substitutes, and the accessibility for new entrants shape the firm's strategic position. Stay with us as we dissect these forces to illuminate the intricate interplay influencing Wavestone's success.

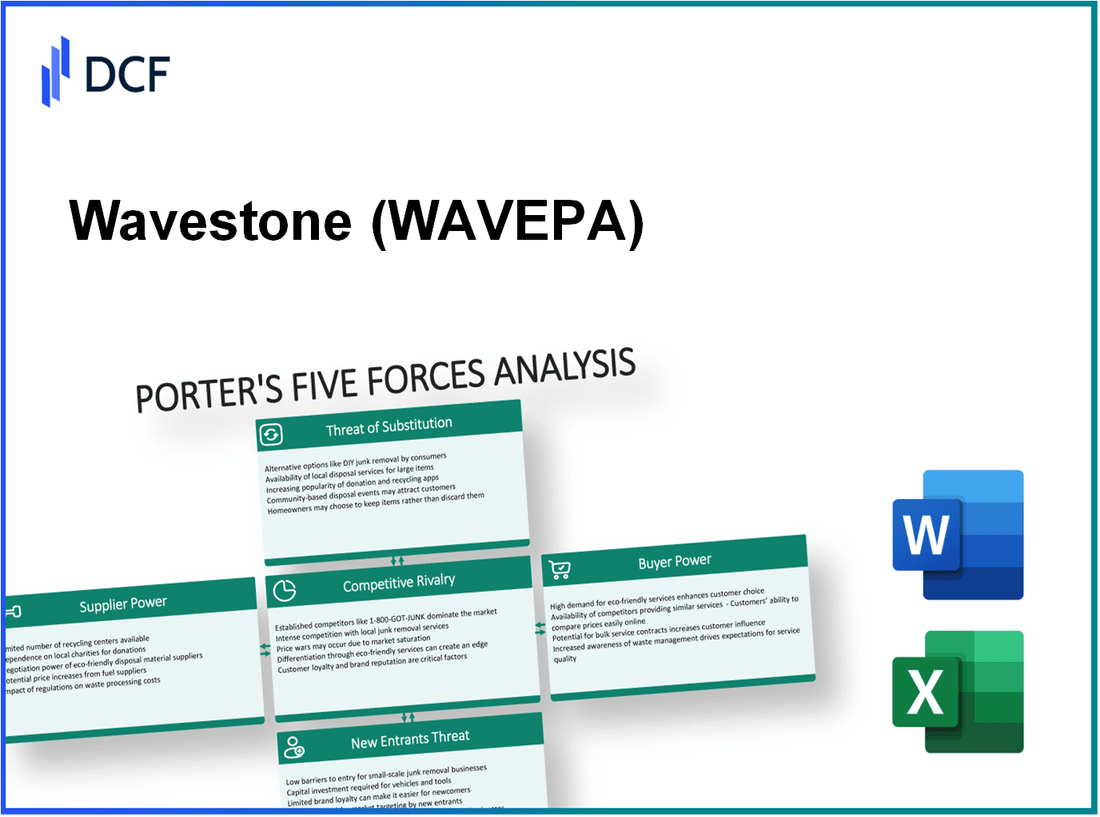

Wavestone SA - Porter's Five Forces: Bargaining power of suppliers

The bargaining power of suppliers for Wavestone SA is influenced by several key factors that shape the consulting industry's dynamics.

Limited number of specialized consulting firms

Wavestone operates in a sector characterized by a limited number of specialized consulting firms. As of 2023, the top consulting firms, such as McKinsey & Company, Boston Consulting Group, and Bain & Company, dominate the market. These firms offer similar services, creating a competitive landscape that limits Wavestone's options for sourcing specialized consultancy work.

Essential for niche technological expertise

Wavestone's focus on digital transformation and cybersecurity necessitates reliance on suppliers with niche technological expertise. For instance, the global cybersecurity market was valued at approximately $172 billion in 2021 and is projected to grow to $345 billion by 2026. This critical reliance on specialized suppliers enhances their bargaining power, as Wavestone must negotiate with firms that possess unique technical capabilities.

Potential high switching costs for unique suppliers

When engaging with specific technology providers or niche consulting firms, Wavestone faces high switching costs. For example, partnerships with leading data analytics firms such as Tableau can come with integration challenges. The costs of switching vendors can soar, often exceeding $1 million, depending on the contractual obligations and operational disruption, which further strengthens supplier power.

Opportunities for long-term partnerships

Wavestone has the opportunity to forge long-term partnerships with key suppliers. Such alliances can lead to preferential pricing and enhanced service levels. For example, Wavestone's alliance with Oracle reflects a strategic move to secure better pricing models, which are estimated to reduce costs by around 10-15% over the contract duration.

Supplier consolidation can increase power

Recent trends indicate significant supplier consolidation within the consulting industry. From 2020 to 2023, notable mergers, such as Accenture's acquisition of various digital agencies, resulted in decreased alternatives for companies like Wavestone. For instance, the market concentration ratio for the top four consulting firms rose to over 60%, giving consolidated suppliers greater leverage to negotiate higher prices and better contractual terms.

| Factor | Description | Impact on Supplier Power |

|---|---|---|

| Limited number of specialized firms | Dominance of top firms in the consulting market | High |

| Niche technological expertise | Dependence on specialized knowledge in cybersecurity and digital transformation | High |

| High switching costs | Cost of changing suppliers can exceed $1 million | High |

| Long-term partnerships | Strategic alliances can reduce costs by 10-15% | Medium |

| Supplier consolidation | Top four firms hold over 60% market share | High |

Wavestone SA - Porter's Five Forces: Bargaining power of customers

The bargaining power of customers in the case of Wavestone SA showcases several crucial factors that impact the consulting firm’s ability to maintain pricing and profitability.

Diverse client base across industries

Wavestone serves a variety of sectors including financial services, healthcare, telecommunications, and energy. As of 2022, the consultancy reported approximately 550 clients across these sectors. This diversity reduces dependency on any single industry, thereby mitigating the risk posed by any one client's bargaining power.

Possibility of large contracts increasing buyer power

Large organizations often engage in high-value contracts, significantly enhancing their bargaining power. In FY 2023, Wavestone secured a contract valued at €30 million with a major telecommunications provider. This illustrates how large clients can push for better pricing or additional services, reflecting their significant influence in negotiations.

Availability of alternative consulting options

The consulting market is saturated with notable competitors such as Accenture, Deloitte, and Capgemini, allowing clients to exercise considerable choice. In 2023, the global consulting market was estimated at $500 billion, with alternatives readily available for buyers seeking competitive pricing or specialized services. This competition empowers customers as they can switch firms more easily, particularly for standardized services.

High customization demand influences power balance

Clients often require tailored solutions, which complicates their decision-making process. According to Wavestone’s annual report, approximately 70% of projects demanded high customization in 2022. This customization reduces buyer power somewhat, as unique service offerings create dependency on Wavestone’s specialized knowledge and capabilities.

Price sensitivity varies by project scale

Price sensitivity among clients can fluctuate significantly based on project size. For smaller projects, clients may exhibit heightened price sensitivity due to budget constraints. For instance, projects under €100,000 saw negotiation pressures of up to 15% in fees. Conversely, for larger-scale projects, clients may show less sensitivity, illustrated by the fact that engagements over €1 million typically experience a 5% margin negotiation.

| Client Type | Project Size | Bargaining Power Impact (%) | Typical Contract Value (€) |

|---|---|---|---|

| Small Businesses | Under €100,000 | 15% | 75,000 |

| Medium Enterprises | €100,000 - €1 million | 10% | 500,000 |

| Large Corporations | Over €1 million | 5% | 3,000,000 |

Overall, the dynamics of customer bargaining power at Wavestone are influenced by a complex interplay between industry diversity, contract size, and customization needs. The presence of alternative consulting services enables clients to leverage competitive pricing, while large contracts can shift the balance of power toward buyers.

Wavestone SA - Porter's Five Forces: Competitive rivalry

Wavestone SA operates in a highly competitive landscape characterized by numerous global management consulting firms. The market includes major players such as McKinsey & Company, Boston Consulting Group, Accenture, and Deloitte, with combined revenues exceeding €150 billion annually. Each of these firms offers a wide range of consulting services, intensifying the competitive rivalry within the industry.

In particular, the demand for digital transformation services has surged, leading to intense competition among consulting firms. According to a report by Gartner, global spending on digital transformation was projected to reach €1.3 trillion in 2020 and is expected to grow at a rate of approximately 17% CAGR from 2021 to 2025. This rapid growth in the digital consulting sector amplifies rivalry as firms race to capture market share.

Wavestone differentiates itself through its specialized expertise in Information Technology, Operational Efficiency, and Risk Management. The firm reported revenues of €250 million in the latest fiscal year, with a focus on enhancing customer experience and operational efficiency for clients. This specialization allows Wavestone to position itself as a trusted advisor amidst fierce competition.

Market saturation is evident in regions like Western Europe, where many consulting firms are vying for a limited number of high-value contracts. A study indicated that 85% of consulting services were concentrated in major metropolitan areas, leading to diminishing returns for new entrants and heightened competition for existing players.

Competitive pricing pressures further complicate the landscape. The average hourly billing rate for top-tier consulting firms has seen a slight decline, with rates ranging from €250 to €500 per hour. Wavestone's pricing strategy incorporates competitive rates, resulting in a gradual increase of its market share, but also substantially impacting margins. The firm's gross margin was reported at 40%, reflecting the balance between competitive pricing and sustaining profitability.

| Consulting Firm | Annual Revenue (2022) | Market Focus | Average Hourly Rate |

|---|---|---|---|

| McKinsey & Company | €10.5 billion | General Management Consulting | €300 - €600 |

| Boston Consulting Group | €8.6 billion | General Management Consulting | €400 - €700 |

| Accenture | €50 billion | Digital Transformation, Technology | €200 - €500 |

| Deloitte | €60 billion | Audit, Consulting, Financial Advisory | €250 - €600 |

| Wavestone SA | €250 million | IT Consulting, Risk Management | €150 - €350 |

This dynamic competitive environment requires Wavestone to continuously adapt its strategies. Despite the intense rivalry, the firm has managed a steady revenue growth of approximately 5% year-over-year, indicating a resilient business model amidst these pressures. The emphasis on digital transformation ensures that Wavestone remains relevant and competitive, leveraging its specialized expertise to address complex client needs.

Wavestone SA - Porter's Five Forces: Threat of substitutes

The threat of substitutes in the consulting industry plays a crucial role in determining pricing strategies and market share. Wavestone SA, as a player in this market, faces various forms of competition that can impact its operations.

In-house consulting teams as alternatives

Many organizations opt for in-house consulting teams to reduce costs associated with external consultants. A survey by Deloitte in 2022 indicated that 54% of companies preferred using internal teams for strategic projects, up from 47% in 2021. This trend signifies a growing threat to traditional consulting firms like Wavestone.

Emerging small consulting startups

The rise of small consulting startups has increased competition within the industry. According to IBISWorld, the consulting sector saw a 3.5% annual growth from 2019 to 2023, with a notable increase in new entrants. Startups often leverage agile methodologies and niche offerings, attracting clients seeking specialized services.

Technology platforms offering DIY solutions

DIY consulting solutions facilitated by technology platforms are increasing in prevalence. Companies like Airtasker and Toptal provide advisory services that allow businesses to bypass traditional consulting routes. A report by Gartner in 2023 noted that 38% of organizations have utilized such platforms, leading to a potential 20% decrease in demand for traditional consulting services.

Non-traditional consulting models gaining traction

Consulting models that incorporate subscription services or performance-based pricing are gaining ground. For instance, companies like Upwork and Freelancer have redefined how advisory services are offered, allowing clients to pay only for the services used. This shift has led to a 15% year-over-year increase in preference for non-traditional consulting formats as reported in a 2023 McKinsey survey.

High customer loyalty may reduce threat level

Despite the threats posed by substitutes, Wavestone enjoys a relatively high level of customer loyalty. The firm's client retention rate stands at 85%, a robust figure compared to the industry average of 75%. Long-term relationships with clients allow for stable revenue streams, even in a competitive landscape.

| Type of Substitute | Market Impact (%) | Growth Rate (%) | Customer Loyalty (%) |

|---|---|---|---|

| In-house consulting teams | 54 | 6 | 85 |

| Small consulting startups | 3.5 | 3.5 | 75 |

| Technology platforms (DIY) | 38 | 20 | 65 |

| Non-traditional models | 15 | 15 | 70 |

Wavestone SA - Porter's Five Forces: Threat of new entrants

The consulting industry, where Wavestone SA operates, exhibits a structure that significantly influences the threat of new entrants. Here’s a deep dive into the factors affecting this threat.

High barriers due to reputation and expertise

Wavestone SA benefits from a strong reputation built over years of experience in management consulting and digital transformation. The company reported revenues of €319 million in the fiscal year 2023. A solid reputation and proven expertise create a substantial hurdle for newcomers who generally lack established credibility in the market.

Significant initial capital and resource requirements

Entering the consulting market requires significant initial investment in human resources, technology, and infrastructure. It is estimated that a consulting firm needs a minimum of €1 million to €5 million for initial setup, including salaries for senior consultants, technology systems, and marketing expenses. This high capital requirement discourages many potential entrants.

Established brand loyalty in consulting industry

Brand loyalty in the consulting sector is a profound factor that protects established players like Wavestone. A survey by Source Global Research indicated that 70% of clients in the consulting industry prefer to work with established firms due to trust and reliability. This customer loyalty acts as a barrier, making it difficult for new entrants to capture market share.

Regulatory and compliance challenges

Consulting firms must navigate a complex landscape of regulatory requirements, which varies by country and sector. Compliance with data protection laws, such as the EU's General Data Protection Regulation (GDPR), requires robust systems and expertise. Non-compliance can lead to fines of up to €20 million or 4% of annual global turnover, which can severely impact profitability and deter new entrants.

Innovation and niche focus can lower entry barriers

While substantial barriers exist, niches within the consulting industry allow for some lower entry points. Wavestone’s emphasis on innovation—such as their focus on digital transformation—opens avenues for new entrants who can offer specialized services. For instance, firms focusing on sustainable consulting or artificial intelligence may require lower initial investments, potentially disrupting traditional models.

| Factor | Details |

|---|---|

| Revenue of Wavestone SA (2023) | €319 million |

| Estimated Initial Investment Required | €1 million to €5 million |

| Client Preference for Established Firms | 70% |

| Potential Fine for GDPR Non-compliance | €20 million or 4% of annual global turnover |

Wavestone SA operates in a complex landscape shaped by Michael Porter’s Five Forces, where the dynamics between suppliers, customers, and competitors create both challenges and opportunities. Understanding these forces—ranging from the bargaining power of specialized suppliers to the competitive pressures from both established firms and new entrants—enables Wavestone to navigate its strategic decisions adeptly, ensuring it stays ahead in the ever-evolving consulting market.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.