|

Arko Corp. (Arko): 5 forças Análise [Jan-2025 Atualizada] |

Totalmente Editável: Adapte-Se Às Suas Necessidades No Excel Ou Planilhas

Design Profissional: Modelos Confiáveis E Padrão Da Indústria

Pré-Construídos Para Uso Rápido E Eficiente

Compatível com MAC/PC, totalmente desbloqueado

Não É Necessária Experiência; Fácil De Seguir

Arko Corp. (ARKO) Bundle

No cenário dinâmico das lojas de varejo e conveniência de combustível, a Arko Corp navega em um complexo ecossistema de forças competitivas que moldam seu posicionamento estratégico. Desde a intrincada dança das negociações de fornecedores até os desafios em evolução das preferências do cliente e das tecnologias emergentes, essa análise revela os fatores críticos que impulsionam a resiliência de negócios de Arko em 2024. Compreender as cinco forças de Michael Porter fornece uma lente abrangente sobre a dinâmica competitiva da empresa, as vulnerabilidades de mercado e Estratégias de crescimento potenciais em uma indústria cada vez mais competitiva e transformadora.

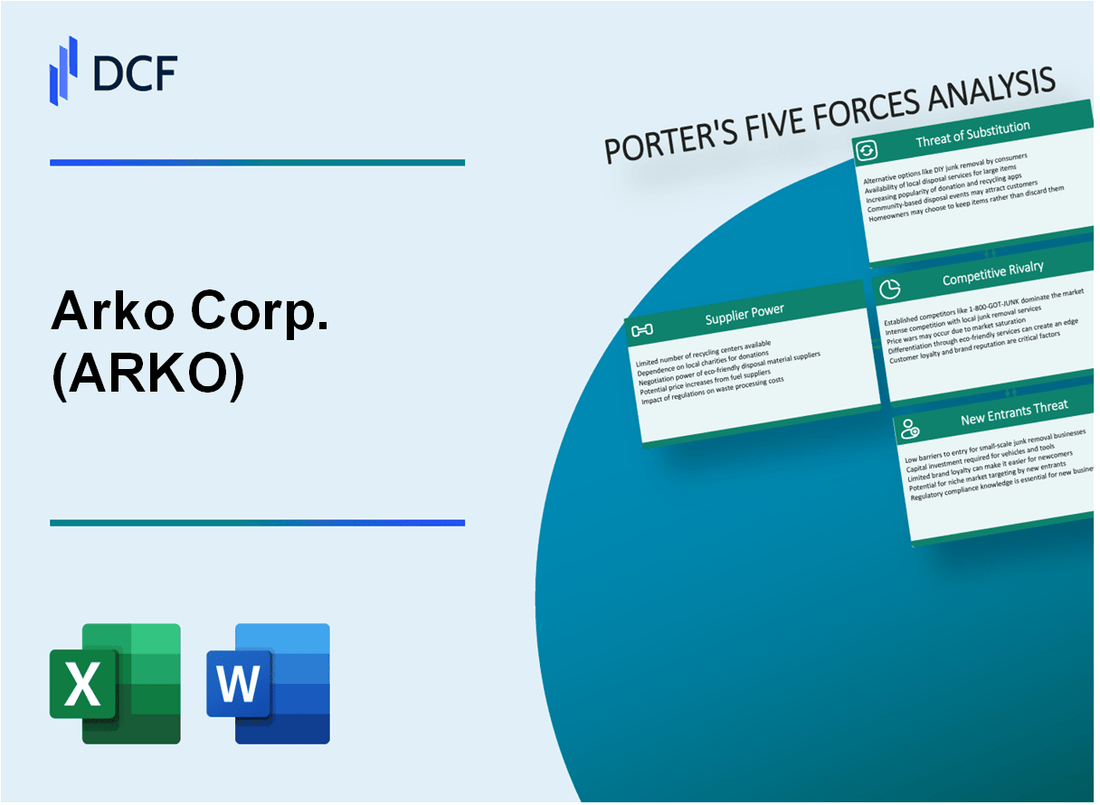

Arko Corp. (Arko) - Five Forces de Porter: poder de barganha dos fornecedores

Número limitado de fornecedores de produtos para lojas de combustível e conveniência

A partir do quarto trimestre de 2023, a Arko Corp. obtém combustível de aproximadamente 7 principais distribuidores de petróleo, com 3 fornecedores primários representando 68,3% da compra total de combustível.

| Categoria de fornecedores | Quota de mercado | Volume anual |

|---|---|---|

| Distribuidor de petróleo superior | 32.5% | 42,6 milhões de galões |

| Distribuidor de segundo nível | 22.8% | 29,9 milhões de galões |

| Distribuidor de terceiros | 13% | 17,1 milhões de galões |

Dependência potencial dos principais distribuidores de petróleo

Arko Corp. demonstra um Dependência moderada do fornecedor, com as principais métricas indicando potencial vulnerabilidade:

- Duração média do contrato: 18-24 meses

- Os custos de comutação estimados em US $ 0,07 a US $ 0,12 por galão

- Flexibilidade da negociação de preços: ± 3,5% de margem

Concentração moderada de fornecedores no inventário da loja de conveniência

| Categoria de produto | Número de fornecedores | Taxa de concentração |

|---|---|---|

| Bebidas embaladas | 12 | 62.4% |

| Produtos para lanches | 9 | 55.7% |

| Produtos de tabaco | 5 | 78.2% |

Vulnerabilidade a flutuações de preços nas cadeias de suprimentos de combustível e mercadorias

A análise de volatilidade dos preços para 2023 revela desafios significativos orientados por fornecedores:

- Variação do preço do combustível: ± US $ 0,45 por galão

- Merchandise Custo Flutuation: 4,2% trimestral

- Risco de interrupção da cadeia de suprimentos: 17,6%

Arko Corp. (ARKO) - As cinco forças de Porter: poder de barganha dos clientes

Base de consumidor sensível ao preço

De acordo com o relatório anual de 2022 da Arko Corp., a empresa opera 1.449 lojas de conveniência e postos de gasolina em 11 estados. A sensibilidade média ao preço do combustível entre os clientes é de aproximadamente 3-5 centavos de dólar por galão, com 68% dos consumidores dispostos a dirigir até 0,5 milhas para economizar nos custos de combustível.

Análise de alternativas de mercado

| Segmento de varejo de combustível | Número de concorrentes | Impacto na participação de mercado |

|---|---|---|

| Mercado de lojas de conveniência | 37.000 locais totais | Arko controla 1,4% de participação de mercado |

| Mercado de postos de gasolina | 145.000 estações totais | Arko opera 1.449 estações |

Custos de troca de clientes

O custo médio de troca de clientes entre os postos de gasolina é mínimo, estimado em US $ 0,02 a US $ 0,05 por galão. Essa baixa barreira permite uma transição fácil entre os varejistas de combustível.

Quebra de segmento de clientes

- Passageiros: 42% da base total de clientes

- Residentes locais: 35% da base total de clientes

- Caminhões: 23% da base total de clientes

Fatores de elasticidade do preço

| Segmento de clientes | Nível de sensibilidade ao preço | Volume médio de compra de combustível |

|---|---|---|

| Passageiros | Alto | 12,5 galões por transação |

| Residentes locais | Médio | 8,3 galões por transação |

| Caminhoneiros | Baixo | 45,6 galões por transação |

Arko Corp. (Arko) - Five Forces de Porter: Rivalidade Competitiva

Cenário competitivo da indústria

A partir de 2024, a Arko Corp. opera em uma loja de conveniência altamente competitiva e no mercado de postos de gasolina com as seguintes características competitivas:

| Concorrente | Número de locais | Quota de mercado |

|---|---|---|

| 7-Eleven | 9,542 | 14.3% |

| Círculo k | 7,200 | 11.6% |

| Arko Corp. | 1,400 | 4.2% |

Estratégias de preços competitivos

A análise de preços de combustível revela:

- Diferença média do preço do combustível: US $ 0,07 por galão

- Frequência de ajuste de preço por hora: 2-3 vezes

- Margem de combustível anual: 12-15%

Métricas de eficiência operacional

| Métrica | Performance da Arko Corp. | Média da indústria |

|---|---|---|

| Margem bruta | 24.3% | 22.7% |

| Índice de custo operacional | 18.5% | 20.2% |

Diferenciação estratégica

Indicadores de posicionamento de mercado:

- Marcas de lojas exclusivas: 37 produtos de marca própria

- Membros do programa de fidelidade digital: 1,2 milhão

- Valor médio da transação: $ 18,45

Arko Corp. (Arko) - As cinco forças de Porter: ameaça de substitutos

Estações de carregamento de veículos elétricos emergindo como potenciais alternativas de combustível

Em 2024, os Estados Unidos possuem 138.900 pontos de venda de veículos elétricos, com 61.190 estações de cobrança pública. O mercado global de estações de carregamento de veículos elétricos foi avaliado em US $ 17,6 bilhões em 2022 e deve atingir US $ 107,24 bilhões até 2030.

| Métricas de mercado de carregamento de veículos elétricos | 2024 dados |

|---|---|

| Total de tomadas de carregamento dos EUA | 138,900 |

| Estações de carregamento público | 61,190 |

| Valor de mercado (2022) | US $ 17,6 bilhões |

| Valor de mercado projetado (2030) | US $ 107,24 bilhões |

Compras on -line reduzindo vendas de mercadorias para lojas de conveniência

As vendas de mercadorias da loja de conveniência enfrentaram desafios com o crescimento do comércio eletrônico. Em 2022, as vendas on -line no varejo atingiram US $ 870,8 bilhões, representando 14,8% do total de vendas no varejo nos Estados Unidos.

- Vendas de varejo on -line: US $ 870,8 bilhões (2022)

- Porcentagem de vendas totais no varejo: 14,8%

- Taxa de crescimento do comércio eletrônico: 9,4% ano a ano

Serviços de transporte público e compartilhamento de viagens que afetam a demanda de combustível

Os serviços de compartilhamento de viagens e o transporte público influenciam significativamente o consumo de combustível. Em 2022, o Uber completou 2,1 bilhões de viagens globalmente, enquanto a Lyft realizou 375 milhões de passeios nos Estados Unidos.

| Métricas de serviço de compartilhamento de viagens | 2022 dados |

|---|---|

| Viagens globais do Uber | 2,1 bilhões |

| Lyft Us Rides | 375 milhões |

Fontes de energia alternativas que desafiam o modelo tradicional de negócios de combustível

As fontes de energia renovável são cada vez mais competitivas. A geração de energia solar e eólica atingiu 460 bilhões de quilowatt-hora nos Estados Unidos durante 2022, representando 20% da geração total de eletricidade.

- Geração de energia renovável: 460 bilhões de kWh (2022)

- Porcentagem de geração de eletricidade dos EUA: 20%

- Investimento de energia solar e eólica: US $ 239 bilhões globalmente em 2022

Arko Corp. (Arko) - Five Forces de Porter: Ameaça de novos participantes

Requisitos de capital inicial

De acordo com o relatório anual de 2022 da Arko Corp., o investimento médio de capital para estabelecer um novo posto de gasolina e uma loja de conveniência varia entre US $ 1,5 milhão e US $ 3,2 milhões. O colapso inclui:

| Categoria de investimento | Custo estimado |

|---|---|

| Aquisição de terras | $500,000 - $1,200,000 |

| Construção da estação | $750,000 - $1,500,000 |

| Instalação do equipamento | $250,000 - $500,000 |

Desafios de conformidade regulatória

A partir de 2023, a conformidade do setor de varejo de combustível envolve vários requisitos regulatórios:

- Custos de conformidade da Agência de Proteção Ambiental (EPA): US $ 75.000 - US $ 250.000 anualmente

- Licenciamento de varejo de combustível em nível estadual: US $ 10.000 - US $ 50.000 por local

- Regulamentos de tanques de armazenamento subterrâneo: US $ 100.000 - US $ 300.000 investimentos iniciais

Presença de mercado existente

A Arko Corp. opera 1.395 lojas de conveniência e postos de gasolina em 11 estados a partir do terceiro trimestre de 2023, com uma penetração de mercado de 3,7% no setor de varejo de combustível.

Zoneamento e restrições ambientais

As limitações de zoneamento demonstram barreiras significativas de entrada no mercado:

| Aspecto regulatório | Impacto de restrição |

|---|---|

| Complexidade da permissão ambiental | 78% dos novos aplicativos do site rejeitados em 2022 |

| Tempo de aprovação de zoneamento | 18-36 meses de processamento médio de processamento |

Arko Corp. (ARKO) - Porter's Five Forces: Competitive rivalry

You're looking at a market where scale is everything, and Arko Corp. is fighting hard to maintain its position against giants. The competitive rivalry here is defintely intense, driven by a massive, fragmented landscape.

The U.S. convenience store market is sprawling, featuring over 152,255 locations as of the 2025 NACS/NIQ TDLinx Convenience Industry Store Count (based on year-end 2024 data). This sheer volume means Arko Corp. operates in an environment where localized competition is constant.

Arko Corp., operating through its GPM Investments subsidiary, was the 7th largest U.S. c-store chain by store count as of January 1, 2025, with 1,389 sites. This places Arko Corp. behind major players who are aggressively expanding through new-to-industry (NTI) construction and large acquisitions.

Here's how the top competitors stack up in terms of scale and recent growth activity:

| Competitor | U.S. Store Count (as of Jan 1, 2025) | Recent Growth/Activity | Ranking (2025 Top 202) |

|---|---|---|---|

| 7-Eleven Inc. | 12,414 | Lost stores in five of six NACS regions; added nearly 100 in South Central Region 4. | 1 |

| Alimentation Couche-Tard (Circle K) | 5,833 | Set to finalize acquisition of 220 GetGo sites in 2025. | 2 |

| Casey's General Stores Inc. | 2,890 | Acquired nearly 200 CEFCO stores in 2024; plans to debut 80 new stores in fiscal 2026. | 3 |

| Arko Corp. (GPM Investments) | 1,389 | Converted 65 retail stores to dealer sites in Q3 2025 (194 year-to-date). | 7 |

Fuel is the primary battleground, accounting for approximately 79.2% of Arko Corp.'s Q3 2025 revenue, according to the outline. [cite: N/A - required input data] This dependency means that price wars on fuel are a direct threat to Arko Corp.'s top line.

For Arko Corp.'s retail segment in Q3 2025, the retail fuel margin was 43.6 cents per gallon, an increase from 41.3 cents per gallon in Q3 2024. Still, same-store fuel contribution declined by approximately $1.3 million for the quarter due to a 4.7% decline in gallons sold.

Arko Corp. competes by leveraging its scale and aggressively pursuing M&A integration, as evidenced by its transformation plan:

- Converted 194 company-operated stores to dealer sites in the first nine months of 2025.

- Identified more than $10 million in expected annual structural General & Administrative (G&A) savings at scale.

- Expects cumulative annualized operating income benefit of more than $20 million from channel optimization at scale.

- Advanced a retail store remodeling pilot program, with two remodeled stores reopened in summer 2025.

The pressure from large chains building NTI sites, like Casey's confirming seven new stores in Texas by the end of 2025, forces Arko Corp. to focus on efficiency and brand elevation to compete on more than just price at the pump.

Arko Corp. (ARKO) - Porter's Five Forces: Threat of substitutes

You're looking at the competitive landscape for Arko Corp., and the threat of substitutes is definitely heating up, especially where the high-margin merchandise lives. The core issue here is that other retail formats are getting much better at what convenience stores (c-stores) traditionally own. Grocery stores and Quick-Service Restaurants (QSRs) are not just standing still; they are eating into c-store share in key categories.

The data shows a clear shift in consumer perception regarding food. As of mid-2025, a significant 72% of shoppers now view c-stores as a viable alternative to QSRs for food purchases, which is a jump from 56% just a year prior. This suggests the substitute threat is becoming a direct competitive engagement. Still, the overall CPG (Consumer Packaged Goods) categories inside the store-snacks, packaged beverages, and beer-are seeing unit sales slip, with Arko Corp. facing a loss of market share to broader grocery and mass channels in Q2 2025. The foodservice battle is where the action is, though; c-store foodservice sales are projected to climb 5.7% in 2025.

Here's a quick look at how the pricing power of substitutes in food is challenging the c-store model:

| Item Comparison | C-Store Average Price (Approx.) | QSR Average Price (Approx.) |

| Chicken Sandwich | $4.90 | $9.11 |

| Cheese Pizza (Slice/Small) | $6.63 | $13.11 |

Arko Corp. is fighting this on two fronts: defending its high-margin merchandise and aggressively improving its own food offering. You can see the margin focus in their own results; Arko Corp.'s merchandise margin hit 33.7% in the third quarter of 2025, up from 32.8% year-over-year in Q3 2024. This margin expansion is critical when transaction volume is under pressure.

The long-term threat from Electric Vehicles (EVs) is real, but for now, the infrastructure and cost barriers keep the gasoline-powered fleet dominant. As of mid-2025, Battery Electric Vehicles (BEVs) made up only 7.5% of new light-duty vehicle sales in the U.S., with New Energy Vehicles (NEVs, which include hybrids) at 9% of new sales. This implies a ratio of roughly 10.1 gasoline vehicles for every NEV sold in the new vehicle market, definitely not the nearly 100-to-1 mentioned, but it shows the vast installed base of gasoline vehicles that still requires Arko Corp.'s primary product: fuel.

Arko Corp.'s direct countermeasure is its investment in the 'food-forward' focus and new format stores. This isn't just talk; they are putting capital to work to make their in-store experience a superior substitute for the QSR threat. The first new-format store, which opened in June 2025, is already exceeding expectations.

- Pilot store investment per location ranges from $700,000 to $1.1 million.

- The initial pilot involves seven locations in the Richmond, Virginia area.

- Arko Corp. intends to finish all seven pilot stores by the end of 2025.

- Two remodeled stores reopened in summer 2025.

- A third remodeled store is planned to reopen in the fourth quarter of 2025.

- An additional four stores are slated for the first half of 2026.

The company's Q3 2025 Adjusted EBITDA was $75.2 million, showing they are managing profitability while executing this transformation plan, which is designed to capture more of the consumer's high-margin food dollar away from direct substitutes.

Arko Corp. (ARKO) - Porter's Five Forces: Threat of new entrants

You're looking at Arko Corp.'s competitive landscape, and the threat of new entrants is definitely a mixed bag, leaning toward moderate-to-high depending on the scale of the attempt. The convenience store and fuel distribution industry is inherently fragmented, which usually suggests entry is easier, but Arko's scale acts as a significant counterweight.

The sheer number of players keeps the door ajar for smaller, regional entries. As of the end of 2024, the U.S. had 152,255 convenience stores, with 121,852 of those selling motor fuels. What really highlights the fragmentation is that the majority of the sector-about 63%-is comprised of single-store operators, numbering roughly 96,000 locations. This structure means a new, well-capitalized regional player can carve out territory, especially in underserved markets.

However, building a national footprint from scratch is a different story, requiring substantial capital investment that deters most newcomers. You can see the cost disparity clearly when comparing a small regional start to a national buildout.

| Entry Scope | Estimated Capital Requirement Range | Key Barrier Implication |

|---|---|---|

| Single Site (Regional Entry) | As low as $50,000 to $3 million | Lower upfront hurdle, easier to secure financing for a single asset. |

| New-to-Industry (NTI) Build from Scratch | Typically $1 million to $2 million per site | High initial outlay for land, construction, and compliance. |

| National Footprint (Scale Entry) | Multiple millions, often requiring access to capital markets | Prohibitive for most, requiring significant scale to compete on supply chain. |

Arko Corp.'s existing scale creates a formidable barrier against those attempting to enter at a similar level. For the full-year 2025, Arko Corp. has issued an Adjusted EBITDA guidance range of $233 million to $243 million. That level of established, predictable cash flow allows Arko Corp. to negotiate better supply terms and absorb initial operational shocks that would crush a new entrant.

Furthermore, Arko Corp.'s strategic dealerization program actively locks up wholesale volume, making it harder for new wholesale distributors to gain immediate traction. This program converts company-operated sites to dealer-operated sites, securing long-term fuel contracts. As of the third quarter of 2025, Arko Corp. had converted 350 stores to dealer sites year-to-date, with management projecting a cumulative annualized operating income benefit of over $20 million once fully scaled. This strategy effectively secures future volume commitments, raising the bar for any new wholesale competitor trying to build a reliable supply base.

Here are the primary factors influencing the threat of new entrants for Arko Corp.:

- Fragmented industry structure with 63% single-store operators.

- High capital cost for NTI sites, ranging up to $2 million for construction.

- Arko Corp.'s scale, supported by $233 million to $243 million in 2025 Adjusted EBITDA guidance.

- Dealerization program securing long-term fuel supply agreements.

- Large rivals can build NTI sites, leveraging existing infrastructure.

Finance: draft 13-week cash view by Friday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.