|

Energy Recovery, Inc. (ERII): 5 FORCES Analysis [Nov-2025 Updated] |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

Energy Recovery, Inc. (ERII) Bundle

You're looking for a clear-eyed view of Energy Recovery, Inc.'s competitive moat as we head into 2026, and frankly, the five forces tell a fascinating, slightly contradictory story. While the company's proprietary PX technology secures a near-monopolistic edge-evidenced by that 64.2% Q3 2025 gross margin-you can't defintely ignore the high bargaining power of customers, who negotiate massive, lumpy deals like the nearly $33 million Saudi order late last year. I've mapped out the entire landscape below, from the low threat of new entrants to the moderate risk from substitute energy recovery devices, so you can see precisely where the real leverage sits in this specialized fluid exchange market.

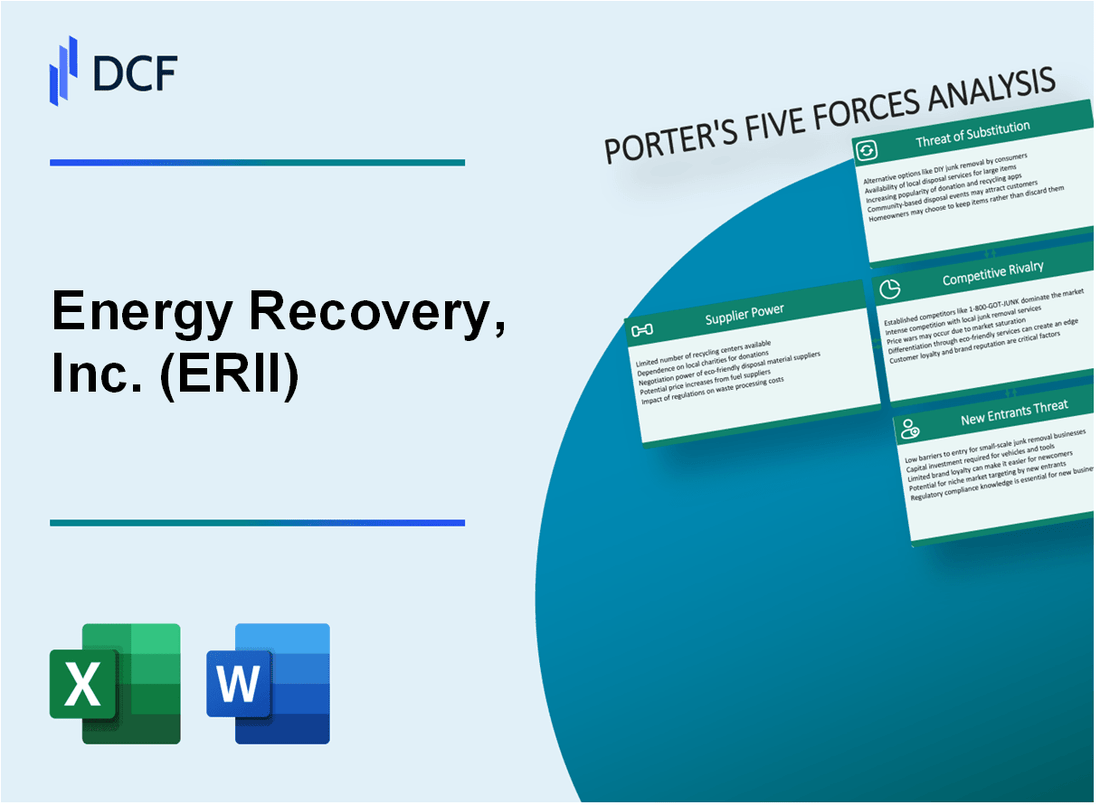

Energy Recovery, Inc. (ERII) - Porter's Five Forces: Bargaining power of suppliers

When you look at the supply side of Energy Recovery, Inc. (ERII), you see a structure intentionally designed to keep supplier leverage low. This isn't accidental; it's baked into their core technology strategy, which is a smart move for maintaining margin control.

The primary defense against supplier power comes from Energy Recovery, Inc.'s deep vertical integration, specifically in manufacturing the heart of their product. Alumina ceramic components for their PX products are manufactured in-house, right there in their California facilities, starting from high-purity alumina raw material all the way to the final product. This in-house ceramics precision manufacturing process means they control the quality and precision of their most critical elements, which is a massive moat against external component suppliers.

The proprietary PX cartridge itself is a testament to this strategy. It's engineered with only a single moving part, and that part is made of that specialized, high-purity alumina ceramic. This design choice inherently limits the need for complex, multi-sourced mechanical assemblies, simplifying the supply chain for the most crucial element. Furthermore, the company has reinforced this durability, announcing in February 2025 that the PX components now boast a validated 30-year design life, which certainly helps mitigate supplier power related to replacement parts.

Here's a quick look at how external factors, like supplier-related costs, showed up in the latest reported financials:

| Metric | Q3 2025 Value | Comparison/Context |

|---|---|---|

| Revenue | $32.0 million | Decrease of $6.6 million compared to Q3 2024. |

| Gross Margin | 64.2% | Down 90 bps compared to Q3 2024. |

| Primary Margin Headwind | Product Mix and Tariffs | These factors slightly lowered the gross margin. |

| Cost of Revenue | $11.44 million | Pressured the gross profit margin. |

Supplier power is definitely mitigated by Energy Recovery, Inc.'s control over precision component quality and design. They leverage their ceramics manufacturing across all PX product lines, ensuring everything meets their high standards. Still, you can't ignore the external pressures that creep in. While they control the core ceramic piece, the overall cost structure is sensitive to the product mix sold in a given quarter and, notably, tariffs.

The Q3 2025 results clearly show this sensitivity. The gross margin of 64.2%, while robust, was slightly lower than the prior year, primarily due to costs related to product mix and tariffs. Management noted that tariffs impacted the Q3 gross margin, and they are actively pursuing a manufacturing option to avoid China tariffs. This indicates that while they control the design and core component manufacturing, the raw material sourcing and global trade environment still introduce some external cost volatility.

To summarize the supplier leverage points:

- In-house manufacturing of core PX ceramic components.

- Proprietary PX cartridge uses only one moving part.

- Material is high-purity alumina ceramic, corrosion-proof.

- Vertical integration controls precision down to the micrometer level.

- Redundant sources qualified for many critical raw materials.

- Tariffs slightly pressured the Q3 2025 gross margin of 64.2%.

Finance: draft 13-week cash view by Friday.

Energy Recovery, Inc. (ERII) - Porter's Five Forces: Bargaining power of customers

You're analyzing Energy Recovery, Inc. (ERII) and the customer side of the equation shows significant leverage. The bargaining power of customers in the Water segment is high, largely because the business model relies on securing and executing what we call mega-project shipments. These are not small, recurring orders; they are massive, discrete capital expenditures, which naturally gives the buyer more negotiating muscle.

The concentration of revenue in a few key geographic areas underscores this power. For the fiscal year ending December 31, 2024, the Middle East and Africa region alone accounted for 62.55% of Energy Recovery, Inc.'s total product revenue. When a single region drives such a dominant share, the major customers within that region-often government-backed municipal water authorities or large Engineering, Procurement, and Construction (EPC) firms-hold considerable sway over terms and pricing.

To be fair, this lumpy nature was evident even in late 2024, when the company flagged potential shipment delays in Q4 because just five projects represented approximately 50% of the revenue for that quarter. That level of dependence on a handful of large orders means those buyers know exactly how critical their purchase is to Energy Recovery, Inc.'s short-term financial performance.

These customers are large, sophisticated entities. They aren't buying off-the-shelf components; they are entering into highly-negotiated, multi-million dollar contracts for critical infrastructure. Energy Recovery, Inc.'s success in securing these deals speaks to the technological advantage of their PX® Pressure Exchanger® (PX) devices, but the negotiation process itself is intense.

Consider the sheer size of recent wins, which exemplifies the high-stakes nature of these customer relationships:

| Project Location/Region | Contract Value (Approximate) | Announcement Date | Product Focus |

|---|---|---|---|

| Saudi Arabia | Nearly $33 million (specifically $32.8 million) | November 2025 | Seawater Reverse Osmosis (SWRO) Desalination |

| Gulf Region (Qatar, UAE) | Approximately $31 million | September 2025 | SWRO Desalination Projects |

| Gulf Region | Over $28 million | February 2024 | Mega Desalination Projects (PX Q400) |

| Spain | Over $7 million | May 2025 | SWRO Desalination Projects (Including Retrofit) |

These multi-million dollar contracts are the norm, not the exception, for the Water segment. For instance, the late 2025 Saudi Arabia order, valued at nearly $33 million, is expected to be fulfilled by the end of 2025. When you are dealing with contracts of this magnitude, the customer's ability to dictate terms, payment schedules, and even product specifications based on their long-term operational needs is substantial. The power comes from the size of the check they write.

Here's the quick math on customer concentration by geography for 2024:

- Middle East and Africa: 62.55%

- Asia: 24.88%

- Europe: 6.36%

- Americas: 6.21%

This geographic skew means that the bargaining power is effectively concentrated in the hands of a few major sovereign or quasi-sovereign entities in the Middle East and North Africa. If one of those key customers pushes back hard on pricing or delivery terms, Energy Recovery, Inc. has limited immediate recourse to offset that revenue loss elsewhere.

Finance: draft 13-week cash view by Friday.

Energy Recovery, Inc. (ERII) - Porter's Five Forces: Competitive rivalry

You're looking at the competitive landscape for Energy Recovery, Inc. (ERII), and honestly, in their core desalination business, the rivalry feels pretty muted. It's almost a near-monopolistic setup for their key technology in that space. We see this reflected in their financial performance, which suggests they have serious pricing leverage. For instance, Energy Recovery, Inc. posted a gross margin of 64.2% for the third quarter of 2025. That's a strong number, even if it was a slight dip of 90 basis points from the 65.1% seen in Q3 2024.

The reason for this strong position is the technology itself. The PX Pressure Exchanger is the differentiator here. It's not just good; it's technically superior to many alternatives. The device achieves a peak efficiency of up to 98%. To be fair, actual operating efficiency usually settles between 93% and 96.4%, but even that is best-in-class. Plus, they just extended the expected durability, which cuts down on customer replacement risk. The PX Pressure Exchanger components now boast a 30-year design life, up from the previous 25-year standard.

Here's a quick look at how that core technology stacks up against its own benchmarks. This shows why customers stick with Energy Recovery, Inc. when they are building major water infrastructure:

| Metric | Energy Recovery, Inc. PX (Latest Spec) | Previous PX Spec | Impact on Rivalry |

|---|---|---|---|

| Peak Efficiency | Up to 98% | Not explicitly stated as lower, but Q400 is 97.3% min | High barrier to entry |

| Design Life | 30 years | 25 years | Reduces long-term customer switching costs |

| Deployed Units | Over 35,000 | N/A | Establishes market incumbency |

Still, direct competitors do exist, especially in the broader energy recovery device (ERD) space, including isobaric devices like DWEER, iSave, and XPR, though specific market share data for these against Energy Recovery, Inc. isn't readily available in the latest reports. We see other industrial machinery names like Kadant (KAI) mentioned in competitor lists, but they operate in a different sphere. The key takeaway is that while alternatives are present, the technical moat around the PX in high-pressure desalination seems wide, supported by that 64.2% gross margin in Q3 2025.

We should also note that while the gross margin is high, the operating margin contracted year-over-year. In Q3 2025, the operating margin was 11.4%, a significant drop from 18.3% in Q3 2024. This suggests that while the cost of goods sold (COGS) relative to revenue is well-managed (hence the high gross margin), operating expenses-perhaps R&D or SG&A-increased relative to the $32.0 million in revenue reported for the quarter.

The competitive dynamic is also shaped by the sheer volume of installed base, which acts as a switching cost barrier. Energy Recovery, Inc. has over 35,000 PX devices deployed. That's a lot of installed technology that customers rely on for critical water production.

- The PX technology can reduce SWRO energy consumption by up to 60%.

- Q3 2025 revenue came in at $32.0 million.

- Adjusted EBITDA for Q3 2025 was $6.8 million.

- Management reiterated its four-year revenue guidance following Q3 2025 results.

Energy Recovery, Inc. (ERII) - Porter's Five Forces: Threat of substitutes

You're looking at the competitive landscape for Energy Recovery, Inc. (ERII) as of late 2025, and the threat of substitutes is definitely a key area to watch. While the PX device is the established leader in its core desalination market, other energy recovery device (ERD) types still pose a moderate threat, mainly hydraulic turbochargers and Pelton wheels.

The containment of this threat comes down to the PX device's superior economics, particularly in Seawater Reverse Osmosis (SWRO). The PX technology can deliver up to 60% energy reduction in SWRO applications compared to systems without energy recovery. When you look at the hard numbers against turbine-style ERDs, the difference in performance is stark, which should keep substitution risk manageable in this mature segment.

Here's a quick math comparison showing why the PX technology is the preferred economic choice over turbine ERDs, which are a primary substitute in the desalination space:

| Metric | PX Device (Pressure Exchanger) | Turbine ERD |

|---|---|---|

| Effective Energy Conversion Efficiency (EECE) | 93.9% | Lower by 15.5% relative to PX |

| Energy Consumption (SWRO) | 3.03 kWh/m³ | Approximately 3.37 kWh/m³ (Higher by 0.34 kWh/m³) |

| Proven Availability (Uptime) | 99.8% | Implied lower due to industry reports of failure and low availability |

| Projected Design Life | 30 years (Confirmed in 2025) | Not explicitly stated as 30 years in current data |

That 30-year design life, officially confirmed in February 2025 after internal testing, gives the PX device an unmatched life-cycle cost advantage over alternatives. Honestly, when you consider that selecting the wrong ERD technology could cost an owner more than twice the initial capital expenditure for the ERD solution over the project's life, durability becomes the primary economic driver, not just initial efficiency. For instance, a conservative estimate shows that just one day per month of unplanned downtime could cost a 100,000 m³/day plant $3.2 million in lost margin over a 25-year life cycle at an 8% interest rate.

Substitution risk does appear higher in newer segments where Energy Recovery, Inc. (ERII) is expanding, such as $\text{CO}_2$ refrigeration. While new data released on October 29, 2025, shows the PX G1300 significantly boosts performance in these systems, alternatives in this space are still establishing themselves. The market itself is set for massive growth, which means more potential for competing technologies to gain a foothold.

To give you context on the scale of this emerging segment, the global subcritical $\text{CO}_2$ refrigeration system market is projected to grow from USD 3.8 billion in 2025 to USD 8.1 billion by 2035. That represents a market value increase of 115.9% over the decade, so establishing the PX device as the standard here is a near-term strategic imperative.

- The PX device has over 35,000 units installed in SWRO facilities worldwide.

- These installations save plant owners an estimated $6 billion in energy costs annually.

- The PX Q400 offers a projected Specific Energy Consumption (SEC) reduction of over 30% compared to a turbocharger.

- The PX Q400 projects a device efficiency of 96.70%.

Finance: draft 13-week cash view by Friday.

Energy Recovery, Inc. (ERII) - Porter's Five Forces: Threat of new entrants

You're looking at Energy Recovery, Inc. (ERII) and wondering how easy it would be for a competitor to walk in and start taking market share, especially in their core desalination business. Honestly, the threat of new entrants here is low, defintely low, because the barriers to entry in specialized, high-pressure fluid exchange technology are extremely high.

Replicating the proprietary PX technology isn't just about copying a design; it requires significant capital investment and deep, proven Research & Development (R&D). Energy Recovery, Inc. has been refining this core technology for more than 30 years, starting its commercial sales in seawater reverse osmosis (SWRO) desalination in 1997. This long history means any new entrant must not only fund their own R&D but also match decades of accumulated, real-world operational data.

The sheer scale of the company's installed base creates a massive experience curve barrier. New players don't just compete on price; they compete against proven uptime and efficiency. Energy Recovery, Inc. has supplied over 30,000 Pressure Exchanger units across more than 100 countries worldwide. This installed base translates directly into customer confidence and reduced perceived risk for large infrastructure projects.

New entrants face long sales cycles, especially in the water infrastructure sector where reliability is paramount. They need to overcome Energy Recovery, Inc.'s incumbent 30-year track record for reliability. For instance, recent project wins in Saudi Arabia in November 2025, valued at nearly $33 million, underscore the scale of deals that require this level of proven performance.

Here's a quick look at the established metrics that set the bar for any potential competitor:

| Barrier Component | Metric | Value | Context |

|---|---|---|---|

| Technology Longevity | Years in Seawater Desalination Market | Over 30 | Since commercialization in 1997 |

| Installed Base Scale | Total PX Pressure Exchangers Supplied | Over 30,000 | Deployed globally |

| Energy Efficiency Barrier | Energy Reduction in SWRO | Up to 60% | Core value proposition of the PX technology |

| Operational Reliability | PX Device Efficiency | Up to 98% | Best-in-class performance |

| Market Traction (Recent) | Value of Saudi Arabia Project Wins (Nov 2025) | Nearly $33 million | Demonstrates current deal size and market acceptance |

The company's focus on cost control, even while maintaining R&D, suggests they are protecting their profitability, which is supported by a high gross margin, noted as 64.0% in Q2 2025. This financial strength helps them weather market fluctuations better than a startup trying to fund initial R&D and sales efforts simultaneously.

Even in newer segments like CO2 refrigeration, where Energy Recovery, Inc. is still building traction, the path to market is slow. Management indicated that real commercialization for the CO2 business is likely going to happen in 2026 or later, with scaled adoption potentially not until 2027. This signals that even where the technology is newer, the process of gaining OEM specification and customer rollout is protracted, reinforcing the difficulty for a new entrant to gain rapid footing.

The barriers to entry are structural, rooted in:

- Proprietary ceramic rotor design.

- Decades of field performance validation.

- High capital required for manufacturing scale-up.

- Established customer relationships in critical infrastructure.

Finance: draft 13-week cash view by Friday.

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.