|

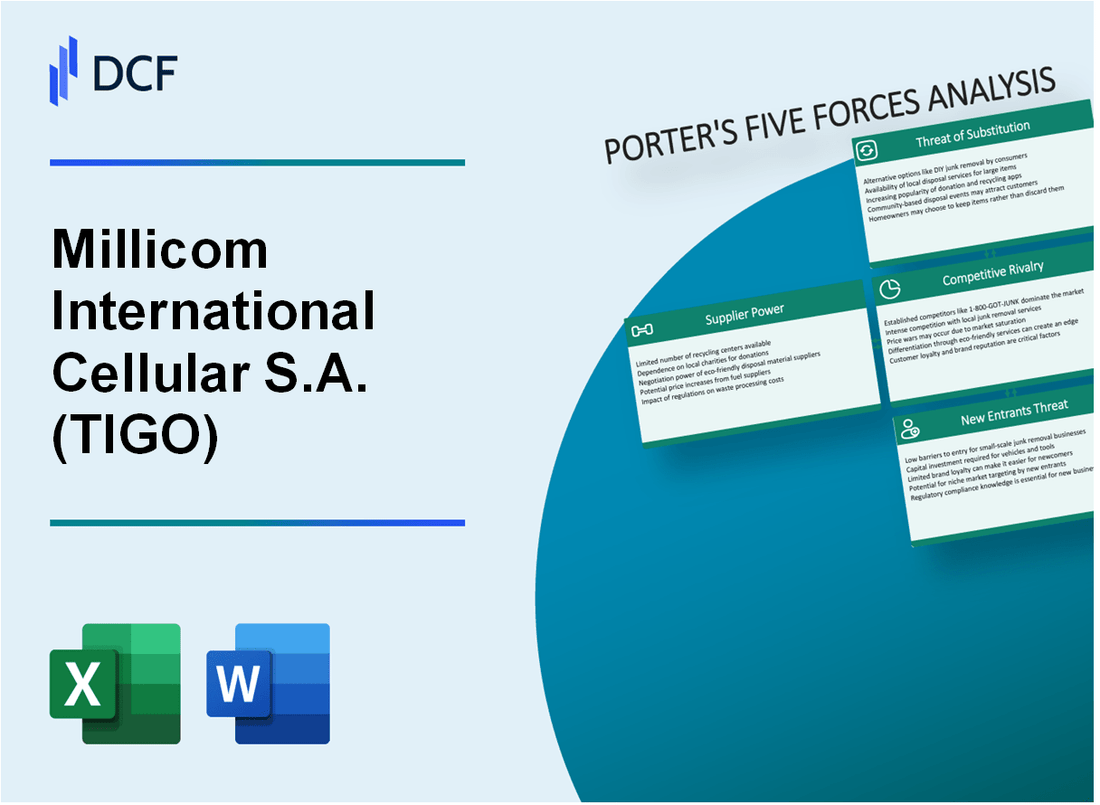

Análisis de 5 Fuerzas de Millicom International Cellular S.A. (TIGO) [Actualizado en Ene-2025] |

Completamente Editable: Adáptelo A Sus Necesidades En Excel O Sheets

Diseño Profesional: Plantillas Confiables Y Estándares De La Industria

Predeterminadas Para Un Uso Rápido Y Eficiente

Compatible con MAC / PC, completamente desbloqueado

No Se Necesita Experiencia; Fáciles De Seguir

Millicom International Cellular S.A. (TIGO) Bundle

En el mundo dinámico de las telecomunicaciones, Millicom International Cellular S.A. (TIGO) navega por un paisaje complejo de desafíos y oportunidades estratégicas. A través de la lente Five Forces de Michael Porter, descubrimos la intrincada dinámica competitiva que dan forma al posicionamiento del mercado de Tigo, revelando los factores críticos de poder de los proveedores, relaciones con los clientes, rivalidad de la industria, posibles sustitutos y barreras para los nuevos participantes del mercado. Este análisis de inmersión profunda expone los matices estratégicos que definen la estrategia competitiva de TIGO en el ecosistema de telecomunicaciones latinoamericano en rápida evolución.

Millicom International Cellular S.A. (TIGO) - Las cinco fuerzas de Porter: poder de negociación de los proveedores

Número limitado de fabricantes de equipos de telecomunicaciones

A partir de 2024, el mercado global de equipos de telecomunicaciones está dominado por tres fabricantes principales:

| Fabricante | Cuota de mercado global | Ingresos anuales (2023) |

|---|---|---|

| Huawei | 31.4% | $ 106.8 mil millones |

| Ericsson | 26.7% | $ 25.8 mil millones |

| Nokia | 22.5% | $ 23.1 mil millones |

Alta dependencia de los proveedores de infraestructura de red

Millicom International Cellular S.A. se basa en gran medida en estos proveedores clave para la infraestructura de red crítica.

- Costos de adquisición de equipos de red: $ 487 millones en 2023

- Gasto de capital en infraestructura: $ 612 millones

- Porcentaje de ingresos gastados en infraestructura de red: 18.3%

Costos de cambio significativos para la tecnología de telecomunicaciones

Los costos de cambio de la infraestructura de telecomunicaciones son sustanciales:

| Categoría de costos de cambio | Costo estimado |

|---|---|

| Reemplazo de equipos | $ 215- $ 350 millones |

| Reconfiguración de la red | $ 127- $ 228 millones |

| Gastos de integración | $ 93- $ 165 millones |

Mercado de proveedores concentrados

Las métricas de concentración del mercado de equipos de telecomunicaciones:

- Herfindahl-Hirschman Índice (HHI): 2,450 puntos

- Control de los 3 principales fabricantes: 80.6% del mercado global

- Número de proveedores alternativos viables: 3-4 a nivel mundial

Millicom International Cellular S.A. (TIGO) - Las cinco fuerzas de Porter: poder de negociación de los clientes

Bajos costos de cambio para clientes móviles en mercados latinoamericanos

En 2023, las tasas de portabilidad del número móvil en América Latina alcanzaron el 8,7% en los mercados clave. La tasa de rotación de clientes de Millicom fue del 2.9% en el tercer trimestre de 2023, lo que refleja barreras de lealtad de clientes relativamente bajas.

| Mercado | Tasa de portabilidad de número | Tiempo de cambio promedio |

|---|---|---|

| Colombia | 7.2% | 24 horas |

| Guatemala | 6.5% | 48 horas |

| Paraguay | 5.3% | 36 horas |

Alta sensibilidad a los precios en los mercados emergentes de telecomunicaciones

Los costos promedio del plan de datos móviles mensuales en los mercados operativos de Millicom oscilan entre $ 5 y $ 15, con la elasticidad de la demanda de precios en 1.4.

- Suscripciones móviles prepagas: 72% de la base total de clientes

- Ingresos promedio por usuario (ARPU): $ 6.30 en 2023

- Impacto de reducción de precios: 10% La caída del precio potencialmente aumenta la demanda en un 14,2%

Aumento de la demanda de los clientes de datos y servicios digitales

El consumo de datos móviles en América Latina creció un 45% en 2023, y Millicom experimenta un aumento del tráfico de datos año tras año.

| Servicio | Tasa de crecimiento 2023 | Uso promedio mensual |

|---|---|---|

| Datos móviles | 38% | 7.2 GB por usuario |

| Servicios digitales | 42% | $ 3.50 ARPU |

Crecientes expectativas del consumidor para paquetes de comunicación agrupados

La penetración del servicio agrupado de Millicom alcanzó el 35% en 2023, con paquetes de triple juego que aumentaron la retención de clientes en un 18%.

- Adopción del paquete de triple juego: 35%

- Mejora de retención de clientes: 18%

- Ingresos promedio de paquete: $ 24.50 por mes

Millicom International Cellular S.A. (TIGO) - Cinco fuerzas de Porter: rivalidad competitiva

Competencia intensa en el sector de telecomunicaciones latinoamericanos

A partir de 2024, el mercado de telecomunicaciones latinoamericanos demuestra una intensidad competitiva significativa. América Móvil controla el 59.4% de participación de mercado en América Latina. Millicom International Cellular S.A. posee aproximadamente el 16,3% de participación de mercado en sus regiones operativas primarias.

| Competidor | Cuota de mercado (%) | Ingresos (Millones de USD) |

|---|---|---|

| América Móvil | 59.4 | 24,673 |

| Millicom (Tigo) | 16.3 | 5,412 |

| Telefónica | 14.2 | 4,876 |

Competidores regionales fuertes

Los competidores regionales clave incluyen:

- América Móvil: Operando en 17 países

- Telefónica: presente en 10 mercados latinoamericanos

- Claro: activo en 8 países

Consolidación de la industria de telecomunicaciones

Las métricas de consolidación de la industria revelan:

- 3 fusiones importantes completadas en 2023

- Valor total de fusión: $ 6.2 mil millones

- Tamaño promedio de la transacción: $ 2.1 mil millones

Inversión de infraestructura de red

La inversión en infraestructura de telecomunicaciones en América Latina alcanzó los $ 12.7 mil millones en 2023, con Millicom Investing $ 987 millones en la expansión de la red y servicios digitales.

Competencia basada en precios en los mercados emergentes

| Mercado | Precio promedio de datos móviles | Presión de precios competitivos |

|---|---|---|

| Colombia | $ 0.12/GB | Alto |

| Guatemala | $ 0.15/GB | Medio |

| Paraguay | $ 0.10/GB | Muy alto |

Millicom International Cellular S.A. (TIGO) - Las cinco fuerzas de Porter: amenaza de sustitutos

Creciente popularidad de los servicios de Protocolo de Internet (VOIP)

El tamaño del mercado global de VoIP alcanzó los $ 43.8 mil millones en 2022, proyectados para crecer a $ 102.4 mil millones para 2027, con una tasa compuesta anual del 18.5%.

| Servicio VoIP | Usuarios activos mensuales | Cuota de mercado |

|---|---|---|

| Skype | 300 millones | 33% |

| 2 mil millones | 40% | |

| Zoom | 300 millones | 15% |

Aumento de la adopción de solicitudes de mensajería

Se espera que el mercado global de mensajería móvil alcance los $ 250.9 mil millones para 2028, creciendo con un 16,8% de CAGR.

- WhatsApp: 2 mil millones de usuarios activos mensuales

- Facebook Messenger: 1.300 millones de usuarios activos mensuales

- WeChat: 1.200 millones de usuarios activos mensuales

Aparición de plataformas de comunicación alternativas

Las alternativas de comunicación móvil generaron $ 85.6 mil millones en ingresos en 2023.

| Plataforma | Ingresos anuales | Base de usuarios |

|---|---|---|

| Discordia | $ 445 millones | 150 millones |

| Telegrama | $ 380 millones | 700 millones |

| Señal | $ 66 millones | 40 millones |

Impacto potencial de las tecnologías de comunicación basadas en Internet

Las tecnologías de comunicación basadas en Internet redujeron los ingresos tradicionales de las telecomunicaciones en un 22% en los mercados emergentes durante 2022-2023.

- Tamaño del mercado de WebRTC: $ 4.5 mil millones en 2023

- Mercado global de telefonía en Internet: $ 64.3 mil millones

- 5G Tecnologías de comunicación Inversión: $ 347 mil millones en todo el mundo

Millicom International Cellular S.A. (TIGO) - Las cinco fuerzas de Porter: amenaza de nuevos participantes

Altos requisitos de capital para la infraestructura de telecomunicaciones

Millicom International Cellular S.A. requiere aproximadamente $ 250 millones a $ 500 millones en inversión inicial de infraestructura para la implementación de redes en los mercados latinoamericanos. Los costos de construcción de la torre celular oscilan entre $ 150,000 y $ 300,000 por torre.

| Componente de infraestructura | Rango de inversión |

|---|---|

| Equipo de red | $ 75-150 millones |

| Torres celulares | $ 50-100 millones |

| Red de fibra óptica | $ 100-200 millones |

Barreras regulatorias significativas en los mercados de telecomunicaciones

El cumplimiento regulatorio de telecomunicaciones latinoamericanas exige recursos financieros y legales sustanciales.

- Costos de licencia de espectro: $ 50-300 millones

- Gastos de cumplimiento regulatorio: $ 10-25 millones anuales

- Procesos de aprobación del gobierno: 18-36 meses

Procesos de licencia complejos en países latinoamericanos

| País | Costo de licencia | Tiempo de aprobación |

|---|---|---|

| Colombia | $ 75 millones | 24 meses |

| Guatemala | $ 40 millones | 18 meses |

| Paraguay | $ 25 millones | 15 meses |

Inversiones tecnológicas sustanciales

La inversión tecnológica de TIGO requiere aproximadamente $ 100-200 millones anuales para actualizaciones de red e infraestructura tecnológica.

- Implementación de tecnología 5G: $ 75-150 millones

- Modernización de la red: $ 50-100 millones

- Infraestructura de ciberseguridad: $ 25-50 millones

Economías de escala que protegen a los proveedores de telecomunicaciones establecidos

Millicom International Cellular S.A. mantiene importantes ventajas del mercado a través de la economía de escala.

| Métrico | Valor |

|---|---|

| Suscriptores totales | 48.3 millones |

| Ingresos por usuario | $8.50 |

| Penetración del mercado | 62% |

Millicom International Cellular S.A. (TIGO) - Porter's Five Forces: Competitive rivalry

The competitive rivalry in Millicom International Cellular S.A. (TIGO)'s core Latin American markets remains fierce, characterized by a tight race for subscriber share and technology leadership. You see this most clearly in Colombia, where the landscape is dominated by three major mobile network operators (MNOs).

As of the end of December 2024, the Colombian mobile market held almost 103mn mobile lines total. América Móvil's Claro was the clear leader with 52.0mn connections, followed by Telefónica's Movistar with 20.8mn, and Millicom's Tigo with 16.7mn connections. WOM, recently saved from bankruptcy, held 7.7mn subscribers.

The battle for next-generation services is intense. By June 2025, 5G technology accounted for 12.4% of total mobile internet access, reaching 6.03 million connections, a massive 185.5% increase compared to 2024. Claro leads this segment with a 68.4% share as of June 2025, while Tigo held 15.7% and Movistar held 15.9%. In fact, Claro operated 92.2% of the nation's 1,433 active 5G sites as of June 2025, with Tigo/Movistar operating the remainder.

Millicom International Cellular S.A. (TIGO) is actively moving to consolidate its position, which directly impacts rivalry levels. This is evident in the M&A activity:

- Acquisition of Telefónica Uruguay for an enterprise value of $440M.

- Successful completion of the acquisition of Telefónica's operations in Ecuador for $380 million on October 30, 2025.

- The Ecuador deal added 5.2mn mobile customers, representing 28.3% of that market as of February 2025.

- The Uruguay deal added another 1.5mn mobile lines.

- The planned acquisition of a 67.5% stake in Movistar Colombia (Coltel) was valued at $400 million.

By March 2025, before the full integration of these deals, Millicom had 41.6mn mobile subscribers across Latin America. The company incurred a $25 million charge related to its strategic exit from Africa to fund this pivot.

Competition is inherently capital-intensive, driven by the necessary build-out of next-generation networks. Millicom projects its full-year 2025 Cash CapEx to be $677 million, matching the 2024 figure. This spending is set against a backdrop where leading Latin American telcos, including América Móvil and Millicom International Cellular S.A. (TIGO), are projected to have a combined capex of over $16bn in 2025, excluding acquisitions. For context, América Móvil allocated a $7 billion capital expenditure budget for 2024 to accelerate its 5G rollout.

The strategy of acquiring competitors is a direct move to reduce rivalry and drive consolidation. The combined Tigo and Movistar mobile internet connections under Millicom's control reached more than 17 million in the first half of 2025, still significantly behind Claro but far ahead of the fourth-ranked provider, WOM, which had 2.67 million connections. Millicom expects the Uruguay acquisition to be Equity Free Cash Flow (EFCF) accretive as early as 2026. The company's leverage ended Q1 2025 at 2.47x, with a stated aim to maintain leverage below 2.5x by 2026.

Here is a snapshot of the competitive structure in key markets based on recent data:

| Market Metric | Claro (América Móvil) | Tigo (Millicom) | Movistar (Telefónica/Millicom) | WOM |

|---|---|---|---|---|

| Colombia Mobile Connections (End-Dec 2024) | 52.0mn | 16.7mn | 20.8mn | 7.7mn |

| Colombia 5G Market Share (June 2025) | 68.4% | 15.7% | 15.9% | N/A |

| Ecuador Mobile Market Share (Feb 2025) | 53.8% | 28.3% (Post-acquisition) | 22% (Pre-acquisition) | N/A |

| Colombia Q1 2025 Service Revenue | N/A | $334 million | N/A | N/A |

| Colombia Q1 2025 Adjusted EBITDA Margin | N/A | 39.1% | N/A | N/A |

The capital intensity is further illustrated by the spending plans of the major regional players:

- Millicom International Cellular S.A. (TIGO) Projected 2025 Capex: $677mn.

- América Móvil Projected 2025 Global Investment: $6.7bn.

- Combined Leading LatAm Telco Capex (2025 Est.): Over $16bn.

- Colombia 5G Connections (End-Dec 2024): 3.8mn (7.7% of total mobile internet accesses).

Millicom International Cellular S.A. (TIGO) - Porter's Five Forces: Threat of substitutes

The threat from substitutes remains a significant structural pressure point for Millicom International Cellular S.A. (TIGO), particularly as Over-The-Top (OTT) applications directly cannibalize traditional revenue streams like voice, SMS, and Pay-TV services.

This substitution effect is defintely structural; you see evidence of people using less traditional voice services, which is mirrored globally by the increasing cost and declining appeal of legacy SMS for enterprise use cases. For instance, international SMS rates have spiked dramatically, in some cases rising by 40% to 500%, making alternatives more compelling for businesses reaching customers in South America.

In many developing markets where Millicom International Cellular S.A. (TIGO) operates, hyper-scalers like Google are actively moving significant traffic away from SMS channels, indicating a clear industry pivot away from this traditional service.

Millicom International Cellular S.A. (TIGO) counters this substitution risk by aggressively scaling its B2B digital services portfolio, which includes cloud, cybersecurity, and SD-WAN offerings. This strategic pivot is showing strong results in the latest reporting periods.

Here's a quick look at the numbers illustrating the dual dynamic of the threat and the company's digital response:

| Metric | Value (Late 2025 Data Point) | Context |

| Digital Services YoY Growth (B2B) | 35% | Cloud, Cybersecurity, SD-WAN Revenue Growth (Q3 2025) |

| Overall Service Revenue YoY Growth (Organic) | 3.5% | Millicom International Cellular S.A. (TIGO) (Q3 2025) |

| B2B Segment Revenue | $231 million | Q3 2025 |

| International SMS Rate Increase (Maximum Reported) | 500% | Illustrates cost pressure making substitutes more attractive |

| Total Customers Served | 46 million+ | As of June 30, 2025 |

The reliance on data-centric services is clear, but this also exposes Millicom International Cellular S.A. (TIGO) to alternatives that bypass traditional network infrastructure entirely.

The low-cost alternative of Wi-Fi-only communication, enabled by unlicensed spectrum technologies, presents a persistent substitution threat for data access, especially in areas with high fixed broadband penetration or where mobile data costs remain a barrier for end-users.

The structural shift is evident in the growth disparity:

- Digital Services Revenue Growth: 35% year-over-year.

- Total Mobile Postpaid Customer Growth: 14% year-over-year (Colombia Q3 2025).

- Traditional Voice/SMS Revenue: Implied decline/stagnation relative to digital growth.

Finance: draft 13-week cash view by Friday.

Millicom International Cellular S.A. (TIGO) - Porter's Five Forces: Threat of new entrants

The threat of new entrants for Millicom International Cellular S.A. (TIGO) in the late 2025 landscape remains decidedly low, primarily due to formidable structural barriers to entry across capital, regulatory, and operational domains within its core Latin American markets.

Extremely High Capital Expenditure Requirements

Launching a competitive mobile and fixed network operation requires massive upfront and ongoing capital. Building out the necessary infrastructure, especially for next-generation services like 5G and Fiber-to-the-Home (FTTH), demands significant investment that deters most potential entrants. Millicom International Cellular S.A. (TIGO) itself has signaled its commitment to this scale of spending, planning to keep its annual Capital Expenditure (CapEx) envelope around ~$700 million for 2025. A new competitor would need to commit comparable, if not greater, sums just to achieve parity in network coverage and quality.

Prohibitive Spectrum Acquisition Costs and Taxation

Securing the necessary radio frequency spectrum licenses is a major hurdle. Spectrum pricing policies in Latin America show significant variation, and in some cases, costs are inflated by high annual taxes charged to license holders, as seen in Mexico. Industry experts have called for abolishing policies that unnecessarily raise spectrum costs to facilitate infrastructure deployment. While a direct comparison to European spectrum costs is complex, the focus on revenue maximization through high auction prices in the region acts as a significant financial barrier, effectively pricing out smaller or less capitalized players before they even begin network construction.

Significant Regulatory and Permitting Hurdles

Beyond the direct financial outlay, navigating the regulatory environment presents a bureaucratic challenge. In many Latin American countries, local regulations often conflict with federal authority, resulting in municipal permitting processes that are frequently restrictive, non-transparent, and bureaucratic for passive infrastructure deployment. These barriers increase the opportunity cost of deployment significantly. While some progress is being made-El Salvador introduced a single platform for unified fees, and Peru is drafting proposals to reduce environmental report approval times-the general complexity remains a deterrent. Furthermore, in some jurisdictions, specific fees are imposed with the purpose of either limiting infrastructure deployment or increasing government revenue, sometimes on an ad-hoc annual basis.

Scale of Incumbent Operations

The sheer scale of Millicom International Cellular S.A. (TIGO)'s established operations presents a formidable competitive moat. For a new entrant to pose a credible threat, it must be able to match the incumbent's existing market presence and financial footprint. Millicom International Cellular S.A. (TIGO)'s total revenue for the trailing twelve months ending Q3 2025 stood at $5.59 billion. This revenue base supports ongoing network investment, economies of scale in procurement, and the ability to absorb regulatory shocks that might cripple a smaller, newer competitor.

The barriers to entry can be summarized by the required investment profile:

- High annual CapEx commitment, estimated near $700 million for Millicom.

- Costly spectrum acquisition, often burdened by high regional taxes.

- Bureaucratic municipal permitting processes slowing deployment.

- Need to match incumbent scale, evidenced by TIGO's $5.59 billion TTM revenue.

The combination of massive required capital, high spectrum costs, and complex, often unpredictable municipal red tape means that only a well-funded, highly strategic global or regional player could realistically consider entering these markets, and even then, the path is fraught with friction.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.