|

Citi Trends, Inc. (CTRN): 5 Analyse des forces [Jan-2025 Mis à jour] |

Entièrement Modifiable: Adapté À Vos Besoins Dans Excel Ou Sheets

Conception Professionnelle: Modèles Fiables Et Conformes Aux Normes Du Secteur

Pré-Construits Pour Une Utilisation Rapide Et Efficace

Compatible MAC/PC, entièrement débloqué

Aucune Expertise N'Est Requise; Facile À Suivre

Citi Trends, Inc. (CTRN) Bundle

Dans le monde dynamique de la mode de réduction urbaine, Citi Trends, Inc. (CTRN) navigue dans un paysage de vente au détail complexe où la survie dépend de la compréhension stratégique des forces du marché. En disséquant le cadre des cinq forces de Michael Porter, nous dévoilons la dynamique concurrentielle complexe qui façonne le positionnement stratégique de l'entreprise, des négociations des fournisseurs aux préférences des clients, révélant les défis et opportunités critiques qui définissent la stratégie compétitive des tendances Citi en 2024.

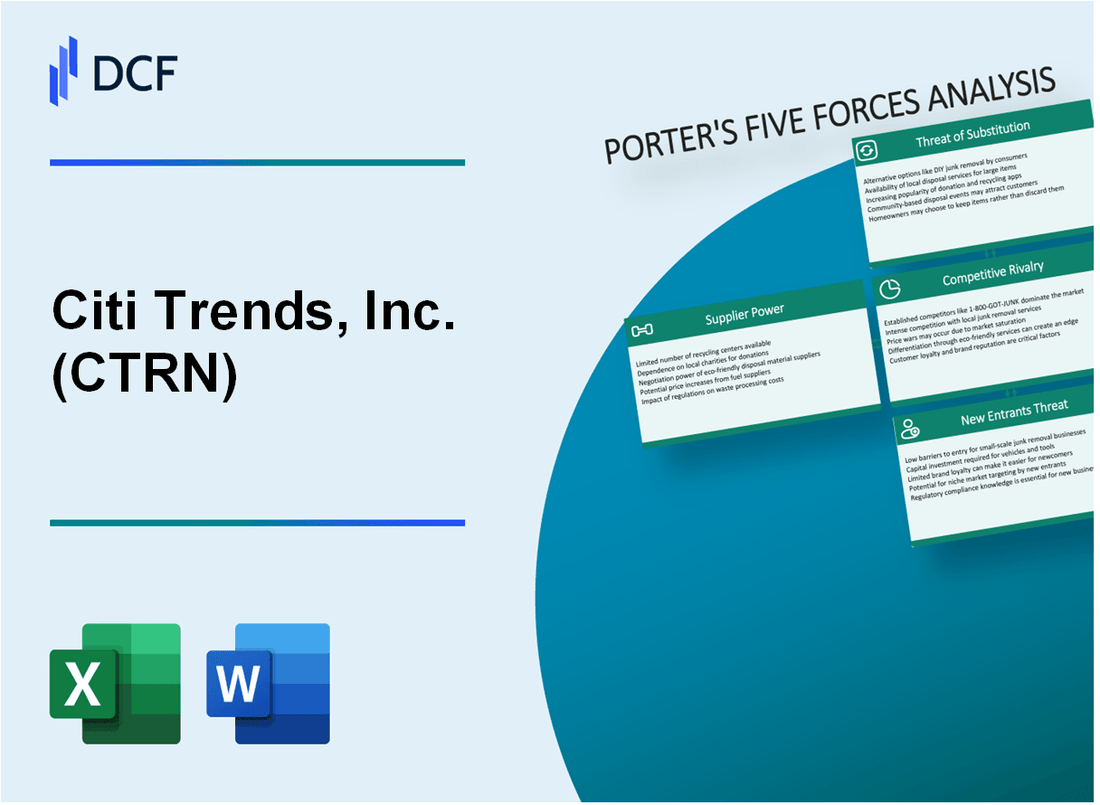

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Bargaining Power des fournisseurs

Nombre limité de fournisseurs de mode et de vêtements urbains

En 2024, Citi tend des sources d'environ 87 fournisseurs internationaux uniques, avec 73% concentrés en Asie. Les 5 principaux fournisseurs représentent 42% de l'approvisionnement total de marchandises.

Concentration de base du fournisseur

| Région du fournisseur | Pourcentage de l'approvisionnement total | Nombre de fournisseurs |

|---|---|---|

| Asie | 73% | 64 fournisseurs |

| Amérique centrale | 18% | 15 fournisseurs |

| États-Unis | 9% | 8 fournisseurs |

Dépendances internationales de fabrication

- La Chine représente 48% de la base totale des fournisseurs

- Le Vietnam représente 22% des fournisseurs internationaux

- Le Bangladesh contribue 15% de la fabrication de vêtements

Risques de perturbation de la chaîne d'approvisionnement

En 2023, les perturbations de la chaîne d'approvisionnement ont abouti à 4,2 millions de dollars des dépenses de logistique et d'approvisionnement supplémentaires pour les tendances Citi.

FLUCUATIONS PRIX PRIX

Les prix du coton ont fluctué entre 0,68 $ et 0,92 $ la livre en 2023, ce qui concerne la dynamique de négociation des fournisseurs et les structures de coûts des produits.

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Bargaining Power of Clients

Marché cible sensible aux prix

Citi Trends sert un marché cible avec un revenu médian des ménages de 41 512 $ dans les zones urbaines à partir de 2023. La clientèle se compose principalement de consommateurs afro-américains et hispaniques dans les quartiers urbains à faible revenu.

| Client démographique | Pourcentage | Dépenses moyennes |

|---|---|---|

| Consommateurs afro-américains | 58% | 127 $ par transaction |

| Consommateurs hispaniques | 22% | 112 $ par transaction |

| Autres données démographiques | 20% | 98 $ par transaction |

Élasticité-prix du client

Le segment de vente au détail de mode à prix réduit montre une sensibilité élevée aux prix avec 67% des clients indiquant le prix comme facteur de décision d'achat principal.

- 68% des clients comparent les prix de plusieurs détaillants

- 52% disposé à changer de marques pour 10 à 15% de différence de prix

- Indice moyen de sensibilité aux prix: 0,73

Préférences de vêtements à la mode abordables

Les prix moyens de vêtements de Citi Trends des Tendances varient de 12,99 $ à 39,99 $, qui s'adressent aux consommateurs soucieux du budget.

| Catégorie de vêtements | Prix moyen | Préférence du client |

|---|---|---|

| Vêtements décontractés pour hommes | $24.50 | Part de marché de 42% |

| Vêtements pour femmes | $29.99 | Part de marché de 35% |

| Vêtements pour enfants | $19.99 | 23% de part de marché |

Dynamique de fidélité à la marque

Urban démographique démontre une fidélité modérée de la marque avec 43% de taux client répété en 2023.

- Taux de rétention de la clientèle: 43%

- Fréquence d'achat moyenne: 2,7 fois par an

- Participation du programme de fidélité: 31% de la clientèle

Attentes de magasinage numérique

Les ventes en ligne représentaient 12,4% des revenus totaux en 2023, avec une augmentation de l'engagement numérique.

| Métrique numérique | Performance de 2023 |

|---|---|

| Revenus de commerce électronique | 47,3 millions de dollars |

| Téléchargements d'applications mobiles | 276,000 |

| Taux de conversion des clients en ligne | 3.6% |

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Rivalité compétitive

Analyse du paysage concurrentiel

En 2024, Citi Trends fait face à une concurrence intense dans le segment de vente au détail avec les principales mesures compétitives suivantes:

| Concurrent | Part de marché | Revenus annuels | Comptage des magasins |

|---|---|---|---|

| Magasins Ross | 15.3% | 15,1 milliards de dollars | 1 790 magasins |

| TJ Maxx | 12.7% | 13,6 milliards de dollars | 1 270 magasins |

| Tendances de Citi | 0.8% | 228,4 millions de dollars | 573 magasins |

Concentration du marché régional

Citi Trends maintient une présence concentrée dans le sud-est des États-Unis avec la rupture régionale suivante:

- Géorgie: 87 magasins

- Floride: 62 magasins

- Caroline du Sud: 45 magasins

- Alabama: 39 magasins

Défis de marge bénéficiaire

Les dynamiques concurrentielles actuelles entraînent des performances financières difficiles:

| Métrique | Valeur des tendances Citi | Moyenne de l'industrie |

|---|---|---|

| Marge brute | 36.2% | 40.5% |

| Marge bénéficiaire nette | 2.1% | 3.7% |

Stratégies de différenciation compétitive

Zones de mise au point de différenciation clé:

- Mode urbain ciblant les consommateurs afro-américains

- Stratégie de tarification compétitive

- Sélection localisée des marchandises

Citi Trends, Inc. (CTRN) - Five Forces de Porter: menace de substituts

Plateformes de commerce électronique en ligne offrant des prix similaires

Les ventes de vêtements en ligne d'Amazon ont atteint 31,5 milliards de dollars en 2022. Le chiffre d'affaires en ligne de Walmart était de 11,2 milliards de dollars la même année. Les ventes de mode numérique de Target ont totalisé 7,6 milliards de dollars.

| Plate-forme de commerce électronique | Revenus de vêtements en ligne 2022 |

|---|---|

| Amazone | 31,5 milliards de dollars |

| Walmart | 11,2 milliards de dollars |

| Cible | 7,6 milliards de dollars |

Marques de mode rapide offrant des alternatives à la mode

Les revenus mondiaux de Shein ont atteint 22,7 milliards de dollars en 2022. Fashion Nova a généré 750 millions de dollars de revenus annuels pour la même période.

Croissance du marché secondaire et d'épargne

Le marché mondial des vêtements d'occasion était évalué à 177 milliards de dollars en 2022. Thredup a projeté le marché pour atteindre 218 milliards de dollars d'ici 2026.

| Segment de marché | Valeur en 2022 | Valeur projetée d'ici 2026 |

|---|---|---|

| Marché de vêtements d'occasion | 177 milliards de dollars | 218 milliards de dollars |

Plates-formes de magasinage numériques

Les ventes de commerce mobile ont atteint 359,3 milliards de dollars en 2021. Le commerce électronique représentait 22,3% du total des ventes au détail en 2022.

Services de vêtements basés sur l'abonnement

Stitch Fix a déclaré 2,1 milliards de dollars de revenus pour 2022. Loyer la piste a généré 267,4 millions de dollars de revenus annuels.

| Service d'abonnement | Revenu annuel 2022 |

|---|---|

| Fixation | 2,1 milliards de dollars |

| Louer la piste | 267,4 millions de dollars |

Risques de substitution compétitive

- Les plateformes en ligne offrent des prix inférieurs de 15 à 30% par rapport à la vente au détail physique

- Les marques de mode rapide fournissent des produits à tendance à 40% de coût inférieur

- Le marché d'occasion augmente à 16% du taux composé annuel

Citi Trends, Inc. (CTRN) - Five Forces de Porter: menace de nouveaux entrants

Exigences de capital dans la mode à moindre coût

Capital de démarrage initial pour une entreprise de vente au détail de mode à prix réduit: 250 000 $ - 500 000 $

| Catégorie d'investissement | Coût estimé |

|---|---|

| Bail de magasin | $50,000 - $75,000 |

| Inventaire initial | $100,000 - $200,000 |

| Assemblées de magasin | $30,000 - $50,000 |

| Infrastructure numérique | $25,000 - $50,000 |

Barrières de reconnaissance de la marque

Citi Trends Market Share: 12,3% dans le segment de la mode de réduction urbaine

Défis de gestion de la chaîne d'approvisionnement

- Cycle de négociation moyen des fournisseurs: 4-6 mois

- Quantités de commande minimales: 5 000 unités par ligne de produit

- Coûts de coordination logistique: 75 000 $ - 125 000 $ par an

Coûts d'infrastructure de vente au détail numérique

Développement de la plate-forme de commerce électronique: 75 000 $ - 150 000 $

Consolidation de la mode de réduction urbaine

| Année | Taux de consolidation du marché |

|---|---|

| 2022 | 7.2% |

| 2023 | 9.5% |

| 2024 (projeté) | 11.3% |

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Competitive rivalry

You're analyzing a sector where every dollar counts, and the competition for the value-conscious shopper is fierce. The competitive rivalry within the off-price sector is, frankly, extremely high as of late 2025. This segment is thriving, which only draws more aggressive tactics from established players.

Direct competition comes from national giants that have massive scale and deep sourcing power. We're talking about The TJX Companies, which operates T.J. Maxx and Marshalls, and Burlington Stores, Inc. These competitors are actively expanding their physical footprints, which puts pressure on Citi Trends, Inc.'s market share. For instance, as of the end of second-quarter fiscal 2026 (which ended August 2, 2025), The TJX Companies operated 5,134 stores globally. Burlington Stores, Inc. executed 23 net new store additions in its second quarter of fiscal 2025, bringing its fleet to 1,138 locations at that quarter-end.

The overall off-price market size itself confirms the battleground's value: it is projected to reach \$372.46 billion in 2025. That's a huge pool of dollars everyone is fighting over.

Here's a quick look at how the major players are positioning their physical presence:

| Retailer | Store Count (Latest Reported as of Mid-2025) | Recent Comp Sales Growth Example |

|---|---|---|

| The TJX Companies (Marmaxx) | 5,134 (Global as of Q2 FY2026) | Comp sales rose 5% in Q3 2025 |

| Burlington Stores, Inc. | 1,138 (U.S. as of Q2 FY2025) | Comp sales growth of 1% in Q3 2025 |

| Citi Trends, Inc. (CTRN) | 591 (As of May 3, 2025) | Comp sales growth of 9.6% in Q2 2025 |

Still, Citi Trends, Inc. maintains a unique, defensible niche. It is, by its own description, the only off-price retailer specifically focused on the African American consumer. This targeted approach allows for a deep understanding of style preferences and budgetary needs within that core demographic. In the past, this core customer base was described as predominantly African American and Latinx households, representing about 84% of the customer base, with a median household income in the range of \$35,000 - \$55,000. This specialization is a key differentiator against the broader appeal of TJX Companies and Burlington Stores.

The positive momentum from this focused strategy is reflected in the financial guidance, showing a positive turnaround in what is clearly a tough, competitive market. The company's full year 2025 EBITDA is expected to be in the range of \$7 million to \$11 million. That's a significant swing when you look at the prior year's performance, which included an Adjusted EBITDA loss of \$18.0 million in Q2 2024 or a full-year Adjusted EBITDA loss of \$14.2 million for fiscal 2024.

The competitive pressures manifest in several ways for Citi Trends, Inc.:

- Direct comparison on comp sales against larger rivals.

- Need to maintain inventory freshness against giants with bigger buying power.

- Vulnerability of its core customer base to macro pressures like inflation.

- The necessity to continually reinforce its cultural relevance.

The success of the strategy is evident in recent operational metrics:

- Q2 2025 Comparable Store Sales Growth was 9.2%.

- Q1 2025 Comparable Store Sales Growth reached 9.9%.

- Gross Margin Rate for Q2 2025 climbed to 40.0%.

The rivalry is intense, but Citi Trends, Inc.'s niche focus provides a specific buffer against the broad market competition.

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Threat of substitutes

You're analyzing the competitive forces facing Citi Trends, Inc. as we head into late 2025, and the threat from substitutes is definitely a key area to watch. Honestly, the sheer variety of ways a customer can spend their apparel dollar outside of a traditional off-price store is growing more complex every quarter.

The threat from online fast fashion brands and general e-commerce platforms is assessed as moderate to high. These digital-native competitors are agile, trend-focused, and often have lower overheads, which pressures the value proposition of brick-and-mortar players like Citi Trends, Inc. For context, the broader US eCommerce sales are projected to hit $1.29 trillion by the end of 2025.

The shift in how consumers shop for value is clear when you look at the off-price segment itself. Online sales are the fastest-growing part of that market, accounting for approximately 30% of total off-price sales back in 2023. While we don't have the final 2025 figure yet, the trend suggests continued digital migration, even for value-seeking customers.

Here's a quick look at the scale of the competing segments:

| Substitute Category | Relevant Metric/Value | Year/Period | Source of Data |

|---|---|---|---|

| Fast Fashion Market Size | $161.7 billion | 2025 Projection | |

| Secondhand/Resale Apparel Market Share | 10% of Global Apparel Market | 2025 Expectation | |

| Online Sales in Off-Price Retail | 30% of Total Sales | 2023 Figure | |

| Citi Trends, Inc. Store Count | 590 locations | Q2 Fiscal 2025 End |

The competition isn't just from new digital players, though. The circular economy is a major substitute force. Thrift stores, secondhand markets, and luxury consignment shops offer alternative deep-discount options that appeal to the increasingly sustainability-aware consumer. The resale market, for example, grew 18% in 2023 alone.

However, Citi Trends, Inc. has built-in defenses against pure online substitution. The physical store footprint remains a competitive advantage, especially for their core customer base who value immediate gratification and the tactile experience. The in-store treasure-hunt experience and neighborhood convenience of the 590 stores serve as a barrier to pure online substitution.

You can see the appeal of the physical experience reflected in their recent results, which shows the strategy is working to pull customers in:

- Comparable store sales growth for Q2 Fiscal 2025 was 9.2%.

- Year-to-date comparable store sales growth through Q2 Fiscal 2025 was 9.6%.

- The company is actively remodeling stores, planning to remodel approximately 50 stores in 2025.

- The company ended Q2 2025 with $50.4 million in cash and no debt, giving it flexibility to invest in the in-store experience.

If onboarding for online competitors takes 14+ days, churn risk rises for customers seeking immediate, low-cost fashion fixes, which is where Citi Trends, Inc.'s physical presence helps.

Citi Trends, Inc. (CTRN) - Porter's Five Forces: Threat of new entrants

You're assessing barriers to entry in the off-price retail space, and for Citi Trends, Inc. (CTRN), the hurdles for a new competitor are substantial, leaning the threat toward low to moderate. The primary defense isn't just capital; it's the operational complexity of their model. New players can't just open stores; they need an established, complex opportunistic buying infrastructure to consistently source the deep discounts that define the value proposition. That takes time and connections, which are not easily bought off the shelf.

Consider the sheer physical footprint a rival would need to match. Citi Trends, Inc. already operates a network that is difficult and expensive to replicate quickly. This scale advantage acts as a significant deterrent against smaller, less capitalized entrants. To even approach parity, a new company would need to immediately fund the build-out of a store base exceeding the current 590 locations across 33 states.

Here's a quick look at the scale and financial muscle Citi Trends, Inc. brings to bear against potential rivals:

| Metric | Value (as of late 2025 data) | Significance to Barrier |

|---|---|---|

| Current Store Count | 590 locations | Requires massive initial capital outlay to match footprint. |

| Geographic Footprint | 33 states | Indicates established national logistics and brand recognition. |

| Cash on Hand (Q2 2025) | $50.4 million | Provides a strong financial buffer against capital-intensive rivals. |

| Total Debt (Q2 2025) | $0 | Maximum financial flexibility for defense or strategic investment. |

| Planned FY 2025 CapEx | Up to $25 million | Reinforces scale advantage through store remodels and new openings. |

That strong balance sheet is a key defensive moat. As of the second quarter of fiscal 2025, Citi Trends, Inc. held $50.4 million in cash and carried absolutely no debt. This financial posture means they can weather competitive pricing wars or fund their own expansion/remodel plans without the immediate pressure of servicing debt, something a startup would certainly face. It's defintely a solid foundation.

Beyond the numbers, the core of the business is deeply embedded in its customer base. The specialized focus on the African American consumer requires deep cultural and merchandising knowledge that is incredibly hard to replicate quickly. New entrants must understand the specific 'Cultural Cachet' that drives purchasing decisions, which is not something you can learn from a textbook. This specialized knowledge translates directly into inventory productivity.

The ongoing investment in the existing fleet further solidifies this advantage. Citi Trends, Inc. is reinforcing its physical presence and customer experience through strategic spending. This commitment to the store base is visible in their planned capital expenditures for 2025:

- Remodel approximately 60 stores to the updated format.

- Plan to open up to 3 new stores.

- Plan to close up to 3 locations, optimizing the fleet.

- Total planned capital expenditures for the year are between $22 million and $25 million.

This continuous investment in store modernization, coupled with the established supply chain for opportunistic buying, creates a high-cost, high-risk proposition for any company thinking about entering this specific value segment. Finance: draft 13-week cash view by Friday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.