|

SCWorx Corp. (WORX): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

SCWorx Corp. (WORX) Bundle

You're looking at a micro-cap like SCWorx Corp. (WORX) with only $2.78 million in trailing-twelve-month revenue and a $3.85 million market cap, and you need to know if this business can survive the pressure. Honestly, the picture is tight: the firm is bleeding cash with a -139.71% net margin and revenue is shrinking by -13.64% year-over-year as of September 2025, which tells you rivalry is fierce and pricing is brutal. We've got high switching costs protecting them from customer flight, but that small size means losing one big healthcare system client is a defintely existential threat, plus specialized labor costs are high. So, let's cut through the noise and see exactly where the five forces are squeezing SCWorx Corp. the hardest right now.

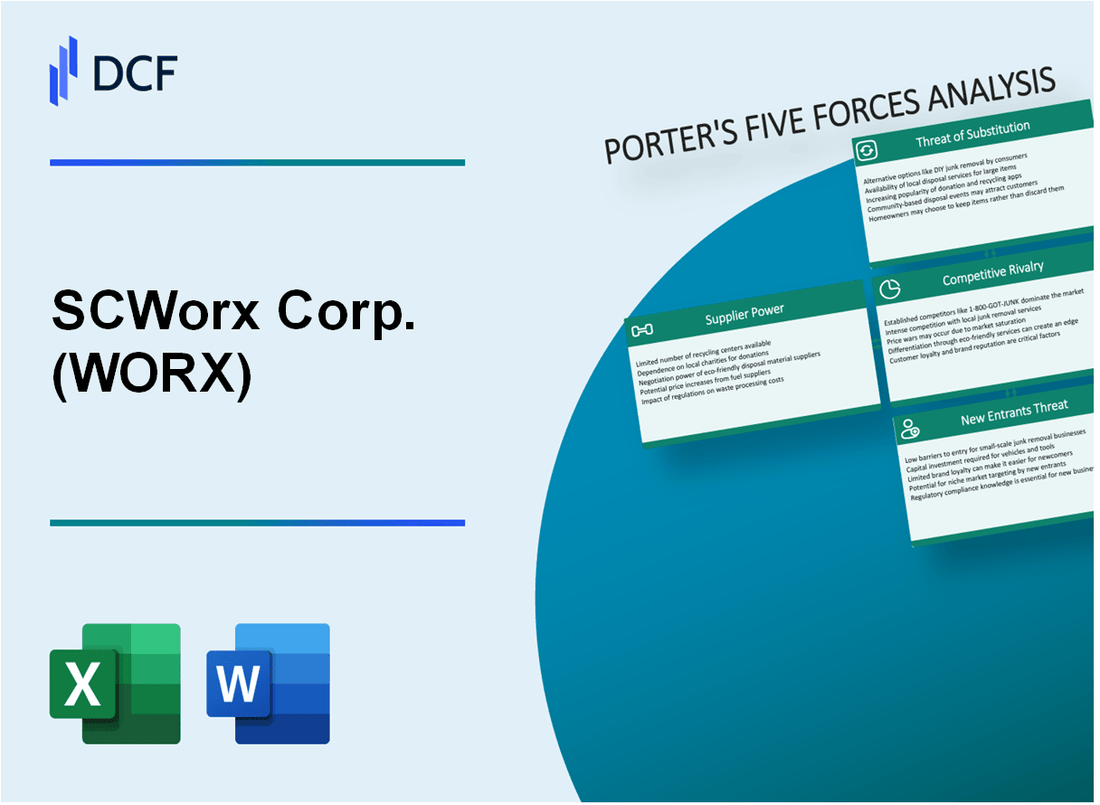

SCWorx Corp. (WORX) - Porter's Five Forces: Bargaining power of suppliers

You're analyzing SCWorx Corp. (WORX) and looking closely at who holds the cards when it comes to getting what the company needs to operate. For a software-as-a-service (SaaS) firm like SCWorx Corp., the supplier power dynamic shifts away from raw materials and heavily toward human capital and essential technology platforms.

Low reliance on physical inputs means SCWorx Corp. doesn't face the same volatility as a manufacturer dealing with commodity suppliers. However, their main supplier is specialized labor, which is a different kind of constraint. While the company reported a decrease in labor costs in the year ended December 31, 2024, that historical data doesn't reflect the current, highly competitive market for top-tier tech talent in late 2025. The power here comes from scarcity, not volume.

The power of cloud and infrastructure providers is definitely high, though we don't have SCWorx Corp.'s specific annual spend on AWS or Azure for 2025. Switching costs in this space are substantial; migrating a data management platform built on a specific infrastructure is a major undertaking, giving those providers inherent leverage over SCWorx Corp. The firm's new Chief Technology Officer, Anders Ohlsson, brings over 25 years of experience, including time at WideOrbit, suggesting deep awareness of the need to manage these critical, high-cost technology relationships effectively.

Key technical talent, specifically data scientists, commands high wages in a scarce market, directly impacting SCWorx Corp.'s operating expenses. If onboarding takes 14+ days, churn risk rises, and you have to pay to keep them happy. Here's the quick math on what that talent costs in the US market as of late 2025:

- Average total compensation for a Data Scientist: $145,858 annually.

- The 75th percentile salary range sits around $136,000.

- Top earners, like specialized AI Specialists, can command up to $220,000 annually.

- The average annual pay reported in November 2025 was $122,738.

Strategic partners, on the other hand, can actually reduce supplier power by creating guaranteed, high-volume demand for SCWorx Corp.'s services, effectively becoming a captive customer base. The August 2025 announcement of a new agreement with a leading healthcare supply chain consulting partner, which operates in all 50 states, solidifies a revenue stream. Even more telling is the October 2025 contract renewal with an existing aggregate purchasing group partner. That deal is for a new three-year term valued at approximately $1,692,000, representing a 113% increase over the prior contract. That kind of commitment gives SCWorx Corp. leverage against its own suppliers because it provides a more stable revenue base against which to negotiate terms.

To put these supplier-related dynamics in perspective, consider the following key figures from SCWorx Corp.'s recent operational and financial context:

| Metric | Value / Context | Date / Period |

|---|---|---|

| TTM Revenue | $2.78 million | Ending September 30, 2025 |

| Q3 2025 Quarterly Revenue | $705.8 thousand | Quarter Ended September 30, 2025 |

| New Partner Reach | Operations in all 50 states | August 2025 Agreement |

| Renewed Contract Value | Approx. $1,692,000 (3-year term) | October 2025 Renewal |

| Contract Value Increase | 113% increase over previous contract | October 2025 Renewal |

| FY 2024 Net Loss | $1,136,225 | Year Ended December 31, 2024 |

The power of the specialized labor supplier is a constant pressure point, definitely. The company's Market Cap as of November 26, 2025, was $4.03 million, meaning the cost of even a few key data scientists represents a significant portion of the firm's total valuation.

SCWorx Corp. (WORX) - Porter's Five Forces: Bargaining power of customers

You're analyzing SCWorx Corp. (WORX) and the customer side of the equation is definitely a major pressure point. When you look at the financials as of late 2025, the power held by their clients-large US healthcare systems-is amplified by the company's own diminutive scale.

High customer concentration means losing one client is a severe risk.

For a company of this size, losing even a single major contract can materially impact the top line. We see this risk explicitly acknowledged in the required disclosures; SCWorx Corp. includes a Schedule of Significant Customer Concentration Risk (Details) in its filings for the 9 Months Ended September 30, 2025, which references a specific 'Customer A'. This signals that the revenue base is not broadly diversified across many small players. To be fair, the renewal of one existing healthcare partner agreement in October 2025, which included a 113% increase in contract value, shows that while concentration is a risk, successful contract management can yield significant upside. Still, the concentration itself remains a structural vulnerability.

Customers are large, sophisticated US healthcare systems demanding cost savings.

SCWorx Corp. sells software for data normalization, application interoperability, and big data analytics to healthcare providers. These customers are not small practices; they are large, sophisticated US healthcare systems that negotiate hard for cost efficiencies. They understand the value of their data and the cost of poor data quality. This sophistication means they can push back effectively on pricing, demanding better terms or faster ROI realization. The company's Q3 2025 sales were reported at USD 0.705799 million, a figure that is small relative to the annual budgets of major hospital networks.

Switching costs are high once the data platform is integrated with ERP systems.

The stickiness of SCWorx Corp.'s offering is a key defense here. Their software deals with foundational business applications, including data repair, normalization, and interoperability. Once these systems are integrated with a hospital's Enterprise Resource Planning (ERP) systems and other core data warehouses, the cost and operational disruption of ripping out and replacing that infrastructure become substantial. If onboarding takes 14+ days, churn risk rises, but once fully embedded, the cost of switching is measured in months of downtime and data migration headaches, not just contract fees. This integration depth creates a natural barrier for customers looking to switch providers.

SCWorx's small size (Market Cap of \$3.85 million) limits its negotiation leverage.

The sheer size difference between SCWorx Corp. and its typical customer is stark, and the numbers tell that story clearly. The company's market capitalization as of late 2025 was reported at \$3.85 million. With only 7 employees and Trailing Twelve Months (TTM) revenue of only \$2.78 million, SCWorx Corp. simply lacks the scale to dictate terms to a large health system. Here's the quick math on the scale disparity:

| Metric | SCWorx Corp. (WORX) Value (Late 2025) | Implication for Customer Power |

|---|---|---|

| Market Cap | \$3.85 million | Extremely low negotiation leverage against large buyers |

| TTM Revenue | \$2.78 million | Any single contract loss represents a significant percentage of total business |

| Employees | 7 | Limited resources for complex, high-touch enterprise sales cycles |

| Q3 2025 Sales | \$0.706 million | Small quarterly revenue base compared to customer budgets |

This small size means that while SCWorx Corp. benefits from high switching costs, the customers hold the upper hand in initial pricing negotiations and ongoing service level agreement (SLA) discussions because the company needs the revenue more than the customer needs that specific vendor.

SCWorx Corp. (WORX) - Porter's Five Forces: Competitive rivalry

You're looking at the competitive landscape for SCWorx Corp. (WORX) as of late 2025, and the rivalry section is flashing red. The core issue here is that SCWorx Corp. is fighting in a market segment where the players are either much bigger or much more nimble, putting immense pressure on pricing and market share.

The sheer scale difference points to intense rivalry from larger companies with greater resources and product breadth. Think about it: SCWorx Corp. has only 7 employees as of November 26, 2025, while managing healthcare IT solutions that compete with industry giants. When you have a trailing twelve months (TTM) revenue of just $2.78M, you are competing against firms that can absorb losses, outspend on R&D, and offer bundled services that SCWorx Corp. simply cannot match on breadth.

This pricing pressure is starkly visible in the profitability metrics. The company's -139.71% net margin suggests aggressive price competition, or perhaps a severe mismatch between cost structure and realized revenue. Honestly, when your net margin is that deep in negative territory, it means you are either giving away services to gain a foothold or your operational costs are overwhelming the top line, which is a classic sign of being undercut by better-resourced rivals.

The competitive environment isn't just top-down; it's also horizontal and internal. Competition comes from smaller, specialized vendors who might focus on a single, high-demand niche better than SCWorx Corp.'s broader suite, and, critically, from internal hospital IT teams. Hospitals are always looking to bring data management and interoperability functions in-house to control costs and data governance, which directly threatens SCWorx Corp.'s service contracts.

This difficult environment is compounded by poor top-line momentum. Slow revenue growth, down -13.64% year-over-year (TTM Sep 2025), heightens rivalry. When revenue is shrinking while the market is supposedly growing-the industry saw growth of 17.06%-it forces the company to fight harder for every dollar of the shrinking piece of the pie it retains. Here's the quick math: Q3 2025 revenue was $705.80K, but the net loss for that same quarter was $-1.31M. That's a massive loss on relatively small sales.

To map out the pressure points SCWorx Corp. is facing in this rivalry, look at these key financial indicators as of late 2025:

| Metric | Value (TTM/Latest Reported) | Context |

|---|---|---|

| Revenue (TTM Sep 2025) | $2.78M | Small revenue base facing large competitors. |

| Revenue Growth (YoY TTM Sep 2025) | -13.64% | Indicates loss of market share or contract non-renewals. |

| Net Profit Margin (TTM) | -139.71% | Extreme unprofitability suggesting severe pricing or cost issues. |

| Employees (Nov 2025) | 7 | Extremely lean operation against resource-heavy rivals. |

| Q3 2025 Net Loss | $-1.31M | Loss significantly exceeds quarterly revenue of $0.71M. |

The implications of this rivalry are clear when you see the operational results:

- Pricing Concessions: The -139.71% net margin suggests SCWorx Corp. is likely engaging in price wars or taking on contracts with poor unit economics to maintain any revenue stream.

- Resource Disparity: With only 7 employees, the ability to service existing clients robustly while simultaneously pursuing new, large hospital system contracts is severely limited compared to competitors.

- Contract Churn Risk: The revenue decline of -13.64% YoY suggests that losing key contracts, as mentioned in the 10-K filing regarding non-renewals, is a persistent threat that larger players can exploit.

- Internal Competition: The push for internal IT solutions by hospitals means SCWorx Corp. is not just competing on features or price, but on the strategic decision of whether a hospital wants to buy or build.

Finance: draft 13-week cash view by Friday.

SCWorx Corp. (WORX) - Porter's Five Forces: Threat of substitutes

You're looking at the substitutes for SCWorx Corp. (WORX) services, and honestly, the threat here isn't just one big competitor; it's a collection of capable, in-house options and massive platform players that can absorb your core functionality. We need to map out the cost and capability of these alternatives to see how much pressure they put on your pricing power.

Hospitals can use internal IT teams to build data normalization tools.

Building a custom data normalization tool in-house is a significant undertaking, especially in healthcare where compliance is non-negotiable. For a hospital deciding to go it alone, the initial development cost for an AI-powered software solution in this sector often ranges from $50,000 to $5,000,000 and higher. This high cost is partly due to the need to prepare sensitive data, which includes normalization across disparate Electronic Health Record (EHR) systems.

If you look at the personnel required, an in-house Data Engineer salary is listed at $159,000 annually for a full-time role, which is a fixed, ongoing cost you must factor in against a SaaS subscription. Furthermore, even after the initial build, maintenance is a factor; model retraining costs can run from $10,000 to $100,000+ per year. To put this in perspective for larger facilities, hospitals with more than 250 beds invest nearly $29 million on average in IT solutions yearly, meaning a multi-million dollar internal build is certainly within the budget of a major potential client, even if it's not their first choice.

What this estimate hides is the time to value; getting compliant is slow. For instance, achieving initial HIPAA compliance for a medium to large organization can require a budget starting at $50,000. If a hospital is already undergoing an EHR migration, the specific task of data normalization and mapping from a generic system can cost between $15,000 to $40,000 for that component alone. That's a direct, measurable cost that SCWorx Corp. (WORX) must beat or match in perceived value.

Major ERP/EHR vendors (e.g., Workday, Epic) can expand their data management modules.

The sheer market dominance of the major players means any expansion of their data capabilities directly threatens your market share. Epic Systems Corporation commands a massive 37.7% to 39.1% of the US acute care hospital market share as of 2025. When a hospital chooses Epic, they are already committing significant capital; the software installation for a large-scale project can cost between $2-10 million, with data migration adding another $1 to $5 million. If Epic enhances its native data management to cover the gaps SCWorx Corp. (WORX) fills, the marginal cost to the client to adopt that feature is far lower than adopting a third-party solution.

Workday, another giant, has a 23.42% market share in the broader Human Capital Management space, and their 2025 revenue was reported at $8.45 billion. With over 31,131 companies using Workday for HCM as of 2025, and with expertise in Financial Management modules being highly sought after, any move to integrate deeper data normalization capabilities within their platform creates a powerful, all-in-one substitute for clients already invested in their ecosystem.

Here's a quick comparison of the scale of these vendors versus SCWorx Corp. (WORX)'s recent performance:

| Entity | Relevant 2025 Metric/Value | Context |

|---|---|---|

| SCWorx Corp. (WORX) TTM Revenue (Sep 30, 2025) | $2.78M | Trailing Twelve Months Revenue |

| Workday Revenue (as of Jan 31, 2025) | $8.45 Billion | Annual Revenue |

| Epic Systems Market Share (US Acute Care) | 37.7% to 39.1% | EHR Market Dominance |

| Workday HCM Market Share | 23.42% | HCM Category Share |

It's clear that the resources these vendors can dedicate to internal development dwarf SCWorx Corp. (WORX)'s current scale; their revenue is measured in billions, while SCWorx Corp. (WORX)'s is in millions.

Consulting firms offer project-based data cleansing as an alternative to SaaS.

Project-based work is a direct substitute for a recurring Software as a Service (SaaS) model. If a hospital prefers a one-time fix or a managed service for a specific data cleanup project, they turn to consulting. The overall Healthcare Consulting Services market is estimated to be worth between $21.9 billion and $34.53 billion in 2025, depending on the source. This is a massive pool of potential alternative spending.

The engagement model is key here: the project-based consulting segment dominated the market in 2024. Furthermore, the digital consulting segment, which covers data transformation and IT, is growing fast, projected to expand at a CAGR of 14.8% from 2024 to 2032. This signals that clients are actively funding large, discrete projects to solve data issues, which is exactly what SCWorx Corp. (WORX) offers, but on a project-by-project basis rather than a subscription.

The market forces supporting this substitution are strong:

- Project-based engagements dominated the delivery model in 2024.

- The overall Healthcare Consulting market size is estimated at $32.08 billion in 2025.

- Digital transformation consulting is a major trend, fueling project work.

- Roughly 30% of facilities entered 2025 non-compliant, creating advisory openings.

Group Purchasing Organizations (GPOs) offer contract management services that overlap.

Group Purchasing Organizations (GPOs) are another layer of substitution, particularly where SCWorx Corp. (WORX) might touch on vendor or contract data management. In the US, the GPO industry revenue is projected to hit $7.3 billion in 2025, showing an expansion of 1.6% in 2025 alone. Globally, the GPO service market is valued at $6.58 billion in 2025.

The healthcare segment is the core of this business, holding over 50% of the overall GPO market. GPOs offer services like contract negotiation and supply chain management, which can overlap with data management needs if a client views data normalization as a precursor to better contract utilization. If a GPO can provide sufficient data analytics or contract compliance tools as part of their core offering, it reduces the need for a specialized data normalization SaaS.

We see the GPO market as a significant, established alternative spend category:

| GPO Market Metric | Value (2025) | Source/Context |

|---|---|---|

| US GPO Industry Revenue Estimate | $7.3 Billion | Projected for 2025 |

| Global GPO Service Market Value Estimate | $6.58 Billion | Valuation for 2025 |

| Healthcare Segment Share of Global GPO Market | Exceeding 50% | Dominant Sector |

| US GPO Industry Annual Expansion | 1.6% | Expansion in 2025 alone |

Finance: draft 13-week cash view by Friday.

SCWorx Corp. (WORX) - Porter's Five Forces: Threat of new entrants

You're looking at the barriers to entry for a new competitor trying to muscle into the healthcare data interoperability space where SCWorx Corp. operates. Honestly, the hurdles here are steep, primarily because the industry is so heavily regulated and requires deep, specialized knowledge to even get a foot in the door.

High regulatory and compliance requirements (HIPAA) create a significant barrier.

For any new entrant handling Protected Health Information (PHI), the Health Insurance Portability and Accountability Act (HIPAA) compliance is a mandatory, non-negotiable cost of doing business. This isn't just paperwork; it requires substantial upfront investment in technical safeguards. For a modern healthcare tech company in 2025, initial compliance costs can range from around $4,000 for a very small operation to well over $150,000 for a larger entity needing complex system overhauls.

To be specific about the required diligence, external risk assessments alone typically run between $5,000 and $20,000. Furthermore, the financial threat of non-compliance looms large; willful neglect violations can result in civil fines reaching up to $1.5 million annually. This mandatory spending acts as a significant capital floor that a startup must clear before generating a single dollar of revenue.

Here are some key financial implications of this regulatory barrier:

- Initial HIPAA setup cost range: $4,000 to $150,000+.

- External Risk Assessment cost: $5,000 to $20,000.

- Maximum annual fine for willful neglect: $1.5 million.

- Cost of compliance automation (potential savings): Estimated $1.45 million in operational costs saved.

Need for deep, specialized healthcare data expertise is a major hurdle.

Beyond the legal compliance, successfully navigating data repair, normalization, and interoperability-SCWorx Corp.'s core business-demands specialized domain expertise that takes years to build. A new entrant needs staff who understand not just data science, but the nuances of healthcare supply chain data, like the Item Master File, and various standards like EMR and MMIS (Medicaid Management Information System) data structures.

Consider the scale of the market a new player would be entering. The Global Health Data Interoperability Market is projected to be valued at USD 84.58 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of 22.65% through 2032. While the market is growing rapidly, it is also mature in North America, dominated by established players. SCWorx Corp. itself operates with only 7 employees, suggesting that the barrier isn't just capital, but the ability to hire and retain a small, highly effective team capable of delivering complex solutions like those that led to a recent contract renewal valued at approximately $1,692,000 over three years.

New entrants face high customer acquisition costs to displace incumbent systems.

If a new company manages the regulatory and expertise hurdles, they still face the high cost of convincing a hospital to switch from an existing vendor, which often means integrating with or replacing mission-critical systems. In the broader Medtech space for 2025, the average Customer Acquisition Cost (CAC) is cited at $921. For a specialized B2B healthcare data solution, this cost is likely at the higher end of the spectrum, especially when displacing an incumbent.

To give you a clearer picture of the sales friction in this sector, here is how CAC varies across different healthcare specialties, which you can use as a proxy for the difficulty in acquiring a new hospital client:

| Clinic Type Proxy | Average Paid CAC (2025 Estimate) | Average Organic CAC (2025 Estimate) |

|---|---|---|

| Neurology | $1,113 | $686 |

| Gastroenterology | $795 | $490 |

| General Practice | $477 | $294 |

| Dentistry | $350 | $216 |

The cost to acquire a new customer is high, and for SCWorx Corp., which reported revenue of $2.78 million for the trailing 12 months ending September 30, 2025, every new acquisition must be highly profitable to offset the operational losses, such as the $(1.26) million Loss from Operations reported for the fiscal year ending March 31, 2025. This means a new entrant must secure large, high-value contracts quickly to achieve viability.

The company's unique data platform for interoperability provides a defensible niche.

SCWorx Corp. has built a defensible position by focusing on the core problem of data quality and interoperability through a suite of integrated modules. This platform is designed to create a Single Source of Truth (SSOT) for a provider's data governance needs. New entrants must replicate this specific, integrated functionality to compete effectively.

The platform's key components that create this niche include:

- Virtualized Item Master File repair and automation.

- Data cleanse and normalization services.

- Contract management and automated rebate management modules.

- Data interoperability modules covering EMR, MMIS, and finance.

The stickiness of this solution is evidenced by customer behavior; for example, one existing partner renewed its agreement with a 113% increase in contract value, demonstrating the measurable value derived from the platform's ability to drive efficiency and cost savings. This level of integration and proven ROI makes displacing SCWorx Corp. a much more complex and expensive proposition for a hospital than simply adopting a new, standalone tool.

Finance: draft 13-week cash view by Friday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.