|

Hyperfine, Inc. (HYPR): 5 forças Análise [Jan-2025 Atualizada] |

Totalmente Editável: Adapte-Se Às Suas Necessidades No Excel Ou Planilhas

Design Profissional: Modelos Confiáveis E Padrão Da Indústria

Pré-Construídos Para Uso Rápido E Eficiente

Compatível com MAC/PC, totalmente desbloqueado

Não É Necessária Experiência; Fácil De Seguir

Hyperfine, Inc. (HYPR) Bundle

No cenário em rápida evolução da tecnologia de imagem médica, a Hyperfine, Inc. (HYPR) fica na encruzilhada da inovação e dinâmica do mercado. Ao dissecar a estrutura das cinco forças de Michael Porter, revelamos o complexo ecossistema que molda o posicionamento estratégico da empresa, revelando informações críticas sobre o poder do fornecedor, influência do cliente, desafios competitivos, potenciais substitutos e barreiras à entrada de mercado. Esta análise de mergulho profundo ilumina as forças intrincadas que determinarão a trajetória do hiperfino no US $ 5,7 bilhões Mercado de imagens médicas portáteis, oferecendo uma narrativa convincente de interrupção tecnológica e resiliência estratégica.

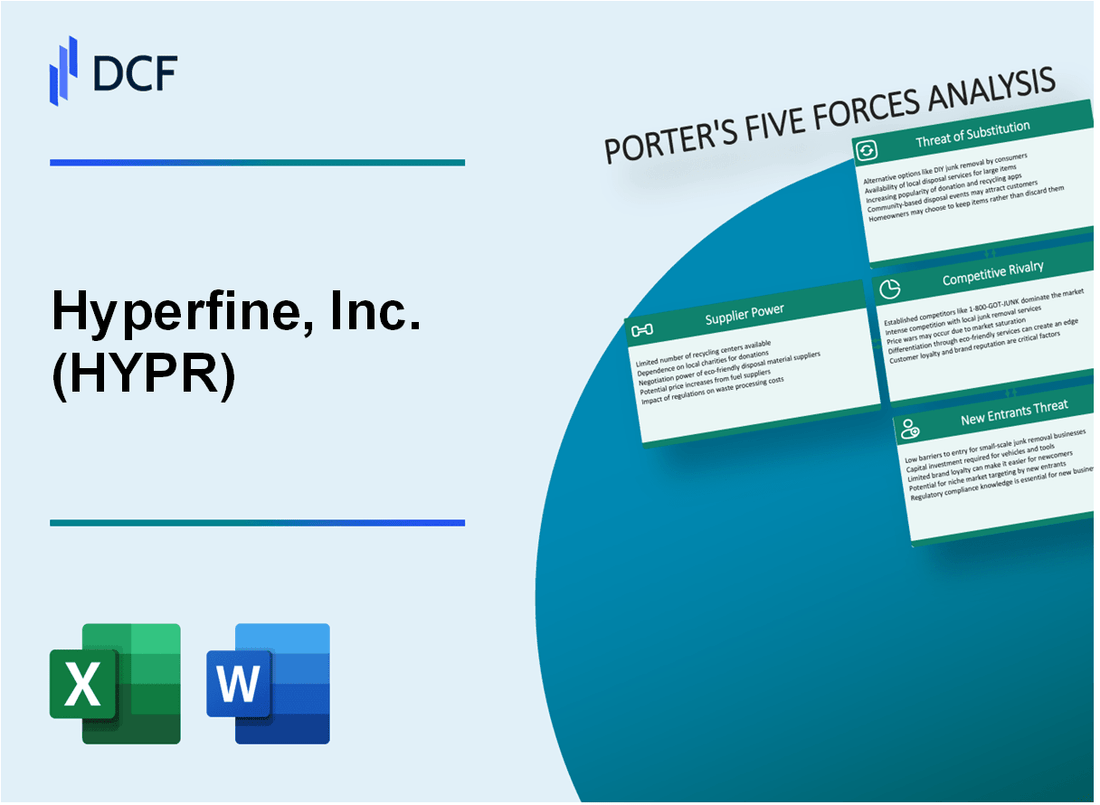

Hyperfine, Inc. (HYPR) - As cinco forças de Porter: poder de barganha dos fornecedores

Fabricantes de equipamentos de imagem médica especializados

A partir de 2024, o mercado global de equipamentos de imagem médica é estimada em US $ 39,6 bilhões, com apenas 4-5 grandes fabricantes dominando o segmento especializado em tecnologia de ressonância magnética.

| Fabricante | Quota de mercado | Receita global |

|---|---|---|

| Siemens Healthineers | 28.3% | US $ 21,4 bilhões |

| GE Healthcare | 25.6% | US $ 19,2 bilhões |

| Philips Healthcare | 22.1% | US $ 16,7 bilhões |

Fornecedores de componentes -chave para tecnologia de ressonância magnética

A Hyperfine, Inc. conta com uma base de fornecedores concentrada com altas barreiras tecnológicas.

- 3 fabricantes de ímãs primários globalmente

- 2 fornecedores críticos de fios supercondutores

- Aumentos médios dos preços dos componentes de 7,2% anualmente

Restrições da cadeia de suprimentos

A cadeia de suprimentos de componentes de imagem médica demonstra restrições significativas:

| Componente | Tempo de espera | Disponibilidade de fornecimento |

|---|---|---|

| Ímãs supercondutores | 18-24 meses | Limitado a 3 fabricantes globais |

| Componentes avançados de semicondutores | 12-16 meses | Fornecimento global restrito |

Análise de concentração de fornecedores

Métricas de concentração de fornecedores de fabricação de dispositivos médicos:

- Índice de Concentração de Fornecedor: 0,68

- Custos médios de troca de fornecedores: US $ 1,2 milhão

- Potencial de integração vertical: baixo (15,3%)

Hyperfine, Inc. (HYPR) - As cinco forças de Porter: poder de barganha dos clientes

Poder de compra do hospital e do centro médico

A partir de 2024, o mercado global de equipamentos de imagem médica está avaliada em US $ 39,6 bilhões, com hospitais representando 68% do volume total de compras. A Hyperfine, Inc. enfrenta um poder significativo de negociação de clientes das instituições de saúde.

| Segmento de clientes | Quota de mercado (%) | Orçamento médio de aquisição de equipamentos |

|---|---|---|

| Grandes hospitais | 42% | US $ 4,2 milhões anualmente |

| Hospitais médios | 33% | US $ 1,7 milhão anualmente |

| Centros médicos especializados | 25% | US $ 2,5 milhões anualmente |

Demandas institucionais de saúde

As instituições de saúde priorizam a relação custo-benefício e a qualidade em soluções de imagem. A sensibilidade média do preço para equipamentos de imagem médica é de aproximadamente 22-27% do orçamento total de compras.

- Requisitos de qualidade: 93% das instituições médicas exigem tecnologia de imagem de alta resolução

- Expectativas de redução de custo: 76% buscam equipamentos com despesas operacionais mais baixas

- Capacidade de integração de tecnologia: 81% requerem compatibilidade com registro médico eletrônico contínuo

Complexidade de tomada de decisão

O processo de aquisição de equipamentos médicos envolve uma média de 5,4 partes interessadas por decisão de compra institucional, aumentando o poder de negociação do cliente.

| Papel das partes interessadas | Porcentagem de influência |

|---|---|

| Diretor médico | 35% |

| Chefe do Departamento de Radiologia | 25% |

| Administrador do hospital | 20% |

| Diretor de Finanças | 15% |

| Gerente de compras | 5% |

O ciclo médio de compras para equipamentos de imagem médica é de 6 a 9 meses, com períodos de negociação normalmente em 3-4 meses.

Hyperfine, Inc. (HYPR) - As cinco forças de Porter: rivalidade competitiva

Concorrência emergente em tecnologia de ressonância magnética portátil e acessível

Em 2024, o mercado de ressonância magnética portátil mostra dinâmica competitiva significativa:

| Concorrente | Quota de mercado | Investimento de Tecnologia de ressonância magnética portátil |

|---|---|---|

| Hyperfine, Inc. | 7.2% | US $ 18,3 milhões |

| GE Healthcare | 42.5% | US $ 124,6 milhões |

| Siemens Healthineers | 33.7% | US $ 98,4 milhões |

| Philips Healthcare | 16.6% | US $ 52,9 milhões |

Presença de empresas de imagem médica estabelecidas

A análise da paisagem competitiva revela:

- Avaliação do mercado global da GE HealthCare: US $ 19,4 bilhões

- Receita de imagem médica da Siemens Healthineers: US $ 16,7 bilhões

- Philips Healthcare Diagnostic Imaging Segment: US $ 8,3 bilhões

Diferenciação por meio de soluções inovadoras e portáteis de ressonância magnética de baixo custo

Métricas de posicionamento competitivo Hyperfine, Inc.:

| Métrica de inovação | Valor |

|---|---|

| Despesas de P&D | US $ 12,6 milhões |

| Aplicações de patentes | 37 |

| Ciclo de desenvolvimento de produtos | 18 meses |

Aumentando a pressão do mercado para reduzir o preço do produto

Preço cenário competitivo:

- Custo médio do sistema de ressonância magnética portátil: US $ 250.000

- Preços do sistema Hyperfine, Inc.

- Tendência de redução de preços de mercado: 4,7% anualmente

Hyperfine, Inc. (HYPR) - As cinco forças de Porter: ameaça de substitutos

Máquinas de ressonância magnética em larga escala tradicionais

A partir de 2024, as máquinas de ressonância magnética tradicionais da General Electric, Siemens e Philips têm um custo médio de US $ 1,5 milhão a US $ 3 milhões por unidade. A penetração do mercado permanece alta, com aproximadamente 11.800 scanners de ressonância magnética nos Estados Unidos.

Tecnologias de imagem emergentes

| Tecnologia | Custo médio | Penetração de mercado |

|---|---|---|

| Ultrassom | $50,000 - $250,000 | 75.000 unidades globalmente |

| TCC de tomografia computadorizada | $250,000 - $600,000 | 6.500 unidades em nós |

| Ressonância magnética portátil | $200,000 - $500,000 | Mercado emergente |

Alternativas de diagnóstico de imagem

- Raios -X: Custo médio de US $ 50.000 - $ 150.000

- Imagem de medicina nuclear: US $ 500.000 - US $ 1,2 milhão

- Pet Scan: US $ 1 milhão - US $ 2,5 milhões

Limitações de custo e acessibilidade

Os gastos com saúde em imagem de diagnóstico atingiram US $ 30,8 bilhões em 2023. As tecnologias portáteis de ressonância magnética representam 3,2% do total de participação de mercado de imagens médicas. Os desafios de acessibilidade persistem, com áreas rurais com 40% menos tecnologias de imagem avançada em comparação aos centros urbanos.

Hyperfine, Inc. (HYPR) - As cinco forças de Porter: ameaça de novos participantes

Altas barreiras à entrada em tecnologia de imagem médica

O mercado de imagens médicas da Hyperfine apresenta barreiras substanciais de entrada com investimento inicial de capital estimado em US $ 50 a 75 milhões para o desenvolvimento de tecnologia.

| Categoria de barreira de entrada | Custo estimado | Tempo necessário |

|---|---|---|

| Pesquisar & Desenvolvimento | US $ 25-35 milhões | 3-5 anos |

| Conformidade regulatória | US $ 10-15 milhões | 2-3 anos |

| Configuração de fabricação | US $ 15-25 milhões | 1-2 anos |

Investimento de pesquisa e desenvolvimento

As despesas de P&D da Hyperfine em 2023 foram de US $ 18,4 milhões, representando 22,3% da receita total.

- A tecnologia de imagem médica requer inovação contínua

- Algoritmos avançados e integração de aprendizado de máquina

- Experiência em engenharia de precisão

Processos de aprovação regulatória

O processo de aprovação de dispositivos médicos da FDA leva uma média de 10 a 15 meses, com taxas de sucesso em torno de 33%.

| Estágio regulatório | Probabilidade de aprovação | Duração média |

|---|---|---|

| Notificação de pré -mercado (510k) | 67% | 6-9 meses |

| Aprovação de pré -mercado (PMA) | 33% | 10-15 meses |

Proteção à propriedade intelectual

A Hyperfine detém 37 patentes ativas a partir do quarto trimestre 2023, com custos de proteção de patentes que variam de US $ 250.000 a US $ 500.000 por patente.

Experiência técnica especializada

O Pool de talentos para imagens médicas Limited, com salário médio especializado em engenheiros em US $ 145.000 anualmente.

- Graus avançados necessários

- Experiência especializada mínima de 5 a 7 anos

- Conhecimento interdisciplinar obrigatório

Hyperfine, Inc. (HYPR) - Porter's Five Forces: Competitive rivalry

You're looking at Hyperfine, Inc. (HYPR) in a market dominated by behemoths. Honestly, the competitive rivalry here is a David versus Goliath story, but with a very specific, high-tech sling. The established, high-field MRI giants like Siemens Healthineers, GE Healthcare, and Philips are the incumbents you need to watch. These players have massive scale; for example, GE Healthcare's annual revenues exceed $19 billion, and Siemens Healthineers reported revenues close to $20 billion. To put Hyperfine's current standing in perspective, its preliminary Q3 2025 revenue was only $3.4 million, and management guided for full-year 2025 revenue between $13 million and $14 million.

Still, Hyperfine holds a distinct first-mover advantage in the niche of FDA-cleared, ultra-low-field portable MRI with its Swoop® system. This technology is FDA-cleared for brain imaging of patients of all ages, which carves out an access point inside intensive-care units and emergency rooms where conventional scanners can't go. The competition, therefore, isn't a direct, head-to-head battle on every metric. It's a competition based on fundamentally different value propositions.

The Swoop system offers unparalleled accessibility and portability, bringing imaging to the bedside. The incumbents, conversely, offer superior image quality from their conventional 1.5T/3.0T MRI systems, which are the gold standard for many complex diagnostic pathways. Here's a quick look at the scale difference you are dealing with:

| Metric | Hyperfine, Inc. (HYPR) | Major Incumbents (e.g., GE Healthcare/Siemens) |

|---|---|---|

| Primary Value Prop | Accessibility, Portability, Point-of-Care | Superior Image Quality, High Field Strength |

| Q3 2025 Revenue | $3.4 million | Billions (e.g., GE Healthcare > $19 billion annual revenue) |

| Market Position | First-mover in ultra-low-field portable MRI niche | Dominant market share in conventional MRI |

| Market Cap (as of one report) | $99.19 million | Not directly comparable; market cap in the tens or hundreds of billions |

The rivalry plays out in the sales cycle and market segmentation. Hyperfine is actively pushing into the neurology office setting, a segment largely untapped by traditional MRI vendors. This expansion is a direct attempt to create a new revenue stream that the giants haven't fully addressed with their high-cost, high-footprint machines. The challenge remains convincing clinicians to adopt the portable system when the established players are continuously integrating AI to improve their own image reconstruction and workflow efficiency.

The core of the rivalry is a trade-off between ubiquity and ultimate diagnostic power. Hyperfine's success hinges on proving that its enhanced image quality-especially with the Optive AI™ software rollout in Q3 2025-is sufficient for a wider range of clinical decisions, thus justifying the lower capital expenditure and operational footprint. If onboarding takes 14+ days for a traditional MRI, churn risk rises for Hyperfine's competitors in time-sensitive settings.

Finance: draft 13-week cash view by Friday.

Hyperfine, Inc. (HYPR) - Porter's Five Forces: Threat of substitutes

You're assessing the competitive landscape for Hyperfine, Inc. (HYPR), and the threat of substitutes is a major factor, particularly when you look at the established imaging giants. Conventional high-field MRI remains the primary, high-quality substitute for definitive diagnosis, even with the advancements in the Swoop® system.

To put the capital expenditure in perspective, a fixed conventional MRI unit, based on older data, was estimated to cost between $992,400 and $1,984,800 in 2018 US dollars, including installation. This massive installed base represents a significant barrier to entry for a full replacement strategy, but it also highlights the cost differential against Hyperfine, Inc.'s offering.

CT scans are a faster, lower-cost substitute for acute neuro-triage, a key Swoop use case. While final 2025 out-of-pocket costs are variable, general historical data suggests a typical CT scan cost around $1,200 compared to an MRI at about $2,000. Speed is the real differentiator here; a typical CT scan lasts about 10 minutes, whereas MRIs can take up to an hour or longer. This speed advantage makes CT the default for time-sensitive decisions.

However, the Swoop system is positioned to address an unmet need (bedside imaging for unstable patients), which reduces the substitution threat in that specific niche. For instance, in a 2022 study examining ICU patients, the turnaround time for a point-of-care MRI was significantly reduced to 5.3 hours compared to 11.7 hours for a fixed MRI. Still, that same study noted that 10 of 36 point-of-care MRIs were not of diagnostic quality, mainly due to patient motion, and five of those required follow-up with fixed MRI which then revealed acute or subacute infarctions.

The threat remains high as the Swoop system is not a replacement for fixed conventional MRI; it is a complementary tool. Hyperfine, Inc.'s Q3 2025 results show they sold 8 commercial Swoop® systems, with a preliminary effective average device selling price of approximately $360,000 for the quarter. The next-generation subsystem carries an MSRP of $550,000. This pricing is a fraction of fixed MRI capital cost, but the clinical utility gap is what keeps the high-field machines relevant for definitive, non-emergent diagnosis.

Here's a quick look at how the substitutes stack up against the current commercial reality for Hyperfine, Inc. as of late 2025:

| Imaging Modality | Estimated Capital Cost (Reference) | Typical Scan Time (Brain) | Diagnostic Quality Context |

| Fixed Conventional MRI | $992,400 - $1,984,800 (2018 USD) | Up to 60+ minutes | High-quality, definitive diagnosis |

| CT Scan | Lower capital cost (not specified for fixed/mobile comparison) | Approx. 10 minutes | Faster, lower cost, but less soft tissue detail |

| Swoop System (Portable MRI) | Approx. $360,000 (Q3 2025 Avg. Selling Price) | Faster than fixed MRI (ICU context: 5.3 hours turnaround vs 11.7 hours) | 72% diagnostic quality in one study; used for acute triage |

You should track these points as you model the substitution risk:

- Fixed MRI is the gold standard for image quality.

- CT is preferred for speed in acute triage settings.

- 72% diagnostic quality was seen in a prior POC MRI study.

- Hyperfine, Inc. Q3 2025 revenue was $3.4 million.

- The next-gen Swoop MSRP is $550,000.

- Neurologists order 500 to 600 brain MRIs yearly, but only 5% of private offices have in-house imaging.

Finance: draft 13-week cash view by Friday.

Hyperfine, Inc. (HYPR) - Porter's Five Forces: Threat of new entrants

You're looking at the barriers to entry for a new company trying to replicate Hyperfine, Inc.'s position in the ultra-low-field, point-of-care brain imaging market. Honestly, the hurdles are substantial, especially given the regulatory landscape for medical devices.

High regulatory barriers exist, including lengthy and costly FDA/CE Mark clearances for Class C/D medical devices. Hyperfine, Inc. has already navigated this for its Swoop® system, securing its initial U.S. Food and Drug Administration clearance back in February 2020. More recently, in late 2025, the company obtained both CE Marking and UK Conformity Assessment (UKCA) approval for its Optive AI™ software. Successfully clearing these international regulatory bodies demonstrates a proven, expensive pathway that new entrants must replicate.

Significant capital is required for R&D; Hyperfine, Inc.'s Q3 2025 R&D expense was \$4.0 million. This level of sustained investment is necessary to advance the technology, as evidenced by their tenth software release, Optive AI™, which marked a critical inflection point in image quality.

Here's a quick look at the financial and regulatory anchors that keep the threat of new entrants relatively contained:

| Barrier Component | Metric/Data Point | Source Year/Period |

| R&D Investment Barrier | \$4.0 million (Q3 Expense) | Q3 2025 |

| Regulatory Hurdle (International) | CE Mark and UKCA Approval obtained for Optive AI™ software | September 2025 |

| First-Mover Validation | Sold 8 commercial Swoop® systems in the quarter | Q3 2025 |

| Technology Protection | Multiple granted patents for low field magnetic resonance imaging methods and apparatus | As of late 2025 |

Established distribution networks and clinical trust favor existing MedTech players. To be fair, convincing a hospital system or a private practice to adopt a new imaging modality requires overcoming inertia. Consider the neurology office setting: only 5% of private neurology offices currently have in-house imaging. This low penetration suggests that while there is an opportunity, the established players in traditional imaging have a strong foothold in the existing infrastructure and clinician workflows that Hyperfine, Inc. is trying to penetrate.

The ultra-low-field niche is protected by Hyperfine, Inc.'s intellectual property and first-mover clinical validation. The company holds granted patents covering core technology, such as 'Low field magnetic resonance imaging methods and apparatus' and specific B0 coil configurations. This IP portfolio creates a moat around the specific engineering required to achieve high-quality imaging at ultra-low fields. Furthermore, the company's next-generation Swoop® system, which achieved 63% of unit sales in Q3 2025, represents validated, evolving technology that new entrants would have to match or surpass immediately.

You should track the speed of their next-gen adoption-it shows market acceptance is building fast.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.