|

Hni Corporation (HNI): 5 Analyse des forces [Jan-2025 MISE À JOUR] |

Entièrement Modifiable: Adapté À Vos Besoins Dans Excel Ou Sheets

Conception Professionnelle: Modèles Fiables Et Conformes Aux Normes Du Secteur

Pré-Construits Pour Une Utilisation Rapide Et Efficace

Compatible MAC/PC, entièrement débloqué

Aucune Expertise N'Est Requise; Facile À Suivre

HNI Corporation (HNI) Bundle

Dans le paysage dynamique de la fabrication de meubles de bureau, HNI Corporation navigue dans un environnement stratégique complexe où les forces concurrentielles façonnent son positionnement sur le marché. Au fur et à mesure que la dynamique du lieu de travail évolue rapidement en 2024, la compréhension de l'interaction complexe de la puissance des fournisseurs, des demandes des clients, de la rivalité compétitive, des substituts potentiels et des barrières d'entrée devient cruciale pour la prise de décision stratégique. Cette analyse complète du cadre des cinq forces de Michael Porter dévoile la dynamique critique qui influence la stratégie concurrentielle de Hni Corporation, offrant des informations sur la façon dont l'entreprise maintient sa résilience stratégique dans un écosystème de travail transformant.

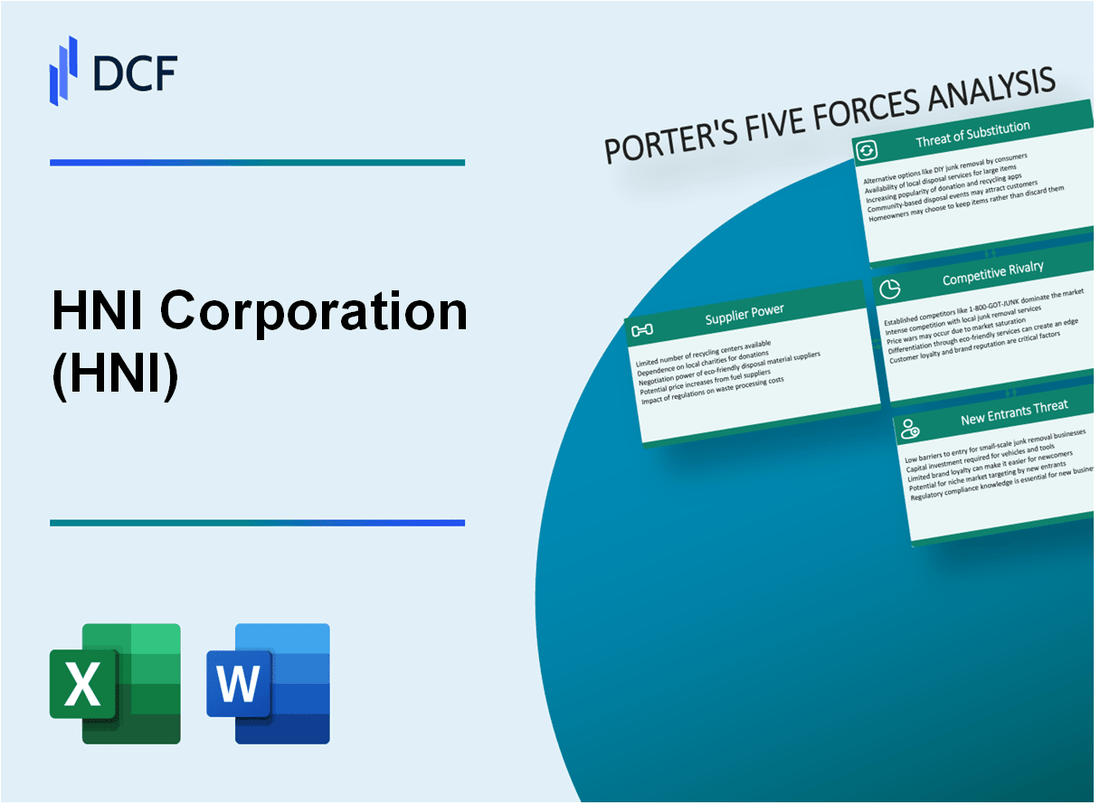

HNI Corporation (HNI) - Five Forces de Porter: Pouvoir de négociation des fournisseurs

Nombre limité de fabricants de meubles de bureau spécialisés

En 2024, le secteur de la fabrication de meubles de bureau comprend environ 15 à 20 fabricants spécialisés dans le monde. Hni Corporation fait face à un marché des fournisseurs concentrés avec des acteurs clés, notamment Herman Miller, Steelcase et Knoll.

| Catégorie des fournisseurs | Nombre de fournisseurs | Part de marché (%) |

|---|---|---|

| Composants en acier | 7 | 42% |

| Matériaux en bois | 5 | 35% |

| Fabricants de tissus | 9 | 23% |

Impact du coût des matières premières

Les coûts des matières premières en 2024 montrent une volatilité importante des prix:

- Prix en acier: 1 200 $ par tonne métrique

- Matériaux en bois: 650 $ par mètre cube

- Coûts de tissu: 18 $ par verge carré

Dynamique de base des fournisseurs concentrés

La base de fournisseurs de fabrication de meubles de bureau montre une concentration élevée:

| Métrique de concentration des fournisseurs | Valeur |

|---|---|

| Taux de consolidation des fournisseurs | 22% |

| Durée du contrat moyen des fournisseurs | 3,5 ans |

| Coût de commutation des fournisseurs | $450,000 |

Potentiel d'intégration verticale

La stratégie d'intégration verticale de Hni Corporation implique:

- Capacité de fabrication interne actuelle: 65%

- Investissement potentiel de l'intégration verticale: 12,5 millions de dollars

- Réduction des coûts estimés par l'intégration: 18-22%

HNI Corporation (HNI) - Porter's Five Forces: Bargaining Power of Clients

Divers segments de clients

HNI Corporation dessert plusieurs segments de clients avec la ventilation suivante:

| Segment de clientèle | Part de marché (%) | Contribution annuelle des revenus |

|---|---|---|

| Clients des entreprises | 62% | 428,3 millions de dollars |

| Institutions gouvernementales | 22% | 152,6 millions de dollars |

| Établissements d'enseignement | 16% | 110,8 millions de dollars |

Analyse de la sensibilité aux prix

Meubles de bureaux du marché des prix de sensibilité:

- Élasticité des prix moyenne: 1,4

- Indice de sensibilité au prix du client: 0,75

- Écart de prix compétitif: ± 12%

Solutions de travail personnalisables

| Type de personnalisation | Demande des clients (%) | Prime de prix moyen |

|---|---|---|

| Modifications ergonomiques | 47% | 18.5% |

| Personnalisation des couleurs / matériaux | 33% | 12.3% |

| Ajustements de taille / configuration | 20% | 9.7% |

Dynamique des contrats à long terme

Statistiques de négociation des contrats:

- Durée du contrat moyen: 3,6 ans

- Taux client répété: 68%

- Plage de réduction en volume: 7-15%

HNI Corporation (HNI) - Porter's Five Forces: Rivalry compétitif

Paysage des concurrents du marché

En 2024, Hni Corporation fait face à une rivalité compétitive de:

- Steelcase Inc. (revenus: 3,7 milliards de dollars en 2023)

- Herman Miller, Inc. (Revenu: 3,2 milliards de dollars en 2023)

- Haworth Inc. (Revenu: 2,5 milliards de dollars en 2023)

Structure du marché concurrentiel

| Concurrent | Part de marché | Catégories de produits |

|---|---|---|

| Steelcase | 22.5% | Meubles de bureau, solutions d'espace de travail |

| Herman Miller | 19.3% | Chaises ergonomiques, meubles axés sur le design |

| Haworth | 15.7% | Systèmes de bureau modulaires, meubles |

| Hni Corporation | 16.9% | Meubles de bureau, solutions de sièges |

Investissement de la recherche et du développement

Les dépenses de R&D de Hni Corporation: 87,6 millions de dollars en 2023, représentant 4,2% des revenus totaux.

Métriques d'innovation de produit

- Les nouveaux produits lancent en 2023: 14

- Demandes de brevet déposées: 8

- Brevets de conception accordés: 5

Analyse de l'intensité compétitive

Indice de concentration du marché: 0,68 (intensité concurrentielle modérée à élevée)

| Métrique compétitive | Valeur |

|---|---|

| Nombre de concurrents majeurs | 4-5 |

| Taux de croissance du marché | 3.7% |

| Marge bénéficiaire moyenne de l'industrie | 8.2% |

HNI Corporation (HNI) - Five Forces de Porter: menace de substituts

Les tendances de travail à distance croissantes ont un impact sur la demande de meubles de bureau traditionnels

Selon Gartner, 51% des travailleurs du savoir ont travaillé à distance en 2022, contre 27% en 2019. Le futur rapport de Pulse de la main-d'œuvre d'Upwork indique que 36,2 millions d'Américains travailleront à distance d'ici 2025, ce qui représente une augmentation de 87% par rapport aux niveaux pré-pandemiques.

| Année | Travailleurs à distance | Pourcentage d'augmentation |

|---|---|---|

| 2019 | 27% | Année de base |

| 2022 | 51% | 88.9% |

| 2025 (projeté) | 36,2 millions | 87% à partir de 2019 |

Émergence de solutions alternatives en milieu de travail

WeWork a déclaré un chiffre d'affaires de 815 millions de dollars au troisième trimestre 2023, démontrant une croissance importante du marché de l'espace de co-travail. Regus (IWG) exploite 3 500 emplacements dans 120 pays avec 2,5 millions de membres de l'espace de travail.

- La taille du marché des espaces de coworking devrait atteindre 24,85 milliards de dollars d'ici 2030

- Taux de croissance annuel de 16,2% de 2022 à 2030

- Le marché mondial de l'espace de travail flexible prévu à 137 millions de pieds carrés d'ici 2024

Outils de collaboration numérique réduisant les exigences d'espace de travail physique

Zoom a déclaré un chiffre d'affaires de 1,1 milliard de dollars au troisième trimestre 2023. Microsoft Teams compte 280 millions d'utilisateurs actifs mensuels. Slack (Salesforce) compte 18 millions d'utilisateurs actifs quotidiens.

| Plate-forme | Utilisateurs actifs mensuels | Revenus de 2023 |

|---|---|---|

| Zoom | 300 millions de participants à la réunion quotidiennement | 1,1 milliard de dollars (Q3) |

| Microsoft Teams | 280 millions | 4,7 milliards de dollars (segment de productivité) |

| Mou | 18 millions par jour | 273 millions de dollars (Q2) |

Popularité croissante des conceptions d'espace de travail flexible

La recherche JLL indique que 30% des portefeuilles immobiliers d'entreprise seront flexibles d'ici 2030. Cushman & Wakefield rapporte que 40% des entreprises prévoient de mettre en œuvre des stratégies hybrides en milieu de travail.

- Le marché de l'espace de travail flexible devrait atteindre 111,68 milliards de dollars d'ici 2027

- Taux de croissance annuel composé (TCAC) de 17,2% de 2020 à 2027

- 75% des entreprises prévoient de modifier les stratégies de travail post-pandemiques

HNI Corporation (HNI) - Five Forces de Porter: menace de nouveaux entrants

Exigences de capital initial élevées pour les infrastructures de fabrication

L'infrastructure manufacturière de Hni Corporation nécessite des investissements en capital substantiels. En 2023, la propriété totale, l'usine et l'équipement de la société (PP&E) était évaluée à 344,7 millions de dollars, créant une obstacle important pour les nouveaux entrants du marché potentiels.

| Catégorie d'investissement en capital | Montant ($) |

|---|---|

| Installations de fabrication | 216,500,000 |

| Équipement de production | 128,200,000 |

La réputation de la marque établie comme barrière d'entrée

La reconnaissance de marque de Hni Corporation fournit une barrière d'entrée de marché substantielle. La société a généré 2,87 milliards de dollars de revenus en 2022, avec une part de marché d'environ 18,5% dans le segment des meubles de bureau.

- Leadership du marché dans les solutions de meubles en milieu de travail

- Plus de 75 ans d'expérience dans l'industrie

- Marque reconnue dans 50 États et plusieurs marchés internationaux

Processus de fabrication complexes et expertise technologique

La complexité manufacturière de HNI nécessite des capacités technologiques avancées. La société a investi 42,3 millions de dollars dans la recherche et le développement en 2022, démontrant la sophistication technologique requise pour l'entrée du marché.

| Zone d'investissement technologique | Dépenses ($) |

|---|---|

| Dépenses de R&D | 42,300,000 |

| Inscriptions aux brevets | 23 |

Investissement important dans la conception et l'innovation

La conception et l'innovation représentent des obstacles critiques à l'entrée du marché. Les capacités de conception de Hni Corporation se reflètent dans son développement continu de produits et son portefeuille de brevets.

- 23 brevets de conception actifs à partir de 2022

- Cycle d'innovation de produit continu

- Des équipes de conception couvrant plusieurs départements spécialisés

HNI Corporation (HNI) - Porter's Five Forces: Competitive rivalry

The competitive rivalry within the office furniture sector remains intense, facing major players such as MillerKnoll across various segments. The overall Office Furniture Market size is estimated at USD 78.10 billion in 2025 globally, projected to grow at a 6.89% CAGR through 2030.

The pending acquisition of Steelcase (SCS) by HNI Corporation, valued at approximately $2.2 billion in a cash and stock transaction announced on August 4, 2025, will consolidate the market significantly. This transaction is expected to close before the end of calendar 2025.

The structure of the deal dictates that upon closing, HNI shareholders will own roughly 64% of the combined organization, while Steelcase shareholders will hold the remaining 36%. This combination anticipates generating pro forma annual revenue of approximately $5.8 billion and projected annual run-rate synergies of $120 million.

Rivalry is high, partly due to the mature nature of office furniture markets, though the U.S. market is still expected to grow from an estimated USD 17.43 billion in 2025 to USD 22.24 billion by 2030, representing a 5.0% CAGR from 2025 to 2030.

HNI Corporation is driving internal financial outperformance, confirming expectations for a fourth consecutive year of double-digit non-GAAP earnings improvement. The company explicitly projects mid-teens percent diluted non-GAAP EPS growth for the full year 2025.

Here's a look at recent non-GAAP EPS performance and outlook:

| Period | Non-GAAP Diluted EPS | Year-over-Year Change |

| Q1 2025 | $0.44 | +19% |

| Q3 2025 | $1.10 | +7% |

| Full Year 2024 (Actual) | $3.06 | +15% |

The company's competitive positioning relies on specific operational strengths:

- Brand reputation.

- Distribution network.

- Product innovation.

The expected synergies from the Steelcase acquisition, along with savings from the KII acquisition and the Mexico facility ramp-up, are expected to contribute a total of $0.75 to $0.80 to diluted non-GAAP EPS across 2025-2026.

HNI's gross debt leverage is targeted to return to the range of 1 to 1.5x within 18 to 24 months following the acquisition close, having stood at 0.9x after reducing debt by $120 million in Q3 2025.

HNI Corporation (HNI) - Porter's Five Forces: Threat of substitutes

You're looking at how external pressures could erode HNI Corporation's core business, and the threat of substitutes is definitely a major factor, especially with how work and home life have shifted.

Remote work and hybrid models are a long-term substitute for commercial office furniture. While HNI Corporation's Workplace Furnishings segment is still seeing some activity-orders were up 2% year-over-year in the third quarter of 2025, excluding certain customer pull-ins-the underlying trend is a move away from traditional, full-time office setups. Data suggests that increased space-sharing practices, up 30% since 2021 among corporate real estate executives, allow organizations to report up to 30% real-estate cost savings after reconfiguration. This dynamic puts pressure on the overall volume needed for the office furniture market, which stands at an estimated $78.10 billion in 2025. It's a big market, projected to hit $109 billion by 2030, but the need for HNI Corporation's specific product mix is being challenged by less physical space being utilized full-time.

Residential Building Products face substitution from alternative heating solutions, though HNI Corporation's hearth business seems relatively insulated for now. The modern hearth market, which includes HNI Corporation's gas, electric, and wood-burning fireplaces, is valued at approximately $2.5 billion in 2025 and is projected to grow at a Compound Annual Growth Rate (CAGR) of 5% through 2033. This suggests that while other energy sources exist, the demand for aesthetically pleasing and energy-efficient hearths remains strong, especially since the Residential Building Products segment orders grew 8% in the first quarter of 2025, even though Q3 performance was described as 'stable.'

E-commerce platforms allow for easier access to lower-cost, non-contract furniture alternatives. This is a direct threat to HNI Corporation's contract-focused sales channels. While B2B/direct sales commanded a 71.4% share of the office furniture market in 2024, the B2C online channels are rising fast, showing a 7.6% CAGR through 2030. If smaller firms or individuals furnishing home offices bypass traditional dealer networks, they often opt for less expensive, non-contract-grade items, increasing the pool of substitutes available online.

The $0.70 to $0.80 incremental Earnings Per Share (EPS) from KII synergies helps fund product differentiation. HNI Corporation continues to realize significant savings from the Kimball International (KII) acquisition integration and its Mexico facility ramp-up. These two initiatives are collectively expected to contribute between $0.75 to $0.80 to diluted non-GAAP EPS across the 2025-2026 period. This financial cushion is critical; it allows HNI Corporation to invest in higher-value products that can better withstand substitution pressure from cheaper alternatives.

High-quality, ergonomic contract furniture maintains a strong value proposition for large firms. This is HNI Corporation's defense against the low-cost threat. While the economy pricing tier still accounted for 52% of the office furniture market size in 2024, the premium furniture segment is expanding at an 8.1% CAGR through 2030. This indicates that large corporate clients, despite hybrid work, are prioritizing better, more ergonomic solutions to entice employees back to the office. HNI Corporation's Q3 2025 non-GAAP operating margin hit 10.8%, the highest for a third quarter, which reflects successful execution on profit transformation and pricing, supporting the ability to compete on quality.

- Q3 2025 Non-GAAP diluted EPS: $1.10.

- Q3 2025 Net Sales: $683.8 million.

- Workplace Furnishings Q3 2025 Net Sales: $516.9 million.

- Expected KII/Mexico Synergy EPS contribution (2025-2026): $0.75 to $0.80.

- Office Furniture Market Size (2025 Est.): $78.10 billion.

| HNI Segment/Market Area | Metric | Value/Rate | Timeframe/Context |

| Office Furniture Market | Estimated Size | $78.10 billion | 2025 |

| Office Furniture Market | Projected CAGR | 6.89% | 2025-2030 |

| Office Furniture Market (Price Tier) | Economy Tier Share | 52% | 2024 |

| Office Furniture Market (Price Tier) | Premium Furniture CAGR | 8.1% | Through 2030 |

| B2C Online Channels (Office Furniture) | CAGR | 7.6% | Through 2030 |

| Hearth Market (Residential Products) | Estimated Size | $2.5 billion | 2025 |

| Hearth Market | Projected CAGR | 5% | 2025-2033 |

| Hearth Market (Geography) | North America Share | ~60% | Current |

The ability of HNI Corporation to offset these substitution threats hinges on its internal execution, like realizing that $0.70 to $0.80 in synergy-driven EPS. Finance: draft the 13-week cash view by Friday to monitor liquidity against potential dips in commercial demand.

HNI Corporation (HNI) - Porter's Five Forces: Threat of new entrants

You're looking at HNI Corporation (HNI) and wondering how tough it is for a new player to muscle in on their turf, especially with that massive Steelcase deal pending. Honestly, the barriers to entry here are substantial, built up over decades of capital deployment and network development.

Significant capital investment is required for manufacturing and distribution scale.

To compete effectively in workplace furnishings or hearth products, a new entrant needs serious upfront cash. Think about the scale HNI operates at; their Trailing Twelve Month (TTM) Net Sales, as of Q3 2025, hit $2.6B. That kind of revenue base requires massive, efficient production capacity. HNI Corporation's own investment in physical assets shows the baseline; for the period ending March 29, 2025, their total Capital Expenditures (CapEx) were $16.3 million. This figure covers both segments, Workplace Furnishings ($11.0M) and Residential Building Products ($3.2M), plus general corporate spending ($2.0M). Furthermore, HNI is actively investing in optimization, like ramping up a new facility in Mexico, with total expected savings from that and KII synergies reaching $80-85 million through 2026. A new entrant must match or exceed this level of investment just to achieve cost parity, let alone scale.

| Metric | HNI Corporation (as of late 2025 Data) | Unit |

|---|---|---|

| Trailing Twelve Month Net Sales (TTM) | 2.6B | USD |

| Total Capital Expenditures (Q1 2025) | 16.3M | USD |

| Expected Synergy Savings (2025-2026) | 80-85M | USD |

| Steelcase Acquisition Consideration | 2.2B | USD |

Established brand loyalty and dealer networks create high distribution barriers.

Brand equity is a huge moat here. In the hearth business, HNI's brands like Heatilator, Heat & Glo, Majestic, Monessen, and Stellar are market leaders in gas and wood fireplaces. Building that level of trust takes years. Distribution is just as sticky. HNI's Hearth & Home unit sells through independent dealers, distributors, and 28 Corporation-owned installing distribution and retail outlets under the Fireside Hearth & Home brand. For the workplace segment, HNI relies on an extensive dealer network that provides localized service-something a startup simply cannot replicate overnight. The pending acquisition of Steelcase, which also has established dealer networks, only entrenches this barrier further for any potential new competitor.

The pending Steelcase merger creates an even larger, more formidable incumbent.

The announced acquisition of Steelcase Inc. by HNI Corporation is a game-changer for industry concentration. The deal valued Steelcase at approximately $2.2 billion in cash and stock. Once closed, expected by the end of calendar year 2025, the combined entity will see HNI shareholders owning approximately 64% and Steelcase shareholders owning about 36%. This consolidation means fewer, but much larger, established players dominating the market share, making it significantly harder for a new entrant to gain traction against the combined scale and complementary brand portfolios.

New entrants can easily target niche product lines or direct-to-consumer e-commerce.

To be fair, the threat isn't zero. New entrants often find success by avoiding direct confrontation with the incumbents' core, high-volume channels. You see this play out in two main areas. First, niche product lines within the Workplace Furnishings segment, perhaps highly specialized ergonomic seating or unique modular systems for micro-offices, offer an opening. Second, the direct-to-consumer (D2C) e-commerce channel remains an avenue. HNI itself uses e-commerce retailers for its Residential Building Products segment, suggesting that a digitally native brand focused purely on online sales, bypassing the traditional dealer network entirely, could find a foothold, though they'd still face HNI's established brand recognition in that space.

- Targeting specific, underserved commercial sub-markets.

- Focusing on D2C sales channels for residential products.

- Developing proprietary, highly differentiated material technology.

- Leveraging lower overhead from a purely digital sales model.

Regulatory and environmental compliance adds cost complexity for new manufacturers.

Manufacturing in the U.S. comes with a heavy compliance overhead that disproportionately affects smaller, newer firms. The total cost of federal regulations in 2022 was estimated at $3.079 trillion across the U.S. economy. For a small manufacturer, the burden is immense; environmental compliance costs alone averaged $40,700 per employee in 2022, compared to $12,500 for larger firms. New entrants must immediately budget for things like EPA's TSCA Title VI standards for composite wood materials and CPSC safety requirements for children's furniture. Navigating this complex web of rules requires specialized staff or expensive consultants, immediately inflating the initial operating expenses before a single product is sold profitably.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.