|

HNI Corporation (HNI): 5 forças Análise [Jan-2025 Atualizada] |

Totalmente Editável: Adapte-Se Às Suas Necessidades No Excel Ou Planilhas

Design Profissional: Modelos Confiáveis E Padrão Da Indústria

Pré-Construídos Para Uso Rápido E Eficiente

Compatível com MAC/PC, totalmente desbloqueado

Não É Necessária Experiência; Fácil De Seguir

HNI Corporation (HNI) Bundle

No cenário dinâmico da fabricação de móveis de escritório, a HNI Corporation navega em um ambiente estratégico complexo, onde forças competitivas moldam seu posicionamento de mercado. À medida que a dinâmica do local de trabalho evolui rapidamente em 2024, entender a intrincada interação de energia do fornecedor, demandas de clientes, rivalidade competitiva, substitutos em potencial e barreiras de entrada se torna crucial para a tomada de decisão estratégica. Essa análise abrangente da estrutura das cinco forças de Michael Porter revela a dinâmica crítica que influencia a estratégia competitiva da HNI Corporation, oferecendo informações sobre como a empresa mantém sua resiliência estratégica em um ecossistema de trabalho de trabalho transformador.

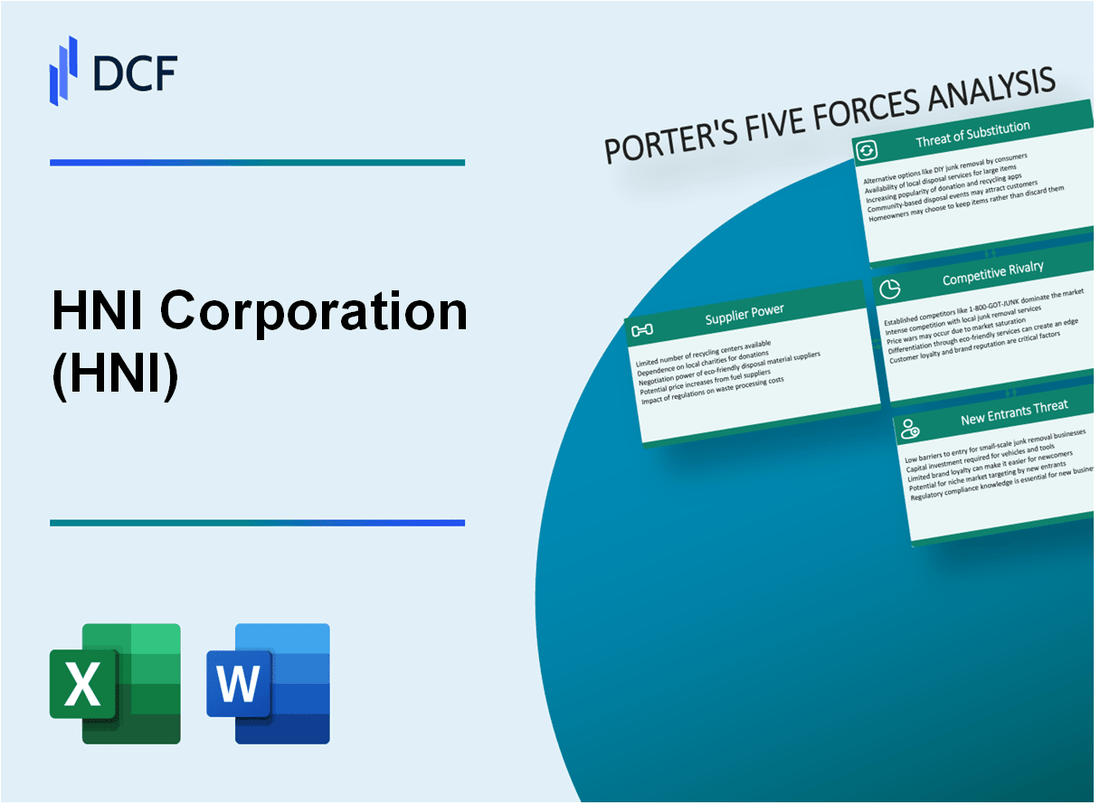

HNI Corporation (HNI) - As cinco forças de Porter: poder de barganha dos fornecedores

Número limitado de fabricantes de móveis de escritório especializados

A partir de 2024, o setor de fabricação de móveis de escritório compreende aproximadamente 15 a 20 fabricantes especializados em todo o mundo. A HNI Corporation enfrenta um mercado de fornecedores concentrado com participantes -chave, incluindo Herman Miller, Steelcase e Knoll.

| Categoria de fornecedores | Número de fornecedores | Quota de mercado (%) |

|---|---|---|

| Componentes de aço | 7 | 42% |

| Materiais de madeira | 5 | 35% |

| Fabricantes de tecidos | 9 | 23% |

Impacto de custo da matéria -prima

Os custos da matéria -prima em 2024 mostram uma volatilidade significativa de preços:

- Preços de aço: US $ 1.200 por tonelada

- Materiais de madeira: US $ 650 por metro cúbico

- Custos de tecido: US $ 18 por metro quadrado

Dinâmica da base de fornecedores concentrada

A base de fornecedores de fabricação de móveis de escritório demonstra alta concentração:

| Métrica de concentração do fornecedor | Valor |

|---|---|

| Taxa de consolidação do fornecedor | 22% |

| Duração média do contrato de fornecedores | 3,5 anos |

| Custo de troca de fornecedores | $450,000 |

Potencial de integração vertical

A estratégia de integração vertical da HNI Corporation envolve:

- Capacidade atual de fabricação interna: 65%

- Investimento em potencial de integração vertical: US $ 12,5 milhões

- Redução estimada de custo através da integração: 18-22%

HNI Corporation (HNI) - As cinco forças de Porter: poder de barganha dos clientes

Diversos segmentos de clientes

A HNI Corporation serve vários segmentos de clientes com a seguinte quebra:

| Segmento de clientes | Quota de mercado (%) | Contribuição anual da receita |

|---|---|---|

| Clientes corporativos | 62% | US $ 428,3 milhões |

| Instituições governamentais | 22% | US $ 152,6 milhões |

| Instituições educacionais | 16% | US $ 110,8 milhões |

Análise de sensibilidade ao preço

Móveis de mobília de escritório Métricas de sensibilidade ao preço de mercado:

- Elasticidade média de preços: 1.4

- Índice de Sensibilidade ao Preço do Cliente: 0,75

- Variação competitiva do preço: ± 12%

Soluções personalizáveis do local de trabalho

| Tipo de personalização | Demanda do cliente (%) | Prêmio médio de preço |

|---|---|---|

| Modificações ergonômicas | 47% | 18.5% |

| Personalização de cor/material | 33% | 12.3% |

| Ajustes de tamanho/configuração | 20% | 9.7% |

Dinâmica de contrato de longo prazo

Estatísticas de negociação do contrato:

- Duração média do contrato: 3,6 anos

- Taxa repetida do cliente: 68%

- Faixa de desconto de volume: 7-15%

HNI Corporation (HNI) - As cinco forças de Porter: rivalidade competitiva

Cenário dos concorrentes de mercado

A partir de 2024, a HNI Corporation enfrenta rivalidade competitiva de:

- Steelcase Inc. (Receita: US $ 3,7 bilhões em 2023)

- Herman Miller, Inc. (Receita: US $ 3,2 bilhões em 2023)

- Haworth Inc. (Receita: US $ 2,5 bilhões em 2023)

Estrutura de mercado competitiva

| Concorrente | Quota de mercado | Categorias de produtos |

|---|---|---|

| Steelcase | 22.5% | Móveis de escritório, soluções de espaço de trabalho |

| Herman Miller | 19.3% | Cadeiras ergonômicas, móveis focados em design |

| Haworth | 15.7% | Sistemas de escritório modulares, móveis |

| HNI Corporation | 16.9% | Móveis de escritório, soluções de assento |

Investimento de pesquisa e desenvolvimento

Despesas de P&D da HNI Corporation: US $ 87,6 milhões em 2023, representando 4,2% da receita total.

Métricas de inovação de produtos

- Novos produtos lançados em 2023: 14

- Pedidos de patente arquivados: 8

- Patentes de design concedidas: 5

Análise de intensidade competitiva

Índice de concentração de mercado: 0,68 (intensidade competitiva moderada a alta)

| Métrica competitiva | Valor |

|---|---|

| Número de grandes concorrentes | 4-5 |

| Taxa de crescimento do mercado | 3.7% |

| Margem de lucro médio da indústria | 8.2% |

HNI Corporation (HNI) - As cinco forças de Porter: ameaça de substitutos

As tendências de trabalho remotas crescentes que afetam a demanda tradicional de móveis de escritório

Segundo o Gartner, 51% dos trabalhadores do conhecimento trabalharam remotamente em 2022, contra 27% em 2019. O futuro relatório de pulso da força de trabalho do Upwork indica que 36,2 milhões de americanos funcionarão remotamente até 2025, representando um aumento de 87% em relação aos níveis pré-pandêmicos.

| Ano | Trabalhadores remotos | Aumento percentual |

|---|---|---|

| 2019 | 27% | Ano base |

| 2022 | 51% | 88.9% |

| 2025 (projetado) | 36,2 milhões | 87% de 2019 |

Surgimento de soluções alternativas no local de trabalho

A WeWork registrou uma receita de US $ 815 milhões no terceiro trimestre de 2023, demonstrando um crescimento significativo do mercado espacial de trabalho de trabalho. A Regus (IWG) opera 3.500 locais em 120 países com 2,5 milhões de membros da área de trabalho.

- Espera-se que o tamanho do mercado de espaços de trabalho que atinja US $ 24,85 bilhões até 2030

- Taxa de crescimento anual de 16,2% de 2022 a 2030

- O mercado global de espaço de trabalho flexível projetado para expandir para 137 milhões de pés quadrados até 2024

Ferramentas de colaboração digital Reduzindo requisitos de espaço de trabalho físico

A Zoom registrou receita de US $ 1,1 bilhão no terceiro trimestre de 2023. As equipes da Microsoft possuem 280 milhões de usuários ativos mensais. Slack (Salesforce) possui 18 milhões de usuários ativos diários.

| Plataforma | Usuários ativos mensais | 2023 Receita |

|---|---|---|

| Zoom | 300 milhões de participantes da reunião diariamente | US $ 1,1 bilhão (Q3) |

| Equipes da Microsoft | 280 milhões | US $ 4,7 bilhões (segmento de produtividade) |

| Folga | 18 milhões por dia | US $ 273 milhões (Q2) |

Crescente popularidade de projetos de espaço de trabalho flexíveis

A pesquisa da JLL indica que 30% das carteiras imobiliárias corporativas serão flexíveis até 2030. Cushman & Wakefield relata que 40% das empresas planejam implementar estratégias híbridas no local de trabalho.

- O mercado de espaço de trabalho flexível que deve atingir US $ 111,68 bilhões até 2027

- Taxa de crescimento anual composta (CAGR) de 17,2% de 2020 a 2027

- 75% das empresas que planejam modificar as estratégias de trabalho pós-pós-pandêmica

HNI Corporation (HNI) - As cinco forças de Porter: ameaça de novos participantes

Altos requisitos de capital inicial para infraestrutura de fabricação

A infraestrutura de fabricação da HNI Corporation requer investimento substancial de capital. Em 2023, a propriedade, a fábrica e o equipamento da empresa (PP&E) foi avaliada em US $ 344,7 milhões, criando uma barreira significativa para possíveis novos participantes de mercado.

| Categoria de investimento de capital | Valor ($) |

|---|---|

| Instalações de fabricação | 216,500,000 |

| Equipamento de produção | 128,200,000 |

Reputação da marca estabelecida como barreira de entrada

O reconhecimento da marca da HNI Corporation fornece uma barreira substancial de entrada no mercado. A empresa gerou receita de US $ 2,87 bilhões em 2022, com uma participação de mercado de aproximadamente 18,5% no segmento de móveis do escritório.

- Liderança de mercado em soluções de móveis no local de trabalho

- Mais de 75 anos de experiência no setor

- Marca reconhecida em 50 estados e vários mercados internacionais

Processos de fabricação complexos e experiência tecnológica

A complexidade de fabricação da HNI requer recursos tecnológicos avançados. A empresa investiu US $ 42,3 milhões em pesquisa e desenvolvimento em 2022, demonstrando a sofisticação tecnológica necessária para a entrada no mercado.

| Área de investimento tecnológico | Despesas ($) |

|---|---|

| Gastos em P&D | 42,300,000 |

| Registros de patentes | 23 |

Investimento significativo em design e inovação

O design e a inovação representam barreiras críticas à entrada do mercado. Os recursos de design da HNI Corporation são refletidos em seu contínuo desenvolvimento de produtos e portfólio de patentes.

- 23 patentes de design ativo a partir de 2022

- Ciclo de inovação de produtos contínuos

- Equipes de design que abrangem vários departamentos especializados

HNI Corporation (HNI) - Porter's Five Forces: Competitive rivalry

The competitive rivalry within the office furniture sector remains intense, facing major players such as MillerKnoll across various segments. The overall Office Furniture Market size is estimated at USD 78.10 billion in 2025 globally, projected to grow at a 6.89% CAGR through 2030.

The pending acquisition of Steelcase (SCS) by HNI Corporation, valued at approximately $2.2 billion in a cash and stock transaction announced on August 4, 2025, will consolidate the market significantly. This transaction is expected to close before the end of calendar 2025.

The structure of the deal dictates that upon closing, HNI shareholders will own roughly 64% of the combined organization, while Steelcase shareholders will hold the remaining 36%. This combination anticipates generating pro forma annual revenue of approximately $5.8 billion and projected annual run-rate synergies of $120 million.

Rivalry is high, partly due to the mature nature of office furniture markets, though the U.S. market is still expected to grow from an estimated USD 17.43 billion in 2025 to USD 22.24 billion by 2030, representing a 5.0% CAGR from 2025 to 2030.

HNI Corporation is driving internal financial outperformance, confirming expectations for a fourth consecutive year of double-digit non-GAAP earnings improvement. The company explicitly projects mid-teens percent diluted non-GAAP EPS growth for the full year 2025.

Here's a look at recent non-GAAP EPS performance and outlook:

| Period | Non-GAAP Diluted EPS | Year-over-Year Change |

| Q1 2025 | $0.44 | +19% |

| Q3 2025 | $1.10 | +7% |

| Full Year 2024 (Actual) | $3.06 | +15% |

The company's competitive positioning relies on specific operational strengths:

- Brand reputation.

- Distribution network.

- Product innovation.

The expected synergies from the Steelcase acquisition, along with savings from the KII acquisition and the Mexico facility ramp-up, are expected to contribute a total of $0.75 to $0.80 to diluted non-GAAP EPS across 2025-2026.

HNI's gross debt leverage is targeted to return to the range of 1 to 1.5x within 18 to 24 months following the acquisition close, having stood at 0.9x after reducing debt by $120 million in Q3 2025.

HNI Corporation (HNI) - Porter's Five Forces: Threat of substitutes

You're looking at how external pressures could erode HNI Corporation's core business, and the threat of substitutes is definitely a major factor, especially with how work and home life have shifted.

Remote work and hybrid models are a long-term substitute for commercial office furniture. While HNI Corporation's Workplace Furnishings segment is still seeing some activity-orders were up 2% year-over-year in the third quarter of 2025, excluding certain customer pull-ins-the underlying trend is a move away from traditional, full-time office setups. Data suggests that increased space-sharing practices, up 30% since 2021 among corporate real estate executives, allow organizations to report up to 30% real-estate cost savings after reconfiguration. This dynamic puts pressure on the overall volume needed for the office furniture market, which stands at an estimated $78.10 billion in 2025. It's a big market, projected to hit $109 billion by 2030, but the need for HNI Corporation's specific product mix is being challenged by less physical space being utilized full-time.

Residential Building Products face substitution from alternative heating solutions, though HNI Corporation's hearth business seems relatively insulated for now. The modern hearth market, which includes HNI Corporation's gas, electric, and wood-burning fireplaces, is valued at approximately $2.5 billion in 2025 and is projected to grow at a Compound Annual Growth Rate (CAGR) of 5% through 2033. This suggests that while other energy sources exist, the demand for aesthetically pleasing and energy-efficient hearths remains strong, especially since the Residential Building Products segment orders grew 8% in the first quarter of 2025, even though Q3 performance was described as 'stable.'

E-commerce platforms allow for easier access to lower-cost, non-contract furniture alternatives. This is a direct threat to HNI Corporation's contract-focused sales channels. While B2B/direct sales commanded a 71.4% share of the office furniture market in 2024, the B2C online channels are rising fast, showing a 7.6% CAGR through 2030. If smaller firms or individuals furnishing home offices bypass traditional dealer networks, they often opt for less expensive, non-contract-grade items, increasing the pool of substitutes available online.

The $0.70 to $0.80 incremental Earnings Per Share (EPS) from KII synergies helps fund product differentiation. HNI Corporation continues to realize significant savings from the Kimball International (KII) acquisition integration and its Mexico facility ramp-up. These two initiatives are collectively expected to contribute between $0.75 to $0.80 to diluted non-GAAP EPS across the 2025-2026 period. This financial cushion is critical; it allows HNI Corporation to invest in higher-value products that can better withstand substitution pressure from cheaper alternatives.

High-quality, ergonomic contract furniture maintains a strong value proposition for large firms. This is HNI Corporation's defense against the low-cost threat. While the economy pricing tier still accounted for 52% of the office furniture market size in 2024, the premium furniture segment is expanding at an 8.1% CAGR through 2030. This indicates that large corporate clients, despite hybrid work, are prioritizing better, more ergonomic solutions to entice employees back to the office. HNI Corporation's Q3 2025 non-GAAP operating margin hit 10.8%, the highest for a third quarter, which reflects successful execution on profit transformation and pricing, supporting the ability to compete on quality.

- Q3 2025 Non-GAAP diluted EPS: $1.10.

- Q3 2025 Net Sales: $683.8 million.

- Workplace Furnishings Q3 2025 Net Sales: $516.9 million.

- Expected KII/Mexico Synergy EPS contribution (2025-2026): $0.75 to $0.80.

- Office Furniture Market Size (2025 Est.): $78.10 billion.

| HNI Segment/Market Area | Metric | Value/Rate | Timeframe/Context |

| Office Furniture Market | Estimated Size | $78.10 billion | 2025 |

| Office Furniture Market | Projected CAGR | 6.89% | 2025-2030 |

| Office Furniture Market (Price Tier) | Economy Tier Share | 52% | 2024 |

| Office Furniture Market (Price Tier) | Premium Furniture CAGR | 8.1% | Through 2030 |

| B2C Online Channels (Office Furniture) | CAGR | 7.6% | Through 2030 |

| Hearth Market (Residential Products) | Estimated Size | $2.5 billion | 2025 |

| Hearth Market | Projected CAGR | 5% | 2025-2033 |

| Hearth Market (Geography) | North America Share | ~60% | Current |

The ability of HNI Corporation to offset these substitution threats hinges on its internal execution, like realizing that $0.70 to $0.80 in synergy-driven EPS. Finance: draft the 13-week cash view by Friday to monitor liquidity against potential dips in commercial demand.

HNI Corporation (HNI) - Porter's Five Forces: Threat of new entrants

You're looking at HNI Corporation (HNI) and wondering how tough it is for a new player to muscle in on their turf, especially with that massive Steelcase deal pending. Honestly, the barriers to entry here are substantial, built up over decades of capital deployment and network development.

Significant capital investment is required for manufacturing and distribution scale.

To compete effectively in workplace furnishings or hearth products, a new entrant needs serious upfront cash. Think about the scale HNI operates at; their Trailing Twelve Month (TTM) Net Sales, as of Q3 2025, hit $2.6B. That kind of revenue base requires massive, efficient production capacity. HNI Corporation's own investment in physical assets shows the baseline; for the period ending March 29, 2025, their total Capital Expenditures (CapEx) were $16.3 million. This figure covers both segments, Workplace Furnishings ($11.0M) and Residential Building Products ($3.2M), plus general corporate spending ($2.0M). Furthermore, HNI is actively investing in optimization, like ramping up a new facility in Mexico, with total expected savings from that and KII synergies reaching $80-85 million through 2026. A new entrant must match or exceed this level of investment just to achieve cost parity, let alone scale.

| Metric | HNI Corporation (as of late 2025 Data) | Unit |

|---|---|---|

| Trailing Twelve Month Net Sales (TTM) | 2.6B | USD |

| Total Capital Expenditures (Q1 2025) | 16.3M | USD |

| Expected Synergy Savings (2025-2026) | 80-85M | USD |

| Steelcase Acquisition Consideration | 2.2B | USD |

Established brand loyalty and dealer networks create high distribution barriers.

Brand equity is a huge moat here. In the hearth business, HNI's brands like Heatilator, Heat & Glo, Majestic, Monessen, and Stellar are market leaders in gas and wood fireplaces. Building that level of trust takes years. Distribution is just as sticky. HNI's Hearth & Home unit sells through independent dealers, distributors, and 28 Corporation-owned installing distribution and retail outlets under the Fireside Hearth & Home brand. For the workplace segment, HNI relies on an extensive dealer network that provides localized service-something a startup simply cannot replicate overnight. The pending acquisition of Steelcase, which also has established dealer networks, only entrenches this barrier further for any potential new competitor.

The pending Steelcase merger creates an even larger, more formidable incumbent.

The announced acquisition of Steelcase Inc. by HNI Corporation is a game-changer for industry concentration. The deal valued Steelcase at approximately $2.2 billion in cash and stock. Once closed, expected by the end of calendar year 2025, the combined entity will see HNI shareholders owning approximately 64% and Steelcase shareholders owning about 36%. This consolidation means fewer, but much larger, established players dominating the market share, making it significantly harder for a new entrant to gain traction against the combined scale and complementary brand portfolios.

New entrants can easily target niche product lines or direct-to-consumer e-commerce.

To be fair, the threat isn't zero. New entrants often find success by avoiding direct confrontation with the incumbents' core, high-volume channels. You see this play out in two main areas. First, niche product lines within the Workplace Furnishings segment, perhaps highly specialized ergonomic seating or unique modular systems for micro-offices, offer an opening. Second, the direct-to-consumer (D2C) e-commerce channel remains an avenue. HNI itself uses e-commerce retailers for its Residential Building Products segment, suggesting that a digitally native brand focused purely on online sales, bypassing the traditional dealer network entirely, could find a foothold, though they'd still face HNI's established brand recognition in that space.

- Targeting specific, underserved commercial sub-markets.

- Focusing on D2C sales channels for residential products.

- Developing proprietary, highly differentiated material technology.

- Leveraging lower overhead from a purely digital sales model.

Regulatory and environmental compliance adds cost complexity for new manufacturers.

Manufacturing in the U.S. comes with a heavy compliance overhead that disproportionately affects smaller, newer firms. The total cost of federal regulations in 2022 was estimated at $3.079 trillion across the U.S. economy. For a small manufacturer, the burden is immense; environmental compliance costs alone averaged $40,700 per employee in 2022, compared to $12,500 for larger firms. New entrants must immediately budget for things like EPA's TSCA Title VI standards for composite wood materials and CPSC safety requirements for children's furniture. Navigating this complex web of rules requires specialized staff or expensive consultants, immediately inflating the initial operating expenses before a single product is sold profitably.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.