|

Kotak Mahindra Bank Limited (KOTAKBANK.NS): BCG Matrix |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Kotak Mahindra Bank Limited (KOTAKBANK.NS) Bundle

In the fast-paced world of finance, understanding how different segments of a business perform is crucial for investors and analysts alike. Kotak Mahindra Bank Limited, a key player in India's banking landscape, offers a fascinating case study through the lens of the Boston Consulting Group Matrix. With its evolving strategies across various segments, this analysis explores the bank's Stars, Cash Cows, Dogs, and Question Marks, revealing where the opportunities and challenges lie in its business model. Read on to discover how Kotak Mahindra Bank is navigating its diverse portfolio.

Background of Kotak Mahindra Bank Limited

Kotak Mahindra Bank Limited, established in 1985, is one of India’s leading private sector banks. Originally founded as a finance company, it received a banking license from the Reserve Bank of India (RBI) in 2003. Over the years, Kotak has expanded its services substantially, offering a wide array of financial products, including retail banking, corporate banking, insurance, and asset management.

As of the fiscal year 2023, Kotak Mahindra Bank reported a total asset base of approximately INR 3.5 trillion, making it one of the largest private banks in India. The bank’s focus on technology and digital transformation has positioned it strategically, attracting a significant number of retail customers. By March 2023, Kotak Mahindra Bank had over 1,600 branches and 2,600 ATMs across the country.

Financial performance has been robust. In the fiscal year ending March 2023, the bank posted a net profit of INR 39.6 billion, representing a year-on-year growth of 20%. This growth is attributed to a steady increase in net interest income and a disciplined approach to managing non-performing assets (NPAs), which stood at 2.25% of total loans.

Kotak’s customer-centric initiatives and multiple digital offerings have helped enhance customer engagement, with the bank serving more than 29 million customers as of March 2023. Additionally, the bank has maintained a strong capital adequacy ratio, above the regulatory requirement, ensuring financial stability and a strong foundation for future growth.

With a vision of becoming the most trusted and preferred bank, Kotak Mahindra Bank continues to expand its footprint in both urban and rural markets, adapting to the evolving financial landscape and customer needs. The bank aims to leverage technology to streamline operations and improve customer experience further.

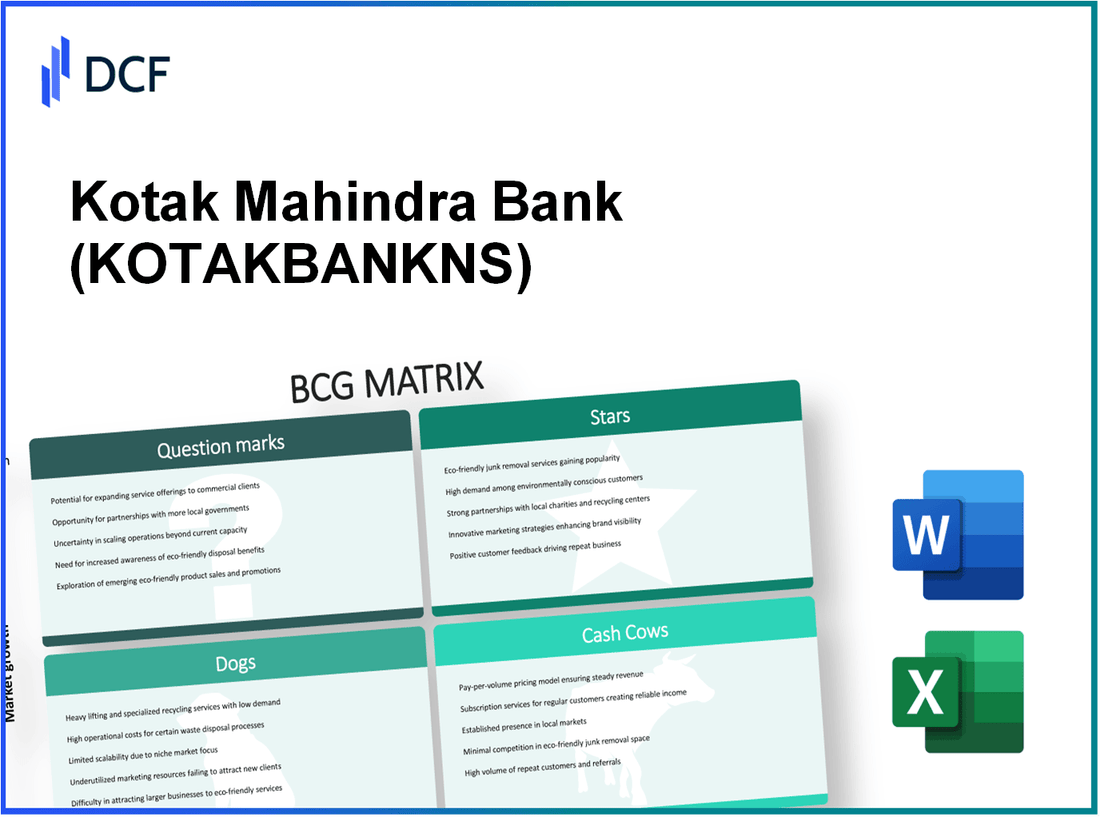

Kotak Mahindra Bank Limited - BCG Matrix: Stars

Retail Banking Services

Kotak Mahindra Bank's retail banking services have seen significant growth, with the bank reporting a retail loan book of approximately ₹2.73 trillion as of Q2 FY2023. The bank has a market share of about 8.3% in the Indian retail banking segment, making it one of the leaders in this sector. The bank's focus on securing a robust customer base has resulted in a sustained year-on-year growth rate of approximately 20% in retail asset growth.

Digital Banking Initiatives

Kotak Mahindra Bank has heavily invested in digital banking initiatives, which have driven substantial customer engagement and retention. The bank recorded over 40 million mobile app downloads for the Kotak Mobile Banking app and reported a remarkable increase in digital transaction volumes. As of Q2 FY2023, digital transactions accounted for about 93% of the total transactions, leading to a reduction in branch visits by 60% over the past year. This shift contributes to lower operational costs while catering to a growing tech-savvy customer base.

Wealth Management Services

The wealth management segment of Kotak Mahindra Bank has emerged as a strong performer, with Assets Under Management (AUM) reaching approximately ₹2.65 trillion as of FY2023. The bank's strategic focus on high-net-worth individuals (HNWIs) has resulted in a client growth rate of around 25% annually. Additionally, Kotak's wealth management services have reported a net profit margin of about 30%, reflecting the high profitability of this business unit.

| Business Segment | Key Metrics | Recent Performance |

|---|---|---|

| Retail Banking Services | Retail Loan Book: ₹2.73 Trillion | YoY Growth: 20% |

| Digital Banking Initiatives | Mobile App Downloads: 40 Million | Digital Transactions: 93% of Total |

| Wealth Management Services | AUM: ₹2.65 Trillion | Client Growth Rate: 25% |

Kotak Mahindra Bank Limited - BCG Matrix: Cash Cows

Kotak Mahindra Bank Limited has established a strong presence in various segments of the financial market. Among its offerings, certain products have emerged as Cash Cows due to their high market share and significant cash generation capabilities. This section explores the primary Cash Cows of Kotak Mahindra Bank: Home Loans, Savings and Fixed Deposit Accounts, and Insurance Products.

Home Loans

Home loans represent a significant segment for Kotak Mahindra Bank, capturing a considerable market share in the Indian housing finance sector. As of FY 2023, Kotak Mahindra Bank's home loan portfolio stood at approximately ₹1.03 trillion, marking a growth of 20% year-on-year. The bank has achieved a market share of about 6.5% in the home loan segment.

With a gross NPA ratio of 1.52% in the housing loan segment, this indicates effective risk management. Additionally, the loan-to-value ratio stands at 75%, reflecting the bank's cautious lending practices.

Savings and Fixed Deposit Accounts

The savings and fixed deposit accounts offered by Kotak Mahindra Bank are crucial in driving deposits and liquidity. As of Q2 FY 2023, the total customer deposits reached approximately ₹3.8 trillion, with savings accounts contributing about ₹1.7 trillion and fixed deposits around ₹1.2 trillion.

The bank reported an average interest rate of 3.5% for savings accounts, which remains competitive in the market. The fixed deposit segment has showcased a maturity profile with an average interest rate of 6.5%, attracting both retail and corporate clients.

| Product Type | Portfolio Size (₹ Trillion) | Market Share (%) | Average Interest Rate (%) | Growth YoY (%) |

|---|---|---|---|---|

| Home Loans | 1.03 | 6.5 | - | 20 |

| Savings Accounts | 1.7 | - | 3.5 | - |

| Fixed Deposits | 1.2 | - | 6.5 | - |

Insurance Products

Kotak Mahindra Bank offers a range of insurance products through its subsidiary, Kotak Life Insurance. The insurance segment has seen substantial growth, with a total premium income reported at approximately ₹10,500 crore for the fiscal year 2023. This places Kotak Life Insurance among the top five private life insurers in India with a market share of 6.1%.

Kotak Mahindra Bank has reported a claim settlement ratio of 97%, reflecting its commitment to customer satisfaction. The insurance products not only provide significant cash flow but also enhance customer retention, contributing to the overall profitability of the bank.

In summary, Kotak Mahindra Bank's Cash Cows—Home Loans, Savings, and Fixed Deposit Accounts, along with Insurance Products—play an essential role in maintaining the bank's financial stability and growth trajectory. These segments generate consistent cash flow that supports ongoing operational investments and strategic initiatives.

Kotak Mahindra Bank Limited - BCG Matrix: Dogs

Within the context of Kotak Mahindra Bank Limited, certain segments can be classified as 'Dogs,' indicating low growth rates and low market shares. This classification is essential for understanding where resources may be underperforming and potentially wasting capital.

Overseas Banking Operations

Kotak Mahindra Bank has made attempts to expand its international operations; however, this segment has not gained substantial traction. As reported in their latest financial statements, the overseas banking operations contributed approximately ₹1,000 crore to total revenues, which represents less than 5% of the bank's overall earnings.

The market share in overseas territories remains minimal, with Kotak holding less than 1% in several international markets. This limited presence in the global banking landscape reflects not only a lack of growth but also difficulty in navigating competitive environments, thereby categorizing this area as a 'Dog.'

Furthermore, operational challenges, including compliance with varying regulations and the cost of maintaining international branches, have contributed to stagnant growth in this segment. The bank faced operational losses in certain geographies amounting to approximately ₹250 crore, highlighting the financial strain and low return on investment.

Legacy IT Infrastructure

Kotak Mahindra Bank's reliance on legacy IT systems has impeded its agility and ability to innovate. The bank has invested around ₹500 crore annually in maintaining this outdated infrastructure. Despite these investments, the segment has not yielded significant growth, with IT operations contributing only 2% to the overall revenue streams.

The ongoing costs associated with these legacy systems include maintenance fees and the need for specialized personnel, leading to an estimated operational expenditure of ₹300 crore per year. This high expenditure against minimal output places this aspect firmly within the 'Dog' category.

| Segment | Contribution to Revenue (₹ Crore) | Market Share (%) | Operational Losses (₹ Crore) | Annual Maintenance Cost (₹ Crore) |

|---|---|---|---|---|

| Overseas Banking Operations | 1,000 | 1 | 250 | N/A |

| Legacy IT Infrastructure | 500 | 2 | N/A | 300 |

In summary, both the overseas banking operations and legacy IT infrastructure of Kotak Mahindra Bank stand as clear representations of 'Dogs' within their business model, demonstrating low growth opportunities coupled with low market share. These segments act as cash traps, requiring strategic evaluations for potential divestiture or reallocation of resources for more profitable ventures.

Kotak Mahindra Bank Limited - BCG Matrix: Question Marks

Kotak Mahindra Bank has several segments within its operations that can be classified as Question Marks. These segments are experiencing high growth potential but currently hold a low market share. The following outlines the areas where Kotak Mahindra Bank is focusing for strategic growth.

Microfinance Services

The microfinance services sector is characterized by rapidly growing demand, particularly in rural and semi-urban areas of India. As of FY2023, Kotak Mahindra Bank's microfinance portfolio, through its subsidiary Kotak Mahindra Bank (NBFC), reported a loan book size of approximately ₹5,000 crore. However, this represents only about 2% of the total microfinance market in India, valued at approximately ₹2.5 lakh crore.

This sector is crucial as the overall growth rate for microfinance is expected to reach 25% CAGR over the next five years. Kotak needs to invest significantly in marketing and distribution to enhance its presence and capture a larger share of this burgeoning market.

SME Banking Solutions

Small and Medium Enterprises (SMEs) are a vital segment for growth. As of Q2 FY2023, Kotak Mahindra Bank's SME banking division had a loan book of around ₹20,000 crore, which is approximately 5% of the total SME financing market, estimated at ₹40 lakh crore.

The SME sector is projected to grow at 17% annually, indicating a robust opportunity for Kotak. The bank's current market penetration is limited, which necessitates focusing on innovative financing solutions and aggressive marketing strategies to capture this growth.

Corporate Banking Expansion

The Corporate Banking sector is another area of interest for Kotak Mahindra Bank, with a reported corporate loan book of about ₹1.5 lakh crore as of FY2023. This represents approximately 8% of the total corporate lending market in India, which stands at around ₹19 lakh crore.

Given the projected growth rate for corporate loans is about 12% CAGR, it is evident that expansion in this sector can yield significant returns if Kotak increases its market share. The current strategy is to strengthen client relationships and enhance service offerings to harness this potential.

| Segment | Current Loan Book Size | Market Share | Total Market Size | Expected Growth Rate (CAGR) |

|---|---|---|---|---|

| Microfinance Services | ₹5,000 crore | 2% | ₹2.5 lakh crore | 25% |

| SME Banking Solutions | ₹20,000 crore | 5% | ₹40 lakh crore | 17% |

| Corporate Banking Expansion | ₹1.5 lakh crore | 8% | ₹19 lakh crore | 12% |

Kotak Mahindra Bank's focus on these Question Mark segments reveals the potential for significant growth if the bank strategically invests and markets these areas effectively. Failing to increase market share in these high-growth sectors may result in these units becoming less viable for the bank's overall portfolio.

Kotak Mahindra Bank Limited showcases a dynamic portfolio through the lens of the BCG Matrix, balancing its robust stars and cash cows with speculative question marks and underperforming dogs. The bank's success hinges on its ability to nurture its stars, optimize cash cows, and transform question marks into future leaders while mitigating the challenges posed by its legacy operations.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.