|

The Karnataka Bank Limited (KTKBANK.NS): BCG Matrix |

Fully Editable: Tailor To Your Needs In Excel Or Sheets

Professional Design: Trusted, Industry-Standard Templates

Investor-Approved Valuation Models

MAC/PC Compatible, Fully Unlocked

No Expertise Is Needed; Easy To Follow

The Karnataka Bank Limited (KTKBANK.NS) Bundle

In the ever-evolving landscape of banking, understanding where a company stands can significantly impact investment decisions. The Karnataka Bank Limited, with its diverse range of offerings, presents a fascinating case study when analyzed through the Boston Consulting Group (BCG) Matrix. From innovative digital banking solutions that shine as Stars to traditional practices that struggle as Dogs, each quadrant reveals vital insights about the bank's strategic positioning. Dive in to explore the dynamic interplay of Cash Cows and Question Marks shaping its future!

Background of The Karnataka Bank Limited

The Karnataka Bank Limited, established in 1924, is one of the oldest private sector banks in India. Headquartered in Mangaluru, Karnataka, it has grown steadily, developing a significant footprint across the country. As of October 2023, the bank operates through a network of over 900 branches and a presence in over 20 states.

Initially focused on serving the needs of the local population, Karnataka Bank evolved into a full-service bank offering a wide array of products such as retail banking, corporate banking, and treasury services. Its diverse offerings have helped the bank tap into various market segments, catering to individual customers as well as businesses.

Financially, the bank reported a net profit of approximately ₹600 crore for the fiscal year 2022-23, marking a growth of about 15% compared to the previous year. The asset quality has also shown resilience, with a Gross Non-Performing Asset (GNPA) ratio of 2.77%, reflecting cautious lending practices.

In its pursuit of digital transformation, the Karnataka Bank has embraced technology with initiatives such as mobile banking apps and online banking services, aiming to enhance customer convenience and operational efficiency. The bank's efforts in adopting a hybrid model of banking have positioned it well in the competitive landscape of the Indian banking sector.

The Karnataka Bank Limited has also been recognized for its commitment to corporate social responsibility (CSR), investing in educational programs, healthcare, and environmental sustainability, which further solidifies its reputation as a community-focused institution.

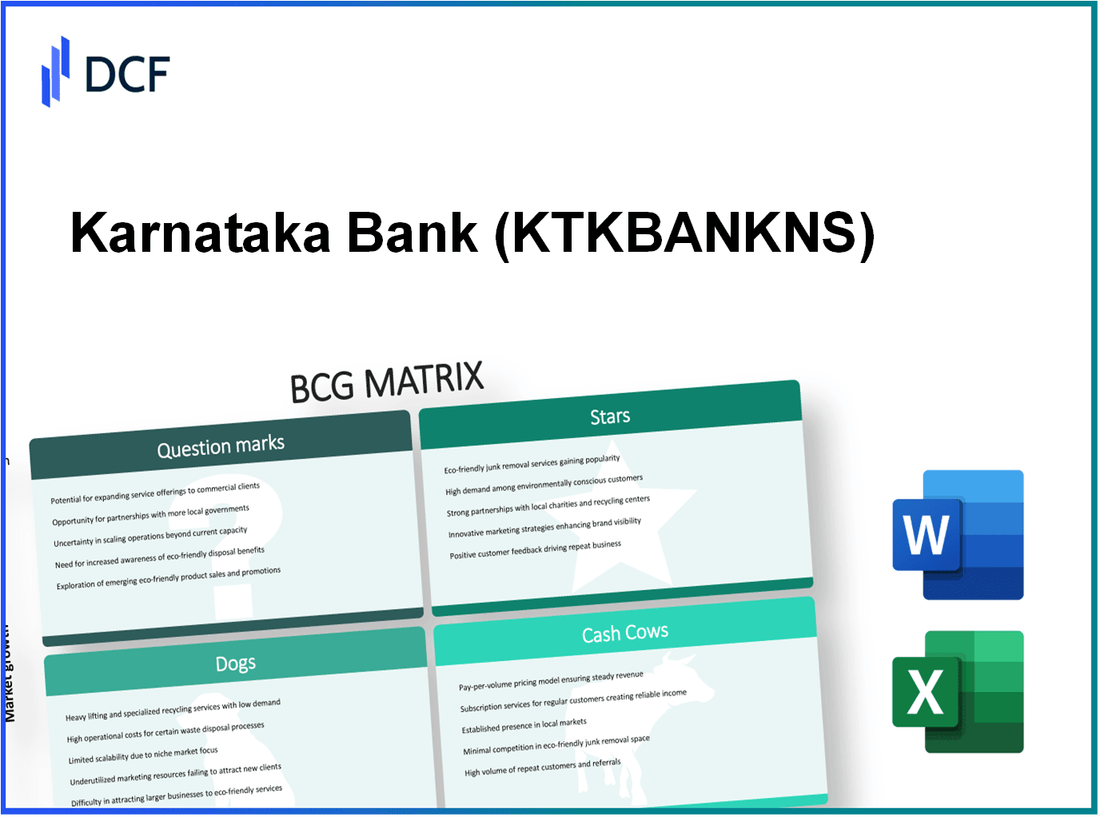

The Karnataka Bank Limited - BCG Matrix: Stars

The Karnataka Bank Limited operates several key business segments that can be classified as Stars within the BCG matrix. These segments exhibit high market share in a rapidly growing financial services market.

Digital Banking Services

Karnataka Bank's digital banking services have seen significant growth. As of 2022, the bank reported a digital banking transaction value of approximately ₹5,700 crore, reflecting a year-on-year growth of 25%. The bank's digital platform boasts over 1 million registered users.

Mobile Apps for Banking

The bank's mobile banking application has recorded over 2 million downloads. In 2023, the app maintained a user satisfaction score of 4.5 out of 5 on prominent app stores. Furthermore, the app facilitates transactions averaging ₹1,000 crore monthly, indicating a strong uptake among customers.

Fintech Partnerships

Karnataka Bank has strategically partnered with multiple fintech companies to enhance its service offerings. In 2023, the bank reported that partnerships with fintech firms contributed to a revenue increase of ₹300 crore, accounting for approximately 15% of the total service-based income. Notable collaborations include alliances for payment gateways and digital lending solutions.

Internet-Based Loan Applications

The bank's internet-based loan application process has been streamlined, resulting in a significant increase in loan disbursals. In 2022, the bank processed over 40,000 loan applications through its online platform. The average processing time has reduced to 48 hours, enhancing customer satisfaction and increasing the loan book by 30% year-on-year.

| Segment | Key Metrics | Year-on-Year Growth |

|---|---|---|

| Digital Banking Services | Transaction Value: ₹5,700 crore | 25% |

| Mobile Banking App | Downloads: 2 million User Satisfaction: 4.5/5 |

N/A |

| Fintech Partnerships | Revenue Contribution: ₹300 crore | 15% |

| Online Loan Applications | Applications Processed: 40,000 Average Processing Time: 48 hours |

30% |

With these high-growth business units, Karnataka Bank demonstrates strong potential to maintain its market leadership and evolve into a more significant revenue generator over time. The investments in these segments are crucial for sustaining growth and achieving long-term success.

The Karnataka Bank Limited - BCG Matrix: Cash Cows

In the context of The Karnataka Bank Limited, several key areas can be classified as Cash Cows, reflecting their high market share and significant contribution to cash flow despite low growth prospects. These areas are primarily focused on retail and corporate banking services.

Retail Banking Services

The retail banking segment of Karnataka Bank has consistently demonstrated strong performance. As of the financial year ended March 31, 2023, retail banking contributed approximately 61% to the bank's total business. The bank’s retail loans reached about ₹20,000 crore, showcasing its strong foothold in this sector.

Fixed Deposits

Fixed deposits remain a vital source of funds for Karnataka Bank. As per the latest financial data, the total amount of fixed deposits stood at around ₹35,000 crore as of March 2023. This segment benefits from the bank's competitive interest rates, which generally range between 5.00% to 6.10% depending on the tenure.

Home Loans

Karnataka Bank has a robust portfolio in home loans, which contributed significantly to its cash flow. The outstanding home loan portfolio was approximately ₹6,500 crore by March 2023, with a market share of about 2.5% in the Indian home loan market. The average interest rate for home loans is 8.00%, which attracts a steady stream of borrowers.

Corporate Banking Services

Corporate banking is another critical Cash Cow for Karnataka Bank. As of the fiscal year 2022-2023, corporate loans made up around 24% of the total loan portfolio, translating to about ₹15,000 crore. The bank provides various facilities such as working capital finance, trade finance, and term loans to corporate clients.

| Bank Segment | Contribution (₹ Crore) | Market Share | Interest Rate Range |

|---|---|---|---|

| Retail Banking Services | 20,000 | 61% | N/A |

| Fixed Deposits | 35,000 | N/A | 5.00%-6.10% |

| Home Loans | 6,500 | 2.5% | 8.00% |

| Corporate Banking Services | 15,000 | 24% | N/A |

Investments and operational efficiencies in these Cash Cow segments allow Karnataka Bank to generate stable cash flows that can be utilized for various corporate needs, including funding growth in other areas like 'Question Marks' and supporting overall business sustainability.

The Karnataka Bank Limited - BCG Matrix: Dogs

In the context of the Karnataka Bank Limited, the 'Dogs' segment encompasses various aspects of its operations that are characterized by low market share and low growth potential.

Traditional Banking Branches

The Karnataka Bank has been facing challenges with its traditional banking branches as customer preferences shift towards digital banking solutions. As of 2022, the bank had approximately 850 branches. However, the growth in branch numbers has stagnated, reflecting broader industry trends where many banks see a decline in foot traffic.

Manual Processing Systems

The reliance on manual processing systems has resulted in inefficiencies. According to the bank's 2022 annual report, operational costs related to manual services constituted about 35% of total operational expenses. This has led to longer turnaround times, impacting customer satisfaction and retention.

Outdated Financial Products

Karnataka Bank’s financial products, particularly some savings accounts and fixed deposits, have not evolved to meet market demands. For instance, the interest rate on certain legacy savings accounts was around 4%, which is relatively low compared to competitors offering rates up to 6% or more. This has resulted in stagnant growth in this segment, further cementing its position as a 'Dog.'

Non-Performing Loans

Non-performing loans (NPLs) represent another critical issue. As of September 2023, the bank's Gross NPA ratio stood at 4.2%, reflecting a persistent problem in managing credit risk. This has consumed resources, with provisions for bad loans amounting to approximately ₹1,000 crore in FY2023, thereby limiting the bank's ability to invest in more promising ventures.

| Parameter | Value |

|---|---|

| Number of Branches | 850 |

| Manual Processing Expenses (%) | 35% |

| Legacy Savings Account Interest Rate | 4% |

| Competitor Interest Rate | 6% |

| Gross NPA Ratio (%) | 4.2% |

| Provisions for Bad Loans (FY2023) | ₹1,000 crore |

The Karnataka Bank Limited - BCG Matrix: Question Marks

The Karnataka Bank Limited has several business units categorized as Question Marks, which are characterized by their presence in high-growth markets yet holding low market shares. These units require strategic attention to ensure sustained growth and market positioning.

New Market Expansion Strategies

In the fiscal year 2022-2023, Karnataka Bank recorded a 14% increase in total business volume, amounting to approximately ₹1.53 lakh crore. This signals an opportunity for the bank to explore new market segments, particularly in Tier-2 and Tier-3 cities, where potential growth exists. The bank has focused on expanding its presence through digital banking initiatives, currently aiming for an increase in its customer base by 20% by the end of FY 2024.

Investment in Blockchain Technology

Karnataka Bank has allocated approximately ₹20 crore for the development and integration of blockchain technology in its operations, primarily to enhance transparency and security in transactions. With the global blockchain market expected to grow to ₹83.13 billion by 2027, this investment positions the bank to leverage blockchain for improving operational efficiency and customer trust.

Sustainable Finance Products

In line with growing consumer demand, Karnataka Bank launched several sustainable finance products, including green loans aimed at renewable energy projects. The bank targets to disburse ₹1,000 crore in green financing by 2025, which aligns with national goals towards sustainable development. Currently, these products represent less than 5% of the bank’s total loan portfolio but show a 30% annual growth rate in customer inquiries.

AI-Driven Customer Service Solutions

AI-driven customer service solutions are being piloted at Karnataka Bank to enhance customer engagement. The bank has invested ₹15 crore in developing AI-based chatbots and support systems, with a target to reduce customer service response time by 50% by the end of FY 2024. Customer satisfaction metrics indicate that current service technologies have a 70% satisfaction rate; enhancing this through AI could significantly improve retention rates.

| Strategy | Investment | Expected Growth | Current Market Share |

|---|---|---|---|

| New Market Expansion | ₹0.15 lakh crore (20% increase) | 14% | 3% (FY 2023) |

| Blockchain Technology | ₹20 crore | 35% (by 2027) | N/A |

| Sustainable Finance Products | ₹1,000 crore (target by 2025) | 30% (annual growth) | 5% (current) |

| AI-Driven Customer Service | ₹15 crore | 50% (response time reduction) | N/A |

The comprehensive analysis of these Question Marks reveals their potential to transition into more dominant positions, provided the bank implements appropriate strategies for market penetration and investment. Each of these initiatives contributes to the broader goal of enhancing the bank's offerings in a competitive financial landscape.

The Karnataka Bank Limited's strategic positioning within the BCG Matrix reveals a diverse portfolio, showcasing strengths in digital innovation and cash-generating retail services, while also highlighting areas that necessitate reevaluation, such as traditional banking models and emerging technologies. With a focus on leveraging its 'Stars' and 'Cash Cows,' the bank can navigate future challenges and capitalize on opportunities to foster growth and sustainability.

[right_small]Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.